The devaluation of Kwanza and inflation

Some studies by prestigious economic consultants have lately issued some reports on the Angolan economy that only report negative numbers and projections, without taking into account either the theoretical models on which some of the main economic policy decisions in Angola are based, or the actual reality of its economy.

One of the most intriguing cases is the permanent link between the rise in inflation and the devaluation of the Kwanza, presenting the two phenomena as cause and effect or effect and cause, as well as always giving a negative connotation to the term “devaluation”.

This article, which does not aim to make forecasts, which at this time of Covid-19 would be rash, offers alternative explanations behind the Kwanza`s devaluation, looking instead at the opportunity it offers foreign investors.

It is evident that the semi-rigid or controlled exchange rate regime that existed before the adoption of the flexible exchange rate last year, was partly responsible for the crash in the Angolan economy.

In fact, pegging the Angolan currency at a high value in view of market conditions, caused unrestrained consumerism while domestic production was allowed to decline, since international prices were artificially made more competitive.

It was the time when Luanda became the most expensive city in the world with the Angolan elite making flagrant shows of wealth. This situation did not correspond to domestic production or development, but rather excessive spending of foreign currency earned from high oil prices which bolstered the inadequate value of the Kwanza. This was unsustainable.

The prolonged recession since 2014 demanded an end to the artificial appreciation of the Kwanza and the introduction of a flexible exchange rate.

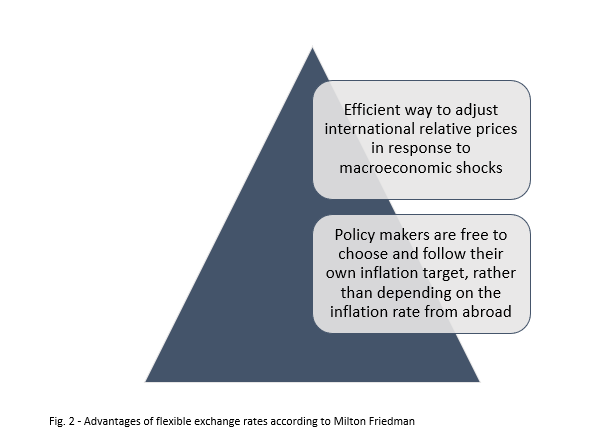

The model underlying the adoption of flexible exchange rates has clear goals. Since Milton Friedman’s seminal text in 1953[1] on flexible exchange rates, two arguments support this policy: first, free movements in exchange rates are an efficient way of adjusting international relative prices in response to macroeconomic shocks; second, with flexible exchange rates, policymakers are free to choose and follow their own inflation target, rather than depending on the inflation rate from abroad. This last factor should be emphasised. Milton Friedman stressed that exchange rates would help to insulate the domestic economy from external shocks and would give national political authorities the ability to meet domestic goals. Flexible exchange rates provide enough insulation to the domestic economy if the sources of the recessionary shock are abroad.

This means that with a flexible exchange rate, it is possible for the government / central bank to pursue an autonomous anti-inflationary policy on the external value of the currency.

In fact, the devaluation of the Kwanza could mean that the prices of international goods become excessively expensive for Angola, and spark that, contrary to what happened previously, being cheaper to produce goods in Angola. That would be the opportunity to invest in Angola`s agriculture and industry, at they will have a market and low production costs due to the devaluation.

With national goods becoming more competitive than corresponding foreign goods, this will boost national production and encourage exports.

And provided that the central bank does not pint excess money, national production should increase and inflation should decrease if internal policies are adequately followed.

This does not mean that the transition from an economy artificially anchored by a high-value Kwanza supported by rising oil prices to a competitive and productive economy is easy. Angola is currently in deep crisis, made worse by the Covid-19 pandemic, and luck, either bad or good, has to be considered.

However, the exchange rate easing policy is right and there is no need to be afraid of devaluation. This is making the economy more competitive overseas and encouraging the manufacture and production of goods to sell both internally and abroad. Success depends more on government policies; policies that are coherent and consistent.

That is why the figures being released on devaluation and inflation are, on the surface, frightening, but they will only have a negative impact if the government implements the wrong policies.

Otherwise, they are not, by themselves, of any relevance. It is known that the Kwanza was overvalued and that this has greatly affected the Angolan economy. It is known that combating inflation, with flexible rates, does not depend on the outside world, but on the right decisions by the government.

There is awareness that Angola is in deep economic crisis, but some real encouraging indicators are beginning to emerge. One of them is that “Angola disbursed, in the first quarter of the year, 495 million dollars (436.5 million euros) on importing food products, a decrease of 31% compared to the 717 million dollars (632.3 million euros) ) for the last quarter of 2019.[2]”

The Angolan government attributed this evolution to a better organisation of its foreign exchange market and to an increase in the demand for national products. Official sources state: “We are verifying these two factors, we can say that we are on the right path, there is a demand for national production, there is a decrease in imports.” These facts seem to confirm the analysis we do. Obviously, in the end everything will depend on the right internal public policies.

[1] Friedman, M. (1953) “The Case for Flexible Exchange Rates.” In Essays in Positive Economics, 157–203. Chicago: University of Chicago Press.

[2] https://www.sapo.pt/noticias/economia/angola-importou-menos-31-de-alimentos-no_5f0f32adb34d505496f5eddd