1-The International Monetary Fund’s report on Angola (Feb.2025)

None of the IMF’s various interventions in Angola have succeeded in changing the country’s economic structure and helping to launch it on a path of development, demonstrating the fragility of the IMF’s models of action in Africa.[1]

When the IMF comes up with equivocal results, it uses ambiguous communiqués that allow for different interpretations and, of course, disempower the institution. This is the case with the organization’s most recent statement on Angola, which is a real exercise in ambivalence.

However, despite this, or above all because of it, this communiqué[2] is a valuable tool from which to draw some conclusions and clues for the future of the Angolan economy, essentially the need for effective and real acceleration of economic reform in the direction of competition, productivity and radical modification of the financial functioning of the state.

On February 24, 2025, the Executive Board of the International Monetary Fund (IMF) concluded its Article IV consultation on Angola. It then issued a communiqué, which has now been made public.

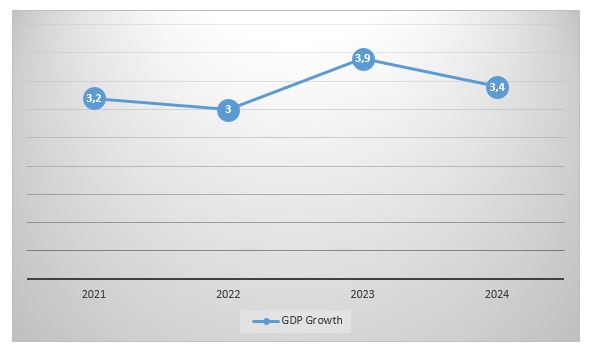

On a positive note, the IMF points out that Angola’s economy recovered in 2024, mainly due to the oil sector. GDP growth is estimated to have reached 3.8 percent, exceeding previous projections, although this growth has been extended to the non-oil sector. The public debt/GDP ratio fell in 2024, benefiting from higher nominal GDP growth and sustained primary fiscal surpluses. This is the good news: the economy is growing due to the oil sector, while at the same time having a spill over effect on the other sectors.

Fig. 1- Evolution of Angola’s real economy as a percentage. Source: IMF 2025

At the same time, the IMF is cautious and somewhat frightened by a number of problems:

-General State Budget (public accounts) slippage due to higher capital expenditure and delay in removing the fuel subsidy.

-High inflation due to exchange rate pressures and food prices.

-Adverse market expectations and a high external debt service put great pressure on the value of the Angolan currency.

Due to the imminent dangers, the IMF “invites” the Angolan Executive to accelerate structural reforms of the economy, in which it emphasizes fiscal consolidation (cutting public spending or increasing taxes), the withdrawal of fuel subsidies, rationalizing public investment and improving the efficiency of spending, strengthening the management of public finances, including the public procurement framework and reforms of public companies. It also reaffirms the need for monetary policy to maintain a restrictive bias to ensure lasting disinflation.

The main emphasis, according to the IMF, should be on pro-market policies aimed at simplifying business regulation, strengthening governance, fighting corruption, developing human capital and deepening financial inclusion. Greater statistical capacity is also needed to support sound policymaking.

2-Beyond the IMF. The necessary reforms

The IMF communiqué itself contains contradictions that show its difficulty in obtaining a realistic view of the Angolan economy. For example, it attributes inflation to the liberalization of the exchange rate and the rise in food prices. Let’s remember that it was the IMF that recommended the abrupt adoption of a totally flexible exchange rate, without noticing that a good part of Angolan food was imported…so it’s an IMF policy that according to the IMF itself generates inflation….

However, further down he talks about the need for a restrictive monetary policy, which is obviously Angola’s major problem and the ultimate source of all inflation, the lax attitude of the BNA which lives with negative reference interest rates in real terms (BNA reference interest rate, 19.5% for inflation of 26.48%) and has difficulties controlling the money supply .[3]

Fig. 2-Development of monetary aggregates as a percentage/end of period. Source: IMF, 2025

Also surprising is the obsession with fuel subsidies, since it is clear that withdrawing them will generate even stronger inflationary pressures and possible social upheaval.

Even the warning about budget slippage seems out of context. If you look, the balance for Angola’s General State Budget (GSB) for 2025 is -1.3% of GDP, nothing significant. In fact, Angola doesn’t need less spending or austerity; on the contrary, it needs more effective spending.

The problems of the Angolan economy do not lie along these lines, but along others that the IMF also addresses, but does not highlight.

The first problem facing the Angolan economy is that of rationalizing public spending. Much of the expenditure is uncontrolled, its destination is unknown, it is the result of over-invoicing, corrupt schemes, endogenous bargaining[4] . Much more than in the United States of America, it is in Angola that a programme like that of Elon Musk and his DOGE (Department of Government Efficiency) would be essential in order to reduce bureaucracy and optimize Angola’s public machine by cutting phantom and invented spending and reformulating government agencies.

In terms of public procurement, it is essential to introduce competition mechanisms. If, perhaps, public tendering is time-consuming and an obstacle to development, allow simplified contracting, but with competition, perhaps through auctions or electronic mechanisms, thoroughly reviewing the current contracting law, which is bureaucratic, slow and unenforceable.

Another important aspect is the renegotiation of the foreign debt. You can’t keep paying billions in capital every year, with the opportunity cost being Angolan development. Paying off the foreign debt under the terms in which it is being paid is an obstacle to the country’s growth.

Domestically, the private economy needs to be stimulated, creating the pro-market conditions that the IMF talks about, with a major effort to reduce bureaucracy, freedom to set up companies, boosting bank credit, depoliticizing the business community and some protectionism for Angola’s infant industries. An internal free market with external protection must be the recipe for the initial years.

We also need to understand the profitability of the large state-owned companies, Sonangol, TAAG, among others, by promoting efficiency in their management and privatizing at least 1/3 of their capital

Even now, Sonangol’s current income statement presents more doubts than certainties: Sonangol ended 2024 with a debt of 4.5 billion dollars, representing an increase of 15.4% on the previous year. At the same time, revenues fell to 10 billion euros last year, a drop of 8.6% in the space of a year. EBITDA (earnings before interest, taxes, depreciation and amortization) also fell by 8.8% year-on-year to 3.2 billion euros[5] . Let’s be clear, these results are not good. It’s not the catastrophe of 2015, but it’s not very encouraging.

The efficiency of companies can be optimized through partial privatization, since management with private partners tends to be more agile and focused on results, possibly encouraging innovation in mixed companies. The introduction of competing visions (state and private) can lead to cost savings and the elimination of unnecessary bureaucracy. Similarly, selling off parts of state-owned companies can generate revenue for the government, easing budget constraints and reducing the need for public funding. Partial privatization can lead to improvements in the quality of services, as private entities focus on customer satisfaction. Finally, mixed companies will have greater flexibility to adapt quickly to market demands.

Essentially:

The state’s financial function will have to be completely restructured, in terms of spending, debt and hiring, possibly by creating an efficiency department like Elon Musk’s in the US.

Introducing a free market in Angola with perfect independence for entrepreneurs to create and manage their companies without bureaucracy and interference from the state and the creation of mechanisms to bring them capital (banks, stock exchanges, venture capital, funds and autonomous state partnerships).

Privatize up to 1/3 of the capital of large state-owned companies, including Sonangol.

All these reforms should be speeded up in the two and a half years that remain before President João Lourenço finishes his term in office.

https://www.cedesa.pt/wp-content/uploads/2025/02/economia-angolana.jpeg7041408CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2025-02-28 11:09:002025-02-28 17:03:11Angolan economy: time for accelerated reforms

The results of Angola’s economic policy, which had been favourably received by international institutions and public opinion in recent times, namely low inflation, fiscal consolidation, control of public debt and the success of foreign exchange liberalisation, seemed to suffer a blow in June.

The trigger for this change in perception was the abrupt announcement of the rise of more than 80% in the price of commercial petrol, due to the partial withdrawal of the state subsidy (without the necessary focus on the mitigation measures that had been well thought out), which was followed by a series of cascading events, the resignation of Manuel Nunes Júnior as Minister of State for Economic Coordination, some rumours about delayed public service salaries, and inevitably the announcement by a rating agency that Angola’s economic outlook had been downgraded from “positive” to “stable”.[1]In addition, the Kwanza is depreciating rapidly against the dollar and the euro. At the end of June, the Angolan national currency passed 800 kwanzas to the dollar for the first time.[2]

The depreciation of the kwanza has raised renewed fears of inflation, in a country still heavily dependent on imports for its daily life. Last February, the National Bank of Angola said that the country would spend over US$2 billion (1.8 billion euros) on food imports in 2022, representing a 40 percent increase over the previous year.[3] A lower value of the national currency and a rise in food import requirements obviously results in higher prices.

In turn, the statement that the new Minister of State and Economic Coordination made about the delays in some public salaries in May, did not reassure, since Lima Massano assured that this was due to “a time lag between the time of receipt of the funds resulting from tax collection and the period of payments.”[4] The minister’s explanation is not contested, the problem is that even if we accept it, it contains a problem, which is that of the government’s lack of cash reserves, indicating that the budgetary restraint imposed by the International Monetary Fund (IMF) has not created any space for Angolan public finances. It should be noted that although the price of oil is not very high, over the last six months it has fluctuated between USD 70 and 80, with prevalence at USD 75/76. As the State Budget was based on 75 USD (which we criticised at the time[5] ), the truth is that the price has been in line with the forecast, although with no margin for manoeuvre.

The possible effect of oil prices

In the light of the above, in theory, the price of oil will not yet have a negative effect on the State Budget in the immediate future.

However, this could happen in the second half of the year. We have formed the opinion that there is a strong downward pressure on the price resulting from the oil embargoes on Russia and probably Iran. Our thesis is that these Western oil embargoes do not have the effect of significantly restricting the supply of that product by Russia, which would push up the price of oil, but rather of selling it at a discount to intermediaries who act as “laundromats”. This means that the longer the oil embargo on Russia lasts, the more Russia will make the circumvention mechanisms efficient and the more it will sell oil at a discount. Thus, it is very possible that there will continue to be downward pressure on the price of oil, especially if China’s economy continues not to show the strength of the past.

Consequently, it may be that fiscal tightening will intensify in the second half of this year if oil prices succumb to these pressures.

The doctrinal and practical problem

The concrete fact is that IMF “recipes” in Angola seem to have failed, and once again the application of classical economic doctrines does not work.

It is increasingly clear that a universal theory of economics based on the classical thinking disseminated by North American universities may work in mature developed economies or in places with relatively solid institutions (market, government, courts), but it does not work in countries still suffering from extreme imbalances and under institutional construction. It cannot speak of true markets functioning freely according to the rules of supply and demand, nor of efficient governance or even of a justice system approaching that which works in Angola. For various reasons, these are unfinished processes in the making. To that extent, any economic model that takes them as preconditions will fail. That is why the IMF measures fail, failing to bring prosperity to Angola and making the country go from one crisis to another. It should be stressed that since 2009 the IMF has been monitoring and agreeing with Angola’s economic policies.

There is a doctrinal problem underlying the negative impact of economic policy in Angola that is linked to the fact that the main decision-makers are trained in foreign universities that adopt institutional models of the market economy, with greater or lesser state intervention, but always assuming that the situation is operating normally. The truth is that Angola is in a pre-institutional situation, so the models to be applied should be those of development and institutional building rather than stabilization. This problem, while seemingly very theoretical, has real practical relevance, since something is being applied that has little to do with reality.

Furthermore, some fundamental structural reforms were not undertaken by the government. A system marked by the interference of politicians in the running of companies was maintained, with continued investment in oligopolies that are essentially importers, justice was not speeded up and bureaucracy was clearly not reduced.

The combination of these factors means that the Angolan economy has not yet emerged from the oil cycle and from repeating past mistakes.

The questioning of Agenda 2050

It is these basic deficiencies that appear to limit the effect of Agenda 2050. In a previous report we praised the unassuming and honest way in which the authors of the Agenda made the diagnosis of the past and present situation[6] , and we had some anticipation in reading the proposals for the future.

It is evident that Agenda 2050[7] has many interesting objectives and profound analyses that stimulate the debate, which should be broadened in Angolan society. However, at its core the document does not bring us the necessary ambition and has the defect of being based, as we have mentioned, on generalist models.

If we notice the essential core of the strategic objectives is hardly mobilising. The predicted increase until 2050 of the GDP is 2.4 times, which in terms of GDP per capita, assuming that the population growth is only 2.1 times (and may be much more) results in an increase from USD 3,675 to USD 4,215 of the mentioned GDP per capita. If we look at this, it is a rise in population welfare of only 14% in 27 years[8] . Add that unemployment will still be around 20%. An extremely high figure, although the statistical formula used by the National Statistics Institute of Angola (INEA) cannot be compared with others because it is more demanding and therefore presents more negative results .[9]

It is very discouraging. In fact, in view of the increase in population, what Agenda 2050 is putting as a goal is a quasi-progression. Is it not possible to do differently?

Angola in 2050 is supposed to be similar to what today are countries like Paraguay, Jordan, Sri Lanka, Essuatini or Mongolia[10] . We cannot subscribe to this vision, which in practice envisages a stagnant country where a sharper rise in population will pose severe problems.

Conclusions

In all independence and objectivity, we believe that this future Agenda should be fundamentally revised and substantially altered with the participation of the Economic and Social Council, the various study centres working on Angola in universities and elsewhere, and the country’s living forces, with a view to presenting a model that is both ambitious and feasible for Angola’s future. Only in this way will the current problems resulting from bad doctrinal models and little structural reformism be overcome.

Further and faster has to be the motto of the future.

[10] Countries that currently have a GDP per capita close to 4125 USD. GDP, Per Capita GDP – US Dollars”, and 2018 to generate the table), United Nations Statistical Division.

https://www.cedesa.pt/wp-content/uploads/2023/06/situacao-economica-em-angola.jpg465830CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2023-07-07 10:20:002023-07-07 10:23:20The economic situation in Angola and Agenda 2050

In this document there are necessary conditions and possible solutions for the removal of the subsidy to fuel in Angola.

1-The necessary conditions are:

a) Creation of transparency mechanism of budgetary financial flows. The fate of savings made with the withdrawal of subsidies, emphasizing social aspects;

b) Modification of the oligopolistic market structure. Promotion of competition in the fuel distribution market. One hypothesis is the split of Sonangol distribuição in three entities and privatization of two of them.

2-The possible solutions are:

a) Focus on the subject

AA) direct subsidy to the most disadvantaged and social pass

AB) direct allowance to companies

AC) Tax Benefit /Negative Tax to AA) and AB)

b) Focus on the object

BA) Subsidized fuel prices continues for lower displacement vehicles

BB) subsidized fuel prices continue for transportation companies and similar

c) Composite systems

***

Elimination Fuel Subsidies: IMF and Vera Daves

It is an integral part of any intervention of the International Monetary Fund (IMF) to have fuel subsidies withdrawn, where they exist. Of course, the same booklet was followed in Angola creating this burden on the Angolan government.

In terms of fiscal policy, in the recent Staff Report according to article IV the fund makes this the main measure to take at the level of fiscal policy, prescribing that: “Authorities need to take political action to increase non-oil tax revenues and gradually eliminate fuel subsidies while increasing support for vulnerable. These measures should help reduce vulnerabilities debt, create tax space and achieve their fiscal and medium-term debt goals. ”[1] (emphasis added).

Minister Vera Daves tunes for the same tuning fork, and in a recent interview said that the removal of fuel subsidies is “the elephant in the middle of the room, and with ballerina shoes”, stating that the political decision was made and was not implemented only because it is lacking to find the mechanism that reduces the impact on the most disadvantaged. And she explained that: “It is a blind subsidy, which everyone accesses, and with this revenue we could have a more directed policy instead of subsidizing those who do not need.” Adding arguments for the elimination of this measure as “fuel leakage to neighboring countries, lack of market share and the consequent loss of tax revenue, beyond the issue of inequality of treatment. There are several distortions to the market, but we are aware that the impact, especially through transport, is considerable. “It also recognized the negative impact on municipalities, industries and farms and the price of freight to transport food. And concluded by saying:” We have everything mapped, now the challenge is to take the dancer’s shoe thinking of measures that can mitigate the removal “from this allowance that costs between $ 3 and 4 billion, about $ 2.8 to 3.7 billion euros, per year. “It is a considerable value, given that the Integration and Intervention Program in the municipalities (PIIM) has 2 billion, so it would be two PIIM. ”[2]

It seems, therefore, that the IMF and Vera Daves are determined to eliminate fuel subsidies, apparently they do not know yet is how.

The political issue and the mechanism of transparency

It is evident that these eliminations, even making sense economically, and we will already address doubts in this context, have a large political impact and cannot be viewed as a “lightweight”. From Egypt to Iran to Sudan, France, changes in fuel prices have impacts on political stability, so the first assessment to do is political.

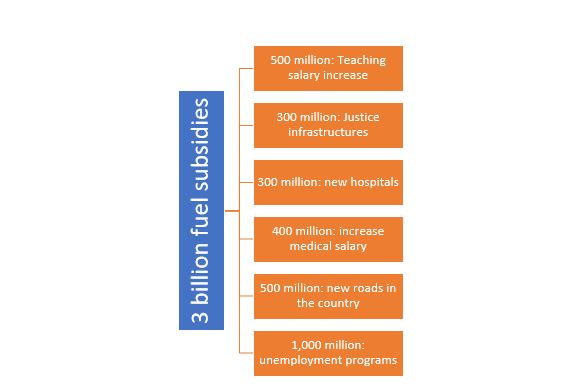

The great argument advanced by Vera Daves is the one that technically is called Crowding Out. By spending 2.8 to 3.7 billion euros, a year on fuel subsidies, the government does not spend them in the social sector, in education and health, for example. In fact, she argues, what is put in the lowering of the price of gasoline is taken from the well-being of the people. Accepting the argument, it must be sustained and convince the population. Accordingly, the first task would be to create a transparency mechanism (perhaps in the form of a digital site) that explained to the population how the background of subsidies would be channeled to other sectors, clarifying government plans. 1000 million for schools, 500 million for teachers, etc. Making a simple scheme and spreading it, everyone would realize the fate of money, and then over the early years there should be a public presentation of this flow. It would be explained by a scheme where the savings had gone with the removal of fuel subsidies. Consequently, the population would see that it had not been invented by the Minister of Finance, but that it was effectively happening.

A first preparatory measure of political nature is the creation of a transparency mechanism for all consultable to explain the path of money, how much it comes out of fuel subsidies and where it will end up in the various sectors of the budget. Thus, the population sees the benefits.

Fig. No. 1- Example of the transparency mechanism of the flow of funds taken from the subsidy to fuels, to be presented annually to the population

The problem of market structure

Entering the economic area there is a question that is raised and should be confronted. It is evident that the termination of fuel allowance will increase their prices.

In 2021, there were 951 gas stations in Angola, of which 432, would be controlled by small operators without brand. Sonangol Distribuidora is the largest in the distribution segment with a market share (sales) of 64%, Pumangol is the second largest player with 24% and the remaining 16% are distributed by Sonangalp and Tomsa (Total Marketing and Services Angola)[3].

The question is the definition of the structure of this market. A first analysis could appear to be facing a competitive market, but the weight of Sonangol and Pumangol, representing a total of 78% of sales market quota indicates that we are facing an oligopolistic type market, where few companies dominate the sector. It is known to price theory that oligopolistic markets have higher prices than perfect competition markets, where no one dominates the market. The oligopoly price is fixed by companies above the price level that would prevail in competition and below the monopoly profit maximizing price level. It is a market structure that constitutes a intermediate case, where there are few companies that compete with each other.[4]Consequently, removing the subsidy of fuel prices in an oligopoly situation would be equivalent at a higher price than the market equilibrium price and to put the population to finance higher profits from fuel distribution companies.

It is fundamental while the gradual withdrawal of prices begins to increase the number of relevant operators in the market and put them to compete with each other, without anyone mastering the market.

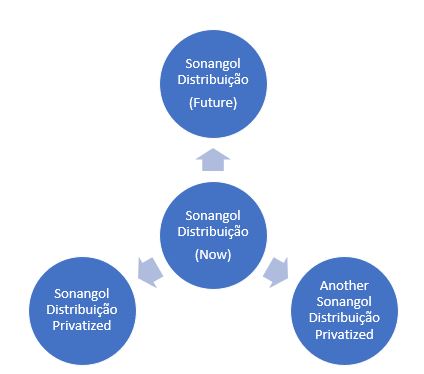

The most advisable was to split Sonangol Distribuidora in three different companies and immediately privatize two of them. Thus, we would have at least 5 relevant operators in competition.

Fig. No. 2- Sonangol Distribuição Scheme to ensure competition in the market

Forms of compensation/mitigation of the removal of subsidies

Described was the need to create a fund flow transparency mechanism for political consensus purposes, as well as the need to reform the market structure of the Downstream segment as a way to prevent oligopoly price formation, that is, higher than normal, it is time to make suggestions for compensation for the removal of subsidies.

The starting point is that there will be no savings of all values pointed out as a cost, 2.8 to 3.7 billion euros per year, and that there are sectors and populations that must be protected. We speak, of course, the populations with less income and the areas of transport and food and agricultural distribution.

Measures can start from various focuses:

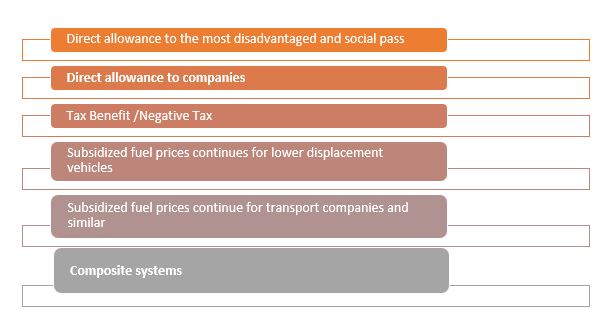

a) Focus on the subject

AA) direct subsidy to the most disadvantaged and social pass

AB) direct allowance to companies

AC) Tax Benefit /Negative Tax to AA) and AB)

b) Focus on the object

BA) Subsidized fuel prices continues for lower displacement vehicles

BB) subsidized fuel prices continue for transportation companies and similar

c) Composite systems

Explaining each of the items and possibilities. We would have the following:

a) Focus on the subject

AA) direct subsidy to the most disadvantaged and social pass

A first hypothesis would be the granting of a fuel subsidy to all those who had a vehicle and/or used fuel in a given activity and showed an income below a given level. This wanted to say that the citizen who used fuel and had low income would receive a direct subsidy of the state in order to alleviating the negative effects of the price of fuel climbing.

In addition, a reduced social pass could be created, allowing any citizen to use transport without repercussion of the amount of fuel climb.

AB) direct allowance to companies

Another hypothesis would be that of direct allowance to transport and distribution companies. So that they did not reverberate the price of fuel in prices charged to the public, there would be compensation paid by the state that would cover the differential. Companies would receive funds so as not to increase prices.

AC) Tax Benefit /Negative Tax to AA) and AB)

In this situation, the instrument used for compensation would be the fiscal system, not the direct transfers of subsidies. It would be allowed to natural persons to a certain level of income and the companies of the affected sectors presented as tax deduction the value of the differential paid with the rise of prices. For example, if they previously paid 5 and then they would pay 10, they would have the opportunity to present an amount of 5 as a fiscal deduction, paying a lower tax.

In a superficial situation, such a deductive possibility would only apply to entities who paid tax, leaving out those who do not pay or are exempt. In these cases, a negative tax should be made, that is, a system through which low-income people would receive supplementary government payments rather than pay taxes. These supplementary payments would be equal to the additional amounts spent on fuel by these people.

b) Focus on the object

BA) Prices of subsidized fuel continues for lower displacement vehicles

In this hypothesis, what would happen would be the establishment of different levels of price for fuel according to the displacement of vehicles. Low-displacement vehicles would pay a lower price and vice versa. It would be a kind of progressive price.

BB) subsidized fuel prices continue for transportation companies and similar

In this case, the system would be the same as indicated above, with the difference that the beneficial price would be applied to the vehicles of transport companies and similar.

c) composite system

It is evident that the above systems can be mixed or complemented by each other, and it is up to the political decision-making to find the best technical combination.

Fig. No. 3- Possible compensatory solutions for the removal of subsidies to fuels

Need for financial calculations

There are no financial calculations in this work because the numbers are not known. The Minister of Finance presents an order of magnitude of current spending quantity with fuel subsidy, which is between 2.8 and 3.7 billion euros per year. Easily it is found that the differential is too large (900 million euros) to do a finer arithmetic of the situation.

[1] IMF, STAFF REPORT FOR THE 2022 ARTICLE IV CONSULTATION, February 7, 2023, p. 7.

https://www.cedesa.pt/wp-content/uploads/2023/03/subs-combustiveis.png380750CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2023-03-19 12:04:002023-03-15 12:24:52Conditions and solutions for the removal of fuel subsidy in Angola

Social life in Angola is very alive and, at this moment, political and judicial matters dominate the country’s agenda. However, it is in the domain of the economy that there is an extremely significant evolution on which it is important to reflect and proceed to a careful analysis.

The recent (February 2023)[1] International Monetary Fund (IMF) report on the country underlines the favorable advances of the Angolan economy and also the necessary reforms. It is based on this report that we will enunciate Angola’s main trends in the economic field and the neuralgic points to avoid relapses such as the last long recession that began in the presidency of José Eduardo dos Santos.

Positive Trends

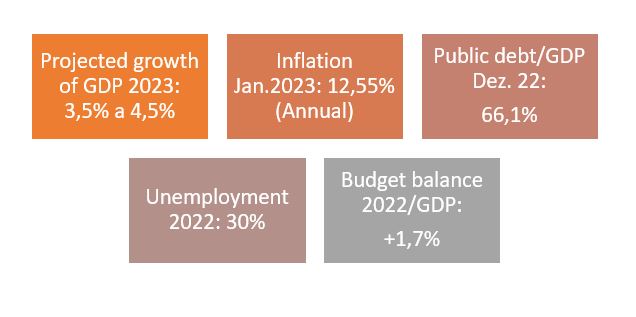

Angola’s economy is in full recovery after the five-year recession (2016-2020). By 2022, supported by higher oil prices and resilient non-oil activity, it has already reached growth of more than 3%, estimating the IMF that by 2023 the country continues to see the GDP increase in the order of 3.5%.

Therefore, we see growths of over 3% per year, which by our calculations, maintaining the price of oil and accelerating the liberalization of Angolan markets and foreign investment, could accelerate to numbers of 4% or 5%, adopted that are the right policies.

The optimism we share here results from the fact that non-oil growth has been widespread, despite a difficult external environment, as it means that the non-oil sector is reviving, as well as the attention that several developed countries with market economies are providing Angola, as is the case of US, Spain, France and Germany. Mentions should be made to recent visits to Angola of the King of Spain and the President of the French Republic, Emmanuel Macron (February and March 2023).

It should be noted that the debt that the public debt/GDP ratio has dropped about 17.5 percentage points of GDP, for an estimated 66.1% of GDP, aided by a stronger exchange rate. It is estimated that the checking account remained with a large surplus in 2022, while coverage of foreign currency reserves remained adequate (IMF data).

The fact is that the Angolan government has, according to the IMF, to adopt and maintain solid macroeconomic policies and maintained a commitment to structural reforms that are vital to Angola’s economy.

Necessary reforms

We understand that it is in the verification of fundamental structural reforms that resides the future of the Angolan economy. We highlight some reforms that are necessary to take and/or continue.

1-First renovation, with impact on the medium and long term, is to foster training for the economy of young people. Training not only means, and perhaps not in most, university education, but solid training in basic education and in professional aspects. We argue, therefore, that there must be an effective bet on vocational and technical education in Angola, before any other. A real bet on professional and technical schools and institutes, which are seen as valuable alternatives to academism and not mere university imitations (tragic error of Portuguese polytechnics).

2-Second renovation entails the creation of more conditions for investment, no longer at the legal level, where there is a modern framing and updated twice during the presidency of João Lourenço, but at the judicial, administrative and good practices level. The investor must feel safe to arrive in Angola and apply his money. One should not be afraid of being without the money due to any interference from an oligarch, or see any process dragging on in court. The speed and impartiality of justice is linked to good investment.

3-Third reform is dedicated to the financial sector, there is a special emphasis on increase credit to private persons and and the resolution of banking weaknesses. Quickly we must merge and capitalize banks, creating a banking sector not dependent on the state, clientelism or mere public debt management.

Finally, among other reforms, we highlight the true imperative of making more progress in strengthening governance and transparency, to improve the business environment and promote private investment.

Of course, continuing and accelerating anti-corruption strategy is also important.

National Employment Plan

All these news should be framed with the well-being of the population and the serious problems still pending. The one we highlight is unemployment, which although noting a slight descent, is still very high, about 30% [2]. This is an area in which we advocate direct state intervention. It is evident that the increase in GDP corresponds to an unemployment decrease, however, we believe that in the face of such high unemployment, in the short term the immediate action of the government is fundamental.

In this sense, the recent announcement of the World Bank of US $ 300 million for a project to accelerate economic diversification and job creation[3] is to greet. Not knowing in detail the design of this acceleration program, its existence should be underlined, as well as the previous announcement of the Angolan Labor Minister of the creation of a National Employment Program, with the aim of creating more opportunities for insertion of young people in job market[4]. Also, in this case, the data are scarce about the design of the plan, and it is certain that the President of the Republic had declared in the discourse of the State of the Nation of 2022, the creation of the referred plan.

So far, these initiatives related to unemployment, although positive, seem uncoordinated and poorly implemented. Therefore, the truth is that Angola would win to see a comprehensive national employment plan, specific and directly coordinated by the President of the Republic, without the risk of not properly implemented a plan, which in the short term is fundamental to the economy and Angolan population.

https://www.cedesa.pt/wp-content/uploads/2023/03/econ2.jpg6581006CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2023-03-17 13:53:002023-03-13 18:59:13Angolan Economy trends, necessary reforms and national employment plan

1-Introduction: IMF, sound economic policies and capital accumulation

Contrary to what some economic studies and forecasts currently carried out by some more or less unknown consultants, the current Angolan economic policy has solid foundations. This is demonstrated by the recent assessment by the International Monetary Fund regarding the agreement between the fund and Angola. The IMF administration is clear in declaring[1]: “The authorities [from Angola government] have supported the [economic] recovery through sound policies that aim to further stabilize the economy, create opportunities for inclusive growth and protect the most vulnerable in Angolan society.”

It would be difficult to have a better endorsement of government economic policy.

However, macroeconomic stabilization and the resumption of economic growth are different realities. There is need of a certain engine to ensure economic growth. It is known that the essential growth model was presented by Robert Solow (Nobel Prize for Economics in 1987), that explains that growth depends essentially on the accumulation of capital, with the increase in GDP resulting from the increase in the capital stock[2].

It is known that the latest Angolan GDP figures for the first quarter of 2021 are negative by 3.4%. So the question that now arises is: how to transform sound economic policies into capital accumulation and promote GDP growth?

2-Capital in the Angolan economy

The essential growth model of the Angolan economy, at least from 2021 onwards, was not a model based primarily on investment, but on consumption derived from imports and on the direct benefit of capital gains from the high price of oil. This meant that the investment that existed was induced by oil and not extended to the economy as a whole[3]. It should also be noted that a good part of the savings gains at that time was not transformed into domestic investment, having been transferred abroad from Angola. In a colloquial way, there was a sharp flight of capital from Angola to overseas countries, namely Portugal or off-shore tax havens[4].

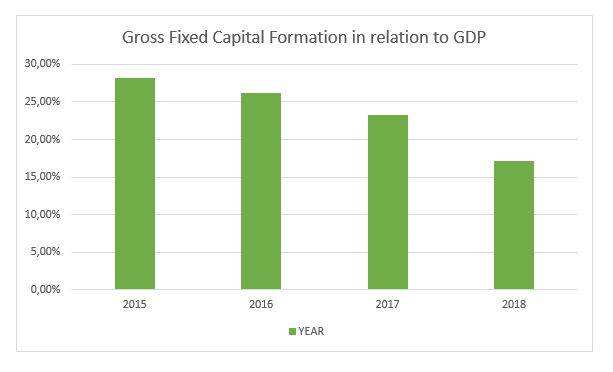

It is public that this model went bankrupt as of 2014, and led to sharp years of recession after 2015. At the same time, it was found that the contribution of gross fixed capital formation (GFCF) to GDP began to decrease from that point on. year (2015). If we look at each year the FCF/GDP was respectively 28.21 %, 26.21 %, 23.24 %, 17.19%. The 2018 number (17.9%) is frightening and makes the discussion about the need to capitalize the Angolan economy more relevant.

Figure 1: Gross Fixed Capital Formation in relation to GDP

“The country has a capital deficit”[5] and this problem has to be resolved so that growth can occur. This aspect has to be one of the guides for future economic policy. A goal must be set to raise the GFCF/GDP rate to higher levels, possibly to the 25/26% that happened in 2007 or 2012, which ensure GDP growth levels (albeit based on oil) of 14% and 8%. Now a new capitalization not only based on oil has to be carried out.

It’s easy to diagnose. Angola lacks capital and needs strong investment. The answers will be the most costly.

3- Increase capital in Angola

What to do to accumulate and increase capital in Angola?

Our answer is divided into two perspectives, the short-term and the medium-term. Let’s focus on the short term, then make a brief reference to the medium term, although it is clear that there is a continuum, as what is done now has repercussions over time.

The executive has already taken some measures, which we have reported in previous reports[6], such as the Private Investment Law (LIP)-Law no. 10/18, of June 26, which no longer requires partnerships with Angolan citizens or companies from Angolan capital and in its article 14, it guarantees that the State respects and protects the property right of private investors; Article 15 establishes that the Angolan State guarantees all private investors access to the Angolan courts for the defense of their interests, being guaranteed due legal process, protection and security. The range of possibilities for transferring dividends were also expanded. Moreover, in administrative terms, it should be noted that in 2018, all requests for the transfer of dividends above five million dollars (4.3 million euros) were granted to foreign companies operating in the country. And, most importantly, since 2020, the capital import from foreign investors who want to invest in the country in companies or projects in the private sector, as well as the export of income associated with these investments, have been exempted from licensing by the Angolan central bank.

However, this is still not enough, and foreign private investment will take a long time, either because a very turbulent electoral period is starting, or because there is a worldwide distraction with Covid-19. In addition, the executive has not yet communicated with all the worldwide amplification, the opening of Angola for business. Even so, it is essential that the executive maintain the political orientation of openness to foreign direct investment.

More needs to be done in the short term to increase investment in Angola and subsequent economic growth. Below is a list of suggestions.

• The initial suggestion is obvious and is based on strengthening public investment. It is essential that the government becomes an inductor of investment and that the capital gains arising from the rise in oil prices and possible apprehensions in the fight against corruption are applied in reproductive investments with short-term results.

The next two suggestions might be more innovative.

Let us address the first of the most unorthodox suggestions. As mentioned, a good part of the savings obtained by Angolans in Angola was remitted abroad, decapitalizing the country. Now we have to reverse this.

• In this sense, the government should, in the first place, sell the dormant shares and assets or in which there is no very relevant strategic interest, which it has abroad. With the result of this sale, it would constitute an investment fund to be invested within Angola. Thus, the first heterodox proposal to increase the capital available in Angola is to sell what there is abroad that belongs to the State (directly or indirectly) and place it in the Angolan economy. Certainly, Sonangol’s position in Millennium BCP should be sold and transformed into investment capital in Angola, and possibly an indirect stake in Galp, if it is not possible to reach a strategic agreement with the Amorim family to better monetize the Angolan position.

• The second suggestion refers to fighting corruption. It is necessary to get out of a certain delay that entered into and boost the capital recovery.

Thus, the government should directly approach those it calls “hornets” and propose a negotiated solution to their situation. Either they deliver the assets that are abroad for investment in Angola, or they will face long prison terms. In relation to these assets, the method outlined above would be followed: Provided market prices were acceptable, everything would be sold and the capital returned to Angola for investment according to a formula agreed between both parties.

This “negotiation” would not be carried out by common means, but by a specialforce to be set up in Angola and would have short deadlines, not judicial deadlines.

There will have to be a radicalization in both directions in the fight against corruption. More effective punishment or forgiveness with repatriation. Unlike what happened in the previous repatriation law, there would be no waiting, but there would be a proactive attitude on the part of the executive.

By way of an illustration, the participation of Isabel dos Santos in NOS, that of General Kopelipa in the BIG bank and in several hotel developments, the apartments that the former figures have in Estoril, etc., could be sold. The result of these sales would return to Angola where it would be invested in terms to be agreed between the State and the former owners.

These listed measures could give some boost to the Angolan economy and thus promote economic growth immediately.

At the medium-term level, the essential thing is that there is no rampant corruption, good communication infrastructures are created, an investor-friendly legal apparatus and fast, non-corrupt courts, an educated workforce (this does not mean having degree courses but the necessary skills) and reasonable taxes. In short, an inviting political and social climate for investment.

https://www.cedesa.pt/wp-content/uploads/2021/09/capital-angola-1.jpg10801920CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2021-09-17 13:52:002021-09-15 13:53:50The question of capital in Angola

The latest figures available from the National Institute of Statistics on the Angolan economy point to a decrease in GDP in the 1st quarter of 2021 in the order of -3.4%, an unemployment rate in the same quarter of 30.5%, and a annual inflation rate for the month of July 2021 of 25.72%[1]. None of these figures that reflect macroeconomic magnitudes are encouraging in the short term.

However, there are other economic and financial realities to consider in order to have a global view of the movement underway in the Angolan economy, and which allow for a more optimistic perspective.

To begin with, in terms of the budget balance and public debt, essential elements of the support program of the International Monetary Fund (IMF), the expectation is that the 2021 budget balance will be positive, possibly above 2% of GDP (further on we will present our prediction). In relation to public debt, as we had predicted in previous reports, its sustainability is consolidated, as recognized by the IMF representative in Angola very recently (see our forecast below)[2].

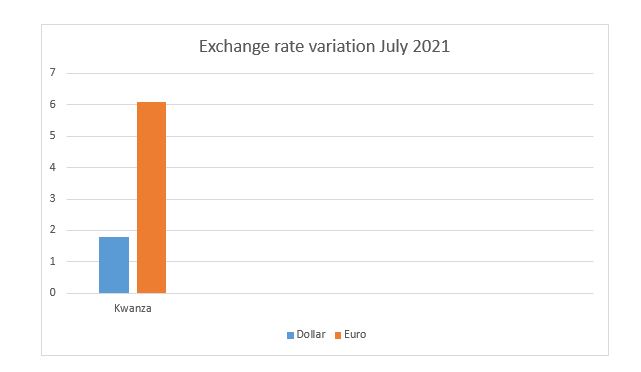

In terms of exchange rate with reference to the month of July 2021, the Kwanza has already appreciated 1.8% against the dollar and 6.1% against the euro, since January 2021, breaking a strong period of strong devaluation started in 2018. Furthermore, 3.5 years after exchange rate flexibility, the gap between formal and informal market rates is below the 20% target announced by the central bank at the time of liberalization, between 7% and 8% for the dollar and euro respectively. Note that at the time prior to liberalization, the same gap was 159% and 167%.

Figure 1 – Kwanza Exchange Rate Variation against the Dollar and Euro (July 2021)

Currently, some sectors are already announcing an increase in the profitability of exports due to the favorable exchange rate policy. This is the case of cement, where Pedro Pinto CEO of Nova Cimangola assures that “To boost exports, the devaluation of the currency helped, because all the costs that the company has in national currency, in dollars, were lower and, in this way, the competitiveness of the company to place products on the international market. In other words, all those products that we continue to buy in Kzs and that have not suffered large price variations in dollars were lower and, therefore, allowed the company to have greater profitability with exports.[3] ”

Also a reference to PRODESI (Program to Support Production, Diversification of Exports and Substitution of Imports), which has generated more than USD 29 million since the beginning of the year. As the main exported products, emphasis is placed on cement, beer, glass packaging, bananas, juices and soft drinks and sugar[4].

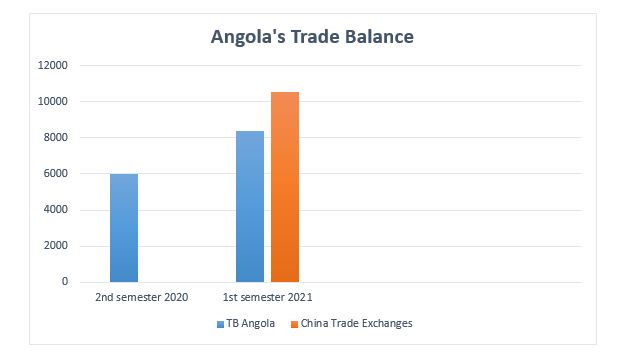

These movements are reflected in the trade balance. Angola’s trade balance recorded, in the 1st half of 2021, a surplus of USD 8,381.9 million[5], an increase of 40.2 % compared to the results recorded in the 2nd half of 2020 (USD 5,978.8 million)[6]. Within this framework, there was an increase in exports of 25%, naturally still influenced by the increase in exports from the oil sector of 28.4%.

Figure 2 – Angola’s Trade Balance and Trade Relations with China

But there is also a significant increase in trade with one of Angola’s main trading partners, China. “Trade between Angola and China increased 23.9% in the first half of 2021, to US$10,550 million (€8,985 million), compared to the same period last year”[7]. According to Gong Tao, Chinese ambassador to Angola, despite the adverse effects caused by the covid-19 pandemic, Chinese companies remain interested in investing in Angola, highlighting the recent construction of factories, one dedicated to the production of tiles and another qualified for the production of energy and water meters.

2021 Summer Forecasts

In modeling the perspectives we present here, several factors are taken into account, among which we highlight the main ones. The first element is the calculation of the oil price (always a determining factor in the Angolan economy). We assume that the price of Brent will maintain a slight upward trend, standing at a level between USD 65 to USD 75 per barrel. A relative stabilization or possible appreciation of the Kwanza against the dollar and the euro is also part of our model, which makes it possible to reverse some of the falls in the past that were merely nominal due to the more flexible exchange rate. We anticipate that the post-Covid-19 world recovery will boost the Angolan economy’s exports, as is already happening with China. Finally, we anticipate that the environment for foreign investment will gradually improve as a result of legislative reforms and the commitment of political power. We have as a recent example the several advertisements coming from Turkey. At the end of July 2021, Angola and Turkey signed 10 cooperation agreements, in the fields of economy, trade, mineral resources and transport, having already announced an increase in the trade balance with Angola to a value of around USD 500 million[8].

From the point of view of obstacles, it is worth mentioning the immense lack of capital. This is the main element for any sustained recovery, and also the inexistence of economic diversification[9] and the persistence of administrative bureaucracy.

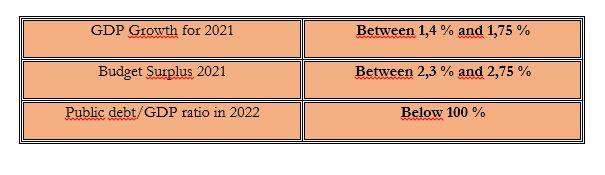

All things considered, our model predicts that by the year 2021 the Angolan economy will come out of recession, and GDP growth will reach between 1.4% and 1.75%.

Our model points to a budget surplus between 2.3% and 2.75%, depending on the evolution of the oil price until the end of the year. And considering the evolution of the Kwanza exchange rate, our forecast is that in 2022, the public debt/Gross Domestic Product (GDP) ratio will be below 100%, achieving greater consolidation.

Figure 3 – CEDESA Model – Forecasts for the Angolan Economy

Consequently, the initial period of strong adjustment and contraction of the Angolan economy is expected to come to an end this year, with no more shocks and global control of the Covid-19 pandemic.

The special case of Unemployment

We understand that unemployment is a special case that should be treated differently, both statistically and in terms of public policies. In terms of statistics, it should be better ascertained who is occupied with informal productive paid activities and who cannot effectively obtain any paid work they want. We should avoid statistical biases that disturb the proper understanding of reality.

On the other hand, it is clear that it will not be the market or the private economy that will solve the problem of lack of employment in the short term, especially for young people. To that extent, the authorities are urged to develop a Keynesian-type employment promotion program, if necessary using available capital from the fight against corruption, as we have advocated in other reports. The state has to spend money on job creation.

https://www.cedesa.pt/wp-content/uploads/2021/08/economia-angola-1.jpg10611920CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2021-08-30 10:20:372021-08-30 10:21:13Indications and Summer Forecasts for the Angolan Economy

At the moment, when we finish this report, the President of the Republic of Angola is in Paris with the President of the French Republic. This meeting represents one of the points in the ongoing realignment of Angola’s foreign policy. One has only to remember that in the last days of José Eduardo dos Santos, the French were “punished” due to their role in Angolagate.

Angola is not an indifferent country. It has played a geopolitically relevant role throughout its short but intense history after independence. First, it was one of the violent stages of the Cold War, where Americans and Soviets clashed with the virulence that they could not adopt in other geographic locations. Angola ended up being a Soviet bastion of great nomination, where they in reality won when in confrontation with the United States. After the Soviet phase, Angola was once again innovative and became the first African country to receive the new China that opened up to the world and sought in Africa a continent for its expansion and testing of its ideas. Angola has become a partner par excellence of China.

Obviously, this being a simplification, from the point of view of the major trends, the geopolitical position of Angola started to be aligned with the Soviet Union and after its fall, with China. Not being a country that is enraged anti-Western, very far from that, because Angola has a profound influence of European culture, the country has anchored itself in other places over time.

For several reasons, at this moment, Angola is rehearsing a different geopolitical approach that tends to devalue the role of both Russia and China, and to find new references and political dialogues. This text will focus on this devaluation, the new vectors that influence the Angolan repositioning, the countries that will now play a more relevant role in Angola’s external concerns, in addition to a short note on Portugal. Angola’s influence in southern Africa and its stabilizing role in Congos will not be addressed.

2-The decline of the Angolan relationship with Russia and China

The decline in the Soviet (now Russian) relationship with Angola is easy to describe. The Soviet Union’s commitment to Angola was part of a long-term strategy for the involvement of the North Atlantic through the countries of the South. The incursion into Africa that was accelerated by the “loss” of influence in the Middle East in the 1970s due to the cut promoted by Sadat from Egypt and by the Kissinger’s full exploitation. Suddenly, the Soviet Union found itself without one of the main supports it had in the Middle East and from where it hoped to condition the Americans. What is certain is that this situation led to a deepening of several alternatives, among which Angola later stood out. Naturally, the fall of the Berlin Wall in 1989 and the end of the Cold War, with the consequent disintegration of the Soviet Union, meant that Russian interest in Africa waned considerably. The Russia that emerged after Gorbachev’s collapse was no longer interested in any global competition with the United States, but in its survival and transformation. He quickly lost interest in Angola.

It is true that at the present time, Putin has recovered some of the imperial dynamics and is looking for some influence in Africa, but it is still of short reach and has resulted in the sending of mercenaries from the Wagner group, which have had little efficiency, namely in Mozambique. In Angola, there is no significant behaviour by Russia, especially as an essential and determining partner. There are obviously contacts and relationships. There is a lot of talk about the Russian influence on Isabel dos Santos, who might be a citizen of that country, but the fact is that there are no visible Russian investments or ties with Luanda with obvious relevance. In 2019, Russian investments in Angola of 9 billion euros were announced, but there is no known sequence of that. In addition, Angola’s external public debt to Russia is zero according to data from the National Bank of Angola (BNA), having been fully settled by 2019.

It is more difficult to wind up the declining relationship with China. In fact, Chinese investment in Angola has been growing, at least until 2020, and the Angolan external public debt vis-à-vis China in 2020 represented US $ 22 billion, equivalent to more than 40% of the total. The Chinese implantation in Angola is profound, suffice to mention in sociological terms the relevance of the City of China.

However, there is evidence that the Chinese preference is decreasing, or at least, being mitigated. The first indication refers to the negotiations for a new loan that took João Lourenço to China at the beginning of his term. The first information for the press reported large amounts to be made available by China, of around 11 billion dollars. The reality is that there were several procrastinations on that loan, which apparently ended up involving a reduced amount of US $ 2 billion that might have suited to make payments of Angolan debt to Chinese companies.

What is certain is that if we observe the evolution of the Angolan public external debt to China, we will see that there was a remarkable leap between 2015 and 2016, from about US $ 11.7 billion to US $ 21.6 billion, which the debt reached the peak in 2017, 23 billion dollars and that since then has been decreasing with a significant cadence. It seems that China does not want to be involved with Angola any more, preferring to go on managing the current involvement.

If on the part of China it is possible to glimpse some recalcitrance in the relationship with Angola, on the Angolan side there are also obstacles. The first of them is the nature of the Angolan debt to China. Many claim that a good part of this debt is what is called “odious debt”, that is, it served to benefit corrupt private interests and not the country’s development. There is the impression that the opacity with which doing business with China has allowed the creation of situations of corruption that are too evident and harmful to the country. Thus, China’s debt is partly seen as a debt of corruption. In addition, quality problems have arisen in some Chinese buildings in Angola financed by Chinese debt. It is not clear whether this lack of quality is due to any Chinese negligence or objectionable behaviour on the part of Angolan officials, but it is certain that the image persists.

This means that since China is still a key partner for Angola, it is currently in a kind of reassessment phase. It is necessary to resolve the problem of the debt of the past linked to corruption, of the way of contracting too opaque on the part of China and also issues related to quality. It is a demanding task, but required to reactivate the Chinese and Angolan common interest.

If the relationship with Russia does not have the relevance of the past and with China is in a phase of reevaluation and reconditioning, it is clear that Angola, above all, given the changes as it passes, will have to actively seek new partners.

3-The new vectors of Angolan action: goals and countries

The Angolan relationship with Russia and China concurred with the need to assert its own sovereignty, independent of external interference, and also to obtain funds for war and post-war reconstruction. João Lourenço’s current foreign policy is placed at a slightly different level, in which it is important to gather external support for the two major reforms that are being carried out internally: economic reform and the fight against corruption. Both reforms need external collaboration, without which they may not survive.

Economic reform is based on the so-called Washington consensus proposed by the International Monetary Fund (IMF), although international intellectuals and bureaucrats have already abandoned this designation and refuse it. Even so, it implies the adoption of policies to raise taxes and restrict expenditure with the respective fiscal consolidation. Naturally, this type of policy is recessive, in the short term, it increases the economic crisis in Angola. The great way to overcome this effect is to obtain foreign investment and a lot. In fact, says the theory followed, that with these disciplinary reforms of the IMF, foreign investors start to trust the governments that follow them and feel safe to invest. In short, foreign investment is the necessary counterweight to the IMF reforms and the key to their success. Consequently, it is not surprising that one of the main vectors of Angolan foreign policy is the approach to countries with a remarkable reproductive investment capacity and with proven evidence.

In what concerns the fight against corruption, the panorama that is presented is that, in general, it is the countries with the potential to invest in Angola, those in which judicial collaboration is required to recover assets or trace illegal financial movements. The Angolan oligarchies that diverted public funds sent them to the most advanced countries or those with the greatest financial potential.

Therefore, there is a group of countries that currently are of great interest to Angola: they are those with an efficient investment capacity and with a financial system through which many of the illicit movements of Angolan funds have passed, as well as where assets bought, possibly with these funds. At the moment, neither China nor Russia are countries where more investment is expected, nor were the places chosen, apparently, to park illicit goods or assets. Or if they were, there is no knowledge of what is going on there and it is sheltered.

It is in this context that a number of countries have assumed relevance. A first group is the Western Europe countries that have stood out in visits and announcements of investments in Angola. At the beginning of April 2021, the Prime Minister of Spain, Pedro Sanchez, paid a visit to Angola. This visit was accompanied by a great Spanish commitment, affirming Angola as one of Spain’s preferred partners in Africa, and this as a great Spanish bet. It was announced that Angola was the “prow” of a project in Madrid that he called “Focus Africa 2023.” Last year, it was the turn of German Chancellor Angela Merkel to visit Angola within the framework of an Angola-Germany Economic Forum and more broadly of a German Marshall Plan for Africa. Also, President Macron announced a visit to Angola, which has been postponed due to Covid-19. In turn, the Italian President had already visited Angola in 2019. In relation to the United Kingdom, there have been no visits of such high level, but some interest in Angola is beginning to be noticed due to the impositions of Brexit, which they demand new markets for the UK, although there is a huge lack of knowledge.

Visits have followed several promises of investment from Western Europe. The Italian oil company (ENI) plans to invest seven billion dollars (5.9 billion euros) over the next four years in research, production, refining and solar energy, it announced in early April 2021. Before, British businessmen said they intend to invest around US $ 20 billion in Angola. Germany and France also have several projects underway.

This axis of Western Europe has become vital in Angolan foreign policy, as these countries need new markets and investments, to get out of excessive dependence on China, and in the British case, also to look for post-Brexit alternatives, and being mature markets, they have to find out where the youth and the future is, and that is in Africa.

With João Lourenço able to convey the image that governs a competent government and with stable macroeconomic rules and turned to the free market, Spanish, French, British, Italian or German investors will feel safe to invest. At the same time, many of the fortunes out of Angola lay there, so there will be an opportunity to create mechanisms for their recovery or redirection.

It should be noted that, contrary to what one might think, this Westernization of Lourenço’s foreign policy does not pass through Portugal, but indicates a direct approach between European countries and Angola and vice versa.

To this Western European axis it is necessary to add another one, the Gulf axis. The Gulf countries, in which the United Arab Emirates and Saudi Arabia stand out. These countries, previously dependent on oil, have entered into a diversification policy. Dubai for some years now and with tremendous success. Saudi Arabia is still taking its first steps, with the so-called Vision 2030, but what is certain is that they want to invest outside their traditional scope and find new markets. In fact, Dubai already has several investments in Luanda and one of its companies has now taken over the Port of Luanda and in Saudi Arabia, Luanda has now opened an Embassy, which reveals its interest in the kingdom. On the other hand, we know, Dubai is a quite important international financial center and where several Angolan financial movements have gone through, as well as being used in tax evasion schemes in the diamond trade. Allegedly, contrary to what has been its practice, Dubai will be collaborating with requests for Angolan legal aid, representing a typical example of the new geopolitical axis that we are describing, countries with potential for investment and judicial collaboration in the fight against corruption.

In summary, we conclude that a new Angolan geopolitical approach focuses on the countries of Western Europe and the Persian Gulf. But it doesn’t stop there.

4-India’s potential

The amount of trade between Sub-Saharan Africa and India has grown steadily, and today India is a key trading partner for Africa. With regard to Angola, the country is today the third most important exporter in sub-Saharan Africa to India, when in 2005 it was irrelevant. In 2017, the Ambassador of India issued a statement in which he highlighted: “Trade between Angola and India increased 100% to US $ 4.5 billion in 2017, (…) At the end of July, outside the 10th BRICS summit , in Johannesburg, the President of Angola, João Lourenço, met with the Indian Prime Minister, Narendra Modi, and the two reaffirmed the need to increase trade and cooperation in areas such as energy, agriculture, food and pharmaceutical processing. ” As India grows and becomes a very important player worldwide, it is normal for Angola to look at this country with a new vision. It is a millionaire market to which an immensity of Angolan exports can reach.

5- The United States of America. The ultimate prize

The relationship between Angola and the United States has been ambiguous. In fact, even in the days when the US administration supported Jonas Savimbi and UNITA, there was a relationship with Luanda linked to oil and the protection of American multinationals operating in territory dominated by the MPLA government.

Currently, the United States represents everything Angola wants, the country of the dollar with an enviable investment capacity and financial innovation, with a universalizing legal structure that allows it to use multiple legal instruments around the world to pursue the fortunes of corruption. It is also from the United States that Angola needs to raise the various “red flags” that were erected during the time of José Eduardo dos Santos and made Angolan financial life much more difficult. The United States is the key country for this new Angolan phase of foreign investment and fight against corruption, because from here the definitive stimulus for progress can come.

In a way, João Lourenço was unlucky to come across Trump when he needed the USA. It is known that Trump had no interest in Africa, that he only served for his wife to take a trip in colonial style attire. Worse would have been impossible. But American indifference does not have to be an obstacle to a greater Angolan commitment to relations with the superpower. In the early 1970s, Anwar Sadat from Egypt also decided that he wanted to get closer to the United States. These occupied with a thousand and one crises, among which Vietnam stood out, paid no attention to Sadat, who continued to follow his line, expelling Soviet advisers and starting a rapprochement with the Americans.

Historical comparisons and evolutions aside-Sadat ended up murdered for having signed a peace agreement with Israel on American auspices- what seems more logical for Angola at this stage is to accentuate a closer relationship with the United States, even if they are not attentive. And they won’t be, because between Covid-19, China and Russia, and multiple small internal crises have a lot to deal with. However, effective and real US support for the new Angolan policy is essential for the country to come out of the doldrums and no longer have external financial constraints, so a vigorous approach to the US administration would be advisable on the part of Angola, despite of the mutual distrust that exists.

6-Portugal is different

Regarding the visit of Pedro Sanchez, Spanish Prime Minister, Angola came up with some criticisms of the Portuguese government, accusing him of inaction and of being overtaken by Spain. This is nonsense. Not even Portugal can think of having a monopoly on relations with Angola, nor is there any danger in Portuguese-Angolan relations. Portugal is always a separate case, its influence comes less from the government and more from soft power, from the umbilical connection that remains between the peoples of both countries. Luanda continues to stop when Sporting wins the championship or Benfica have a very important game, the favorite destination of most Angolans is Portugal, easy personal relationships are established between Portuguese and Angolans. Portuguese businessmen always look to Angola as a possibility for expanding their business. The relations between Angola and Portugal have an underlying relationship between the peoples before the intervention of the governments.

At the official level, the Portuguese government is generally welcoming towards Angola. Around 2005, he welcomed the wishes of Angolan investment, currently he accepted the requests for judicial cooperation from Angola in relation to Isabel dos Santos, as it ended up sending Manuel Vicente’s case to Angola after great pressure from Luanda. Let’s say there is a manifest porosity of the Portuguese position, easily adapting to the positions and needs of Luanda. This position, combined with the interest of the Angolan elites in Portugal, has ended up consolidating a good relationship between the two countries, despite a bump or two. It is clear that after April 25, 1974, Portugal lost interest in Africa, making its accession to Europe and becoming a modern western country its number one priority. This project has been a little tangled since 2000, but it has not led Portugal to a revision of its European focus yet, it only forced it to take a longer look at Africa, after decades of disinterest. Perhaps there is a time when Portugal wants to focus its foreign policy on Portuguese-speaking countries, but this is not the time, as it is not for Angola, which wants to embrace other “voices”, such as the English-speaking and French-speaking countries, thus, the best that governments can to do is to make life as easy as possible for its population who wish to work in common and mutually support each other’s requests, but little else.

Conclusion

The summary of the new Angolan geopolitical position is that Angola is betting on vectors linked to foreign investment and fighting corruption, assuming relevance in foreign policy, partnerships with Western Europe, Spain, France, Italy, Germany, United Kingdom, with the Persian Gulf, Emirates and Dubai, and with India. At the same time, a strengthening of relations with the United States is anticipated. Portugal will always have a place apart.

Reference Bibliography:

-Banco Nacional de Angola-Statistics- www.bna.ao

-Douglas Wheeler and René Pélissier, História de Angola, 2011

-Ian Taylor, India’s rise in Africa, International Affairs, 2012

-José Milhazes, Angola – O Princípio do Fim da União Soviética, 2009

-Robert Cooper, The Ambassadors: Thinking about Diplomacy from Machiavelli to Modern Times, 2021

-Rui Verde, Angola at the Crossroads. Between Kleptocracy and Development, 2021

0-Introduction. A different focus for Angolan economic analysis

The consulting companies that are dedicated to the study of the Angolan economy follow a conjunctural methodology in which the predominant narrative is based on the negative numbers about the macroeconomic aggregates and their possible perspectives.

However, a more detailed analysis of the evolution of the Angolan economy suggests that behind the numbers of inflation, unemployment, GDP growth and public debt, which are not very encouraging[1], a series of public political reforms are taking place together with the reinforcement of certain economic trends that will indicate the construction of a new, more positive economic reality for Angola.

This study deals with the positive elements that point to the correction of the direction of the Angolan economy in a sense more consistent with the necessary prosperity.

A-Positive trends in the Angolan economy

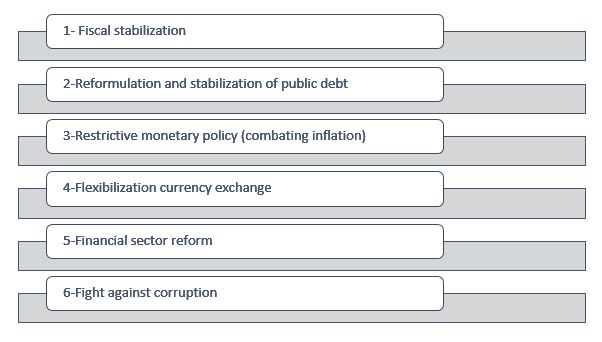

1-The International Monetary Fund (IMF) and public policy reform

A first element that allows to shed a different light on the perspectives of the Angolan economy lies in the recent assessment carried out by the IMF. In fact, on January 11, the IMF Executive Board concluded the fourth review of the Extended Fund Mechanism Agreement for Angola and approved the disbursement of an additional USD 487.5 million[2].

The important thing in this decision is the IMF’s positive assessment of the reform of Angolan public policies. The IMF states that: “The [Angolan] authorities achieved a prudent budgetary adjustment in 2020, which included gains in non-oil revenues and containment of non-essential expenses, while preserving essential spending on health and social security networks. The approval of the 2021 budget in December consolidates these gains. The authorities have also allowed the exchange rate to act as a shock absorber and have begun to implement a gradual shift towards monetary restraint to face increasing price pressures [3]”.

According to what the IMF explains, the economic policy followed by the Angolan government is developed in the following vectors:

-The stabilization of public finances, which is the cornerstone of the authorities’ strategy. In this regard, the government achieved a strong fiscal adjustment in 2020. In addition, its budget for 2021 consolidates non-oil revenue gains and the containment of budget expenditures for 2020, while protecting priority social and health expenditures.

These advances help to reduce the budget’s dependence on oil revenues.

– Reformulation and management of public debt. The government has implemented debt profile reform agreements, in addition to benefiting from the extension of the Debt Service Suspension Initiative until the end of June 2021, which will provide significant debt service relief and help reduce risks related to debt sustainability. We will elaborate below on the reformulation and management of public debt.

-Restrictive monetary policy and exchange rate easing. After easing the monetary constraint to mitigate the shock of COVID-19, the National Bank of Angola (BNA) began, once again, to face the increase in inflationary pressures through the tightening of monetary policy. A more gradual tightening of monetary policy is needed to reduce inflation. Exchange rate flexibility served as a valuable buffer during the crisis. Efforts are underway to develop a liberalized foreign exchange market.

-Reform of the financial sector. Continued progress in financial sector reforms was critical, especially the completion of the restructuring of the two struggling public banks. The timely adoption of the revision of the BNA Law and the revision of the Financial Institutions Law is the key to continuing this progress.

Finally, the IMF highlights the fundamental aspect that underlies all political reform, which is the maintenance of the fight against corruption.

What can be seen clearly from this IMF assessment is that the government is pursuing a reformist policy based on the assumptions made by this international organization, and is implementing difficult reforms.

It is known that many of these IMF policies have an initial recessive effect, especially fiscal consolidation when it involves raising taxes and cutting wages and subsidies, as well as restrictive monetary policy to fight inflation. It is therefore no wonder that the first result of adopting IMF policies is recession and not growth.

What is expected is that this “housekeeping” creates the conditions for a sustained and virtuous growth of the Angolan economy.

Fig. Nº. 1 – Economic policies of the Angolan government celebrated by the IMF

2-Management and careful reformulation of public debt

The executive followed an appropriate strategy when initially negotiating with China the issue of public debt. As we described in previous reports, the Chinese debt is key to Angola, as it represents about 50% of external commitments[4]. Consequently, it was important, first of all to ensure the appropriate terms with China, although they are not public knowledge, apparently imply a three-year suspension of payments agreement. The adherence already mentioned to the IMF’s debt suspension program allowed the government room for maneuver. It should be noted that the Eurobonds on which a lot has been written and pointed out various dangers, has a smaller weight in the total Angolan debt, around USD 8 billion, thus not having, on the contrary, what one could think of exaggerated pressure on Angolan finances in this area.

So, for now, the issue of public debt pressure seems to be eased and within the government’s management capacities.

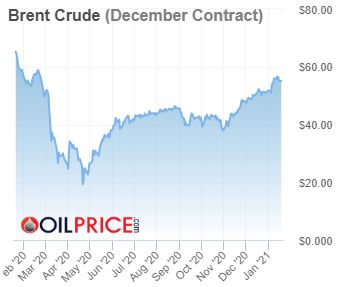

3-Meridian oil price recovery

As we had also anticipated, after an abrupt drop in the price of oil at the beginning of the pandemic (March 2020) there would be a rise[5], which is gradually happening.

The reality is that following a trend that was already very clear at the end of the year, the barrel of brent finally reached a price above $ 55, a value that had not been reached since the end of February 2020, the month before the start of the pandemic. Still being the most relevant indicator for the Angolan economy, and considering that the budget for 2021 was calculated based on USD 33 per barrel, we have a financial margin of more than USD 20. This is an additional “cushion” in the management of Angolan public finances.

It is clear that it is not known for how long this rise in the price of oil will continue. The commitment of the new Biden administration to the Paris Agreement, the evolution of the Chinese economy, the decision to cut or increase production by Saudi Arabia and the maintenance of the restrictions resulting from the Covid-19 pandemic are factors that may imply a further decline in the oil price.