Social life in Angola is very alive and, at this moment, political and judicial matters dominate the country’s agenda. However, it is in the domain of the economy that there is an extremely significant evolution on which it is important to reflect and proceed to a careful analysis.

The recent (February 2023)[1] International Monetary Fund (IMF) report on the country underlines the favorable advances of the Angolan economy and also the necessary reforms. It is based on this report that we will enunciate Angola’s main trends in the economic field and the neuralgic points to avoid relapses such as the last long recession that began in the presidency of José Eduardo dos Santos.

Positive Trends

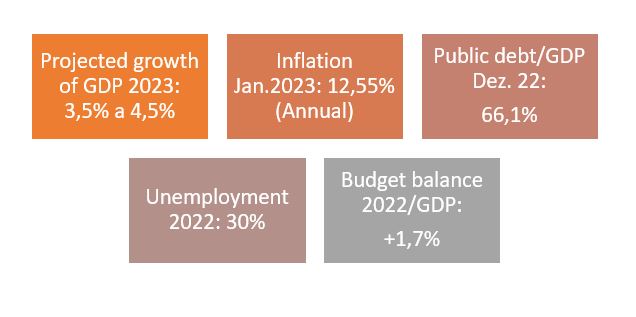

Angola’s economy is in full recovery after the five-year recession (2016-2020). By 2022, supported by higher oil prices and resilient non-oil activity, it has already reached growth of more than 3%, estimating the IMF that by 2023 the country continues to see the GDP increase in the order of 3.5%.

Therefore, we see growths of over 3% per year, which by our calculations, maintaining the price of oil and accelerating the liberalization of Angolan markets and foreign investment, could accelerate to numbers of 4% or 5%, adopted that are the right policies.

The optimism we share here results from the fact that non-oil growth has been widespread, despite a difficult external environment, as it means that the non-oil sector is reviving, as well as the attention that several developed countries with market economies are providing Angola, as is the case of US, Spain, France and Germany. Mentions should be made to recent visits to Angola of the King of Spain and the President of the French Republic, Emmanuel Macron (February and March 2023).

It should be noted that the debt that the public debt/GDP ratio has dropped about 17.5 percentage points of GDP, for an estimated 66.1% of GDP, aided by a stronger exchange rate. It is estimated that the checking account remained with a large surplus in 2022, while coverage of foreign currency reserves remained adequate (IMF data).

The fact is that the Angolan government has, according to the IMF, to adopt and maintain solid macroeconomic policies and maintained a commitment to structural reforms that are vital to Angola’s economy.

Necessary reforms

We understand that it is in the verification of fundamental structural reforms that resides the future of the Angolan economy. We highlight some reforms that are necessary to take and/or continue.

1-First renovation, with impact on the medium and long term, is to foster training for the economy of young people. Training not only means, and perhaps not in most, university education, but solid training in basic education and in professional aspects. We argue, therefore, that there must be an effective bet on vocational and technical education in Angola, before any other. A real bet on professional and technical schools and institutes, which are seen as valuable alternatives to academism and not mere university imitations (tragic error of Portuguese polytechnics).

2-Second renovation entails the creation of more conditions for investment, no longer at the legal level, where there is a modern framing and updated twice during the presidency of João Lourenço, but at the judicial, administrative and good practices level. The investor must feel safe to arrive in Angola and apply his money. One should not be afraid of being without the money due to any interference from an oligarch, or see any process dragging on in court. The speed and impartiality of justice is linked to good investment.

3-Third reform is dedicated to the financial sector, there is a special emphasis on increase credit to private persons and and the resolution of banking weaknesses. Quickly we must merge and capitalize banks, creating a banking sector not dependent on the state, clientelism or mere public debt management.

Finally, among other reforms, we highlight the true imperative of making more progress in strengthening governance and transparency, to improve the business environment and promote private investment.

Of course, continuing and accelerating anti-corruption strategy is also important.

National Employment Plan

All these news should be framed with the well-being of the population and the serious problems still pending. The one we highlight is unemployment, which although noting a slight descent, is still very high, about 30% [2]. This is an area in which we advocate direct state intervention. It is evident that the increase in GDP corresponds to an unemployment decrease, however, we believe that in the face of such high unemployment, in the short term the immediate action of the government is fundamental.

In this sense, the recent announcement of the World Bank of US $ 300 million for a project to accelerate economic diversification and job creation[3] is to greet. Not knowing in detail the design of this acceleration program, its existence should be underlined, as well as the previous announcement of the Angolan Labor Minister of the creation of a National Employment Program, with the aim of creating more opportunities for insertion of young people in job market[4]. Also, in this case, the data are scarce about the design of the plan, and it is certain that the President of the Republic had declared in the discourse of the State of the Nation of 2022, the creation of the referred plan.

So far, these initiatives related to unemployment, although positive, seem uncoordinated and poorly implemented. Therefore, the truth is that Angola would win to see a comprehensive national employment plan, specific and directly coordinated by the President of the Republic, without the risk of not properly implemented a plan, which in the short term is fundamental to the economy and Angolan population.

https://www.cedesa.pt/wp-content/uploads/2023/03/econ2.jpg6581006CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2023-03-17 13:53:002023-03-13 18:59:13Angolan Economy trends, necessary reforms and national employment plan

The proposal of the State General Budget (SGB) from Angola to 2023 has already been delivered to the National Assembly, including its essential elements of an affordable and pedagogical digital page of the Ministry of Finance[1].

The Ministry of Finance in its official note highlighted the following main aspects about SGB[2].

Objectives

The two main objectives of budget policy are the “continuation of national economic growth and the continuation of prudent budgetary management.”

Budget balance and public debt

The budget balance will be surplus in the value of 0.9% of GDP, consolidating the evolution of 2021 and 2022. The public debt ratio in relation to Gross Domestic Product (GDP) is decreasing, and projections for 2022 point a ratio of 56.1% of GDP, manifestly less than 128.7% already registered. The government expects the conjugated tendency to decrease public debt and inflation (which estimates 11% at the end of 2023), finally, to decrease interest rates, promoting economic growth.

Some tax aligners will be maintained such as reducing the VAT rate of basic basket products, which fell from 14 to 5%, and in hotel and tourism (14 to 7%).

Oil price

SGB’s proposal has as reference the oil barrel to USD 75.00.

Sectors expense

In terms of expenditure affectation, 23.9 % for the social sector are budgeted, 10 % for the economic sector, 8.6 % for defense, security and public order while general public services have 12.5 %.

According to the government, social expense represents the largest share of expense in SGB absorbing 43.5% of primary tax expense and 23.9% of total budget expense, with an increase of 33.4% compared to SGB 2022.

Growth

In terms of predictions that substantiate the proposal, the SGB assumes that by 2022, the real GDP should have a positive real growth rate of 2.7%, above the 2.4% initially provided for in SGB 2022, and for the year of 2023, a real growth of 3.3% is expected[3].

Inflation

The government expects to 2022 an inflation of 14.4%, well below the 18%goal. For 2023, it anticipates an inflation rate of 11.1%, as mentioned above.

2-The Question of Oil

It is evident that the price of oil still occupies a wide space in the Angolan economy. According to the Ministry of Finance data, in the SGB of 2022, the oil sector represented approximately 25% of the nominal SGB, and it is expected to be 22%[4].

Set the determining role of oil in the economy and in Angolan public accounts, it is repeated that the indicative price calculated for SGB 2023 was 75.00 USD/BBL as an average for the year, with an average production of 1 180.0 MIL BBL/DAY.

At this moment (December 13 2022) the price of the barrel is in USD 79, 03[5] and the trend in markets in recent times has been falling. Last month came from a level higher than USD 90.00 to a limit less than USD 80.00. Obviously, the volatility of oil price is large and no one can make predictions about the predictable evolution of the price. The current fall is attributed to the slowdown of the Chinese economy and the effect of rising US interest rates on commodoties. It may be like this or not, the price may climb or go down. If there is perhaps an expectation of climbing, as it is anticipated that China begins to recover and US interest rates no longer increase, besides OPEC production cuts, the truth is that the budget margin is not too big in Terms of oil price. Quickly, price oscillations can call into question SGB calculations.

In addition, the accuracy of daily production is 1180 thousand barrels, when the average of 2022 was 1 147 in 2022 and 1 124 in what refers to 2021. Given a recognized obsolescence in some sectors of oil production in Angola It may happen that this barrel value is not achieved.

This means that, in our opinion, there will be some optimism in the oil projections in SGB 2023 both at the price level and at the production level. It cannot be said that projections will not be verified, only that some emergency reserve is required for projections not to be consummated.

There is still a very thin line between success and budgetary failure, so a renewed reform of the economy is critical.

3-The Social Expenditure

The government announces as a great success of its proposal the increase in social expense by 33.4% compared to 2022, occupying the largest slice by sector. Realizing, the reasoning report states that social expenditure will correspond to 43.5% of primary tax expense (without debt service), which is 23.9% of total expenditure and an increase of 33.4% compared to SGB 2022, as already mentioned. “In this sector, we highlight education, health, housing and community services and social protection, with weights of 14.1%, 12.1%, 10.1% and 6.2% in primary tax expense, respectively[6].” The truth is that comparing education, health, and housing with 2022, in all these rubrics there is an increase in expense higher than inflation.

Notably is the exponential climb of health and housing over the next year, with increases of 45.1% and 57.6% respectively.

If we notice the 2022 SGB, the social sector represented 38.8% of primary tax expense, corresponding to 19.02% of total expense and an increase of 27.1% compared to SGB 2021[7]. This means that it is manifest that the government is paying special attention and promotion to the social sector that increases year after year. The numbers prove this social attention of budget policy.

However, as is well known it is in the social sector that the complaints of the population often appear. There is a problem that is not budgetary, but related to management and rationality. It has to effectively execute the SGB and make the money reach people. The issue is increasingly good management and good governance, competence and deliverance, not the lack of resources.

4- The financial expense related to debt

The debt financial expense is 45.1% of SGB expense, decreasing by 2.6% compared to 2022[8]. In practice, we have a little less than half of the SGB designed to pay debts. We will not wave with the “ghost” of debt failure, which we have referred to over the long analyzes we have made, it does not exist. What worries us is the content of the debt and the fact that the state is supporting and paying a debt that is not his.

As an Angolan press agency specialized in economics and confirms official data, “China remains the country that Angola should most, holding about 40% of the total. Most of the debt to China has as its main creditor the China Development Bank (CDB), as a result of a USD 15 billion financing, as part of an agreement signed in December 2015.”[9]

This 2015/2016 Chinese loan is one of the most issues one must pay attention to and has a specific approach.

Our argument is that part of Angolan public debt is what is doctrinally called “odious debt.” The legal doctrine of “hateful debt” argues that sovereign debt contracted without the consent of the people and that it does not benefit it is “hateful” and should not be transferable to a successor government, especially if creditors are aware of these facts in advance[10]. We do not fight for non-full payment of this debt or others to China or another country (also offers us many doubts the debt enrolled in favor of the UK, but we will leave this theme for another occasion) or entity, but a bi-volunteer renegotiation with the respective Haircut of capital and interest that manifestly relieves the weight of the debt.

Consequently, there should be a profound forensic audit to this 2015/2016 Chinese loan whose destination has never been very clear, except in vacancies that would be applied at Sonangol, at a time coincident with the assumption of the company’s management mandate by Isabel dos Santos. After this forensic audit and according to the results obtained there should be a very serious renegotiation of debt with China. In 2015, China already had more than enough elements to know that part of its borrowed money was being poorly applied. In fact, this is the year when its supposed representative, Sam Pa, was apparently detained. The country, as a great power it is, cannot be hidden behind legal formalism and has to face together with Angola the problem of its debt that was diverted by corruption.

5-Conclusions

It is evident that there is an economic policy effort to exist financial rigor and budgetary control according to the injunctions of the International Monetary Fund, externally credible the country in economic terms. Alongside this financial rigor that cost João Lourenço quite electorally in August 2022, there is attention to the social sector, trying to mitigate the financier.

This budgetary policy is correctly formulated, the question to be aware is within the scope of the realization and execution. It is essential that social expense comes to those who need it and in the frontline structures: doctors, nurses, hospitals, schools, teachers, etc., and do not stay in intermediate consumption and corruption shortcuts that act as funds siphon. In other words, it is imperative that budget public money is not diverted. And then it becomes imperative to control the affectation and application of the funds. The task of good management and governance is the most important in the SGB of 2023.

At the level of resources it is relevant to emphasize that the oil activity (price and quantity produced) optimistic is relevant to us, to this extent, it is important to have a contingency reserve for low price and production.

And in relation to public debt in the face of China (and other entities) we argue that certain forensic audits are required and if something similar to a “hateful debt” is glimpsed, mechanisms of profound renegotiation are activated. Ultimately, it would have to bring the matter (“debt hatred”) to the United Nations pursuant to articles 1 (3) and 14, among others from the United Nations Charter to create a consensus on international law on the subject.

https://www.cedesa.pt/wp-content/uploads/2022/12/Capturar.jpg532870CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2022-12-20 11:36:152023-08-14 14:19:13Analysis of the General Budget Proposal of the State of Angola for 2023

0-Introduction. A different focus for Angolan economic analysis

The consulting companies that are dedicated to the study of the Angolan economy follow a conjunctural methodology in which the predominant narrative is based on the negative numbers about the macroeconomic aggregates and their possible perspectives.

However, a more detailed analysis of the evolution of the Angolan economy suggests that behind the numbers of inflation, unemployment, GDP growth and public debt, which are not very encouraging[1], a series of public political reforms are taking place together with the reinforcement of certain economic trends that will indicate the construction of a new, more positive economic reality for Angola.

This study deals with the positive elements that point to the correction of the direction of the Angolan economy in a sense more consistent with the necessary prosperity.

A-Positive trends in the Angolan economy

1-The International Monetary Fund (IMF) and public policy reform

A first element that allows to shed a different light on the perspectives of the Angolan economy lies in the recent assessment carried out by the IMF. In fact, on January 11, the IMF Executive Board concluded the fourth review of the Extended Fund Mechanism Agreement for Angola and approved the disbursement of an additional USD 487.5 million[2].

The important thing in this decision is the IMF’s positive assessment of the reform of Angolan public policies. The IMF states that: “The [Angolan] authorities achieved a prudent budgetary adjustment in 2020, which included gains in non-oil revenues and containment of non-essential expenses, while preserving essential spending on health and social security networks. The approval of the 2021 budget in December consolidates these gains. The authorities have also allowed the exchange rate to act as a shock absorber and have begun to implement a gradual shift towards monetary restraint to face increasing price pressures [3]”.

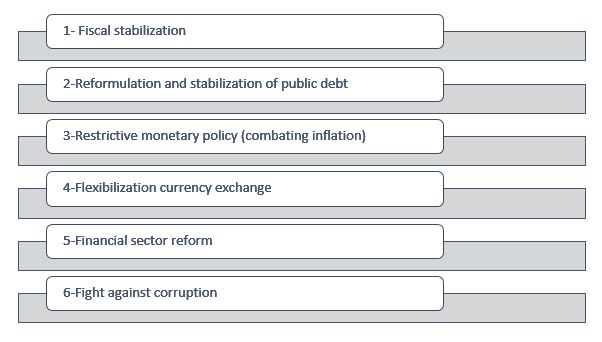

According to what the IMF explains, the economic policy followed by the Angolan government is developed in the following vectors:

-The stabilization of public finances, which is the cornerstone of the authorities’ strategy. In this regard, the government achieved a strong fiscal adjustment in 2020. In addition, its budget for 2021 consolidates non-oil revenue gains and the containment of budget expenditures for 2020, while protecting priority social and health expenditures.

These advances help to reduce the budget’s dependence on oil revenues.

– Reformulation and management of public debt. The government has implemented debt profile reform agreements, in addition to benefiting from the extension of the Debt Service Suspension Initiative until the end of June 2021, which will provide significant debt service relief and help reduce risks related to debt sustainability. We will elaborate below on the reformulation and management of public debt.

-Restrictive monetary policy and exchange rate easing. After easing the monetary constraint to mitigate the shock of COVID-19, the National Bank of Angola (BNA) began, once again, to face the increase in inflationary pressures through the tightening of monetary policy. A more gradual tightening of monetary policy is needed to reduce inflation. Exchange rate flexibility served as a valuable buffer during the crisis. Efforts are underway to develop a liberalized foreign exchange market.

-Reform of the financial sector. Continued progress in financial sector reforms was critical, especially the completion of the restructuring of the two struggling public banks. The timely adoption of the revision of the BNA Law and the revision of the Financial Institutions Law is the key to continuing this progress.

Finally, the IMF highlights the fundamental aspect that underlies all political reform, which is the maintenance of the fight against corruption.

What can be seen clearly from this IMF assessment is that the government is pursuing a reformist policy based on the assumptions made by this international organization, and is implementing difficult reforms.

It is known that many of these IMF policies have an initial recessive effect, especially fiscal consolidation when it involves raising taxes and cutting wages and subsidies, as well as restrictive monetary policy to fight inflation. It is therefore no wonder that the first result of adopting IMF policies is recession and not growth.

What is expected is that this “housekeeping” creates the conditions for a sustained and virtuous growth of the Angolan economy.

Fig. Nº. 1 – Economic policies of the Angolan government celebrated by the IMF

2-Management and careful reformulation of public debt

The executive followed an appropriate strategy when initially negotiating with China the issue of public debt. As we described in previous reports, the Chinese debt is key to Angola, as it represents about 50% of external commitments[4]. Consequently, it was important, first of all to ensure the appropriate terms with China, although they are not public knowledge, apparently imply a three-year suspension of payments agreement. The adherence already mentioned to the IMF’s debt suspension program allowed the government room for maneuver. It should be noted that the Eurobonds on which a lot has been written and pointed out various dangers, has a smaller weight in the total Angolan debt, around USD 8 billion, thus not having, on the contrary, what one could think of exaggerated pressure on Angolan finances in this area.

So, for now, the issue of public debt pressure seems to be eased and within the government’s management capacities.

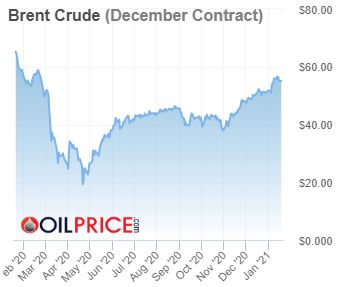

3-Meridian oil price recovery

As we had also anticipated, after an abrupt drop in the price of oil at the beginning of the pandemic (March 2020) there would be a rise[5], which is gradually happening.

The reality is that following a trend that was already very clear at the end of the year, the barrel of brent finally reached a price above $ 55, a value that had not been reached since the end of February 2020, the month before the start of the pandemic. Still being the most relevant indicator for the Angolan economy, and considering that the budget for 2021 was calculated based on USD 33 per barrel, we have a financial margin of more than USD 20. This is an additional “cushion” in the management of Angolan public finances.

It is clear that it is not known for how long this rise in the price of oil will continue. The commitment of the new Biden administration to the Paris Agreement, the evolution of the Chinese economy, the decision to cut or increase production by Saudi Arabia and the maintenance of the restrictions resulting from the Covid-19 pandemic are factors that may imply a further decline in the oil price.

Therefore, movements in the oil price are always unknown and these moments of increase must be used by the government to reinforce its reserves for future reproductive and social investments.

Fig. No. 2- Evolution of the Brent price since February 2020

4-Decrease in imports of food basket and agricultural production with continental relevance

The diversification policy combined with the promotion of the national industry through the substitution of exports has been another “motto” of this government. This policy allows in one fel swoop to reduce external dependency and create a thriving national industry.

While it is still untimely to draw any definitive conclusions about the results of this policy, some figures emerge that can be encouraging, at least in relation to the dependence on imports and foreign exchange spending on foreign trade.

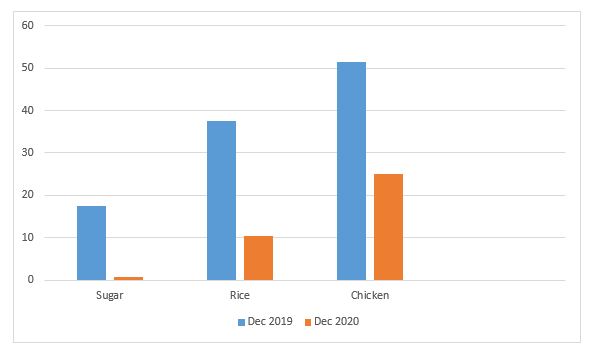

According to data provided by the Ministry of Industry and Trade, Angola managed to record a reduction of almost US $ 100 million in the import of products from the basic basket and other essential goods in the last month of 2020, compared to the same period in December 2019. In December 2019, the Government disbursed US $ 250 million for imports, while in the same period of 2020, it only spent US $ 152 million[6].

In particular, it is worth noting the reduction in sugar imports, which went from 2.1 million tons in 2019, at the cost of 17.6 million dollars, to 1,472 tons, at the cost of 831,121 dollars. Regarding the importation of current rice, in 2019 Angola imported 136,985 tons in the amount of US $ 37.2 million and in 2020, only 59,505 tons, in the amount of US $ 10.5 million. In what concerns chicken (the most consumed meat in Angola), it is also worth mentioning a considerable reduction, compared to 2019. In that year, 46,385 tons were imported, for US $ 51.5 million, whereas last year, only 32,447 tonnes were acquired, for a value of just over US $ 25 million.

Fig. Nº. 3- Comparison of annual imports of basic basket products (Dec.2019 / 2020 in USD million)

These are just some of the products highlighted in the considerable reduction in imports, however this trend has proved to be general in the remaining products that make up the basic basket.

For these numbers to be considered a success, it is necessary to compare them with the internal consumption of the same goods, and understand if the decrease in imports was due to a substitution by domestic products or only reflects a decline in demand as a result of the economic crisis.

In the latter case, although they represent savings in foreign exchange, they do not mean a success in politics, but a decrease in the quality of life of the population. However, even in this situation, national investors should be alert to proceed with investments in these areas in order to correspond to future demand growth.

Statistics published by the Angolan Ministry of Industry and Trade and released by the Portuguese news agency Lusa show the enhanced sustainability of some Angolan agricultural production.

Angola asserts itself as a continental-level agricultural producer. Angola is the largest African banana producer and the seventh in the world with an offer of 4.4 million tons, according to the latest table of the United Nations Food and Agriculture Fund (FAO). It should be noted that the banana continues to be the most produced and consumed fruit in the world. Angola, in particular, has declared itself self-sufficient in banana production for more than six years, with emphasis on the provinces of Bengo and Benguela. In these provinces, private companies already export the fruit to countries such as Portugal, Zambia, Democratic Congo and plan to bring the fruit to the United States, the world’s largest consumer[7].

In relation to cassava, Angola has an annual production estimated at more than 11 million tons of cassava, being today the third largest producer in Africa, after Nigeria and Ghana, and wants to bet on its transformation into starch[8].

5-New investments and exports. Two examples: Rio Tinto and Gold

The finance minister recently told Reuters: “We are building a future (through our reform program) that prioritizes direct investment (not just with China, but with other partners). We want to add value for our economy to create jobs. We want the money to stay. Borrowing is an option, but we are trying to change the way we relate to our partners [9]”.

Thus, it appears that the government is betting on direct investment to revive the economy and also to increase exports.

There are two recent examples that are important to underline in this context. The first is the entry of the powerful multinational Rio Tinto into the Angolan market. Apparently, such a perspective will materialize this year[10].

Also important is the first export of gold mined in Huíla in 2020, in the amount of sixteen hundred and ninety-six ounces sent to Portugal and the United Arab Emirates, which corresponds, at the current price, to more than three million dollars. Obviously, what is relevant is not the amount of gold exported, but the beginning of a trend. As with the entry of Rio Tinto, it is important to mark a trend that brings other big investors like Anglo-American or DeBeers.

None of these investments is very firm yet. Their reference is important because they can represent future axes for the development of the Angolan economy, now in the beginning.

Fig. nº 4 – Signs of optimism in the Angolan economy

B-Necessary policy adjustments

The foregoing demonstrates that the Angolan government pursues an economic reform policy based essentially on the IMF’s revenues: i) budgetary balance and debt control, considering financial solvency as a sine qua non for economic growth; ii) restrictive monetary policy to control inflation; iii) flexible exchange rate policy, allowing for a devaluation of the currency that encourages exports and hinders imports; iv) investing in investment and the private sector as engines of the economy.

Basically, the policy followed corresponds to what was once called the Washington consensus[11]. This is the standard reform package adopted by the IMF, World Bank and the US Treasury Department since the late 1980s and which corresponds to a liberal model of the economy, based on fiscal prudence and the free market.

Naturally, this model has potential for Angola, but it is not enough. There are not strong enough institutions in Angola yet to guarantee the functioning of a free market in which some do not end up dominating others and creating oligopolistic and inefficient situations, as there is not a private sector strong enough to become the engine of the economy.

Making Angola’s economic reform dependent on reforms inspired by the Washington Consensus is not enough, a broader view is needed.

This broader view should imply structural institutional reform. This means that property rights must be clarified by abandoning the confusion that the collectivization of property has generated and still generates, courts must be put in place, bureaucracy is no longer an obstacle, and obviously great corruption must be eradicated. In addition to structural institutional reform, it should be realized that the State has a role to play in this new phase. There is no robust private sector in Angola, nor can everything be delivered to foreign investors with short-term perspectives. A mix should be found between the state and the private sector. In fact, this is how the most advanced Western countries work, despite rhetoric. It is important to adopt the concept advanced by Mariana Mazzucato of Entrepreneurial State[12].

The point to consider in economic reform in Angola is that the role of the government, in the most successful economies, went far beyond creating the right infrastructure and setting the rules. The State is a fundamental agent to achieve the type of innovation that allows companies and economies to grow, not only by creating the “conditions” that allow innovation. Instead, the state can proactively create a strategy around new areas of high growth before the potential is understood by the business community by financing the most uncertain phase of research in which the private sector is risk-averse, seeking new developments, and often even supervising the marketing process.

In addition, the IMF’s recessionary policies, while necessary, must be offset by other types of policies that alleviate the socially depredating burden of those. In short, there must be a mix of reformist policies that is more comprehensive and adequate to Angola, so that in the end the first flashes of success have sustained results.

C-Conclusions

It is necessary to look beyond the negative conjuncture numbers of the Angolan economy and understand that there is a reformist economy policy that is beginning to bear fruit and to mark some new trends. This policy has been applauded (and possibly advised) by the IMF, and here lies its strength and weakness. Strength because it contains some indispensable measures to clean up the Angolan economy and launch it on the path of growth. It also strengthens because its adoption and implementation brings the praise and support of the IMF and sister organizations. However, this policy also has weaknesses, including the lack of attention to institutional reform, the weakness of the private sector in Angola, the recessive effects of contractionary policies, among others.

Consequently, with signs of optimism in the medium-term perspectives of the Angolan economy, it is necessary to improve the economic policy that is being followed, including the intensification of institutional reforms that ensure that the judiciary works, bureaucracy does not hinder, corruption does not divert resources. In addition, the role of the State as an entrepreneurial partner in the private sector should be reviewed.

[1] See the most recent figures: Unemployment 34% (III quarter 2020), Annual inflation 25.19% (December 2020 / December 2019), GDP growth -5.8% (III quarter 2020) at https: // www. ine.gov.ao/

https://www.cedesa.pt/wp-content/uploads/2021/01/otimismo-economia-2.jpg10801920CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2021-05-12 18:51:492021-05-12 18:51:51Flashes of optimism in the Angolan economy at the beginning of 2021

This is a time of reinvention for Angola. Sonangol is no longer the engine of the Angolan economy and it is necessary to find a new driver. There are two reasons for the need to overcome the economic model based on a single product – oil.

The first reason is Sonangol itself. The results for 2019, presented by the Angolan oil company, are structurally discouraging. Although they show a profit, this profit derives from unrepeatable extraordinary results and the essential elements of the oil operation are stagnant: production does not increase, sales do not exceed the level of previous years. The company’s net income was USD 125 million. However, revenues remained stable compared to the previous year. Sonangol produced around 232 thousand barrels of crude oil per day, a number similar to the past and made sales of USD 10,231 million, which represents a 4% reduction compared to the 2018 financial year.

In short, oil exploration no longer adequately supports Sonangol. Not supporting Sonangol means not supporting the country.

In addition to this stagnation at Sonangol, there is the fact that oil is being increasingly viewed with skepticism, seeking to invest in alternative energies and moving away from the use of black gold. This is obviously not a short-term process, but it will have been accelerated with the Covid-19 pandemic. Oil will still have price rises, possibly peaks in higher demand, but everything indicates that the gluttonous years will be over, as other energy sources will emerge that will more or less gradually replace oil. Just note that in the last few months the price of the Brent barrel has fluctuated between USD 53 in October 2019, USD 60 in January 2020, USD 12.78 in April or USD 40.7 recently. However, he never returned to the 2014 figures where he was often above USD 100.

These two reasons mean that the Angolan economy has to reinvent itself, and more quickly than it thinks. It is not just a matter of restructuring Sonangol and focusing it on the oil business. It is not enough, because this business is stagnant. It is the economy itself that needs restructuring, which in the official jargon of the Angolan government is called diversification.

The problem is that diversification implies the creation of a new offer in the Angolan economy, of the production of goods and services that did not exist in the recent past. And for production to exist, investment is necessary. Investment requires, obviously, the contribution of capital.

And here we face another issue that affects the Angolan economy, which is the lack of capital and the recessive policies that intensify this scarcity. Following the parameters chosen by the International Monetary Fund (IMF) and the neoclassical orthodoxy of the economy, a program to contain / reduce public debt and reduce the deficit is being imposed on Angola.

We have many doubts as to whether such a program is justified in the case of the Angolan economy, especially considering the doctrinal contributions in Modern Monetary Theory, but the fact is that such a program to cut spending and increase taxes is being followed. However, the pursuit of such a policy ends up limiting the availability of capital for investment, whether public or private. Therefore, it prevents the so-called diversification that is so necessary to overcome Sonangol’s stagnation.

Thus, the outlook facing the Angolan economy at the moment is difficult. On the one hand, its engine – Sonangol – is stalled, on the other, the creation of capital to mobilize productive investment to diversify the economy is being strangled due to the recessionary policies adopted. This has obvious repercussions on the economy’s figures. GDP growth is negative – 3.6%. Unemployment assumes a staggering number of 32.7% and inflation of 22.8% (similar in August 2020). None of these numbers are encouraging.

The Angolan economy needs political courage to reverse this state of affairs.

Sonangol has to be restructured, but as an energy company and not merely an oil company. In reality, it is not enough to focus on oil, you will have to present yourself with a modern renewable energy company, taking advantage, for example, of the sun. If the United Kingdom recently announced that it wants to become Saudi Arabia by the wind, Angola may be Saudi Arabia by the sun. Therefore, an imaginative restructuring of Sonangol is necessary.

At the same time, recessionary economic policy must be abandoned. Although there should be budgetary discipline and not paying works twice or paying wages to phantom employees, as well as not contracting public debt to feed private pockets, the fact is that the policy of financial rigor must be complemented by a policy of fiscal stimulus that allows building a sufficient capital base to carry out the necessary reproductive investment. A public and private pro-investment tax policy is fundamental in reinventing the Angolan economy.

https://www.cedesa.pt/wp-content/uploads/2020/10/sonangol.png554924CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2021-05-10 20:14:122021-05-10 20:14:14Sonangol and the reinvention of the Angolan economy

Some studies by prestigious economic consultants have lately issued some reports on the Angolan economy that only report negative numbers and projections, without taking into account either the theoretical models on which some of the main economic policy decisions in Angola are based, or the actual reality of its economy.

One of the most intriguing cases is the permanent link between the rise in inflation and the devaluation of the Kwanza, presenting the two phenomena as cause and effect or effect and cause, as well as always giving a negative connotation to the term “devaluation”.

This article, which does not aim to make forecasts, which at this time of Covid-19 would be rash, offers alternative explanations behind the Kwanza`s devaluation, looking instead at the opportunity it offers foreign investors.

It is evident that the semi-rigid or controlled exchange rate regime that existed before the adoption of the flexible exchange rate last year, was partly responsible for the crash in the Angolan economy. In fact, pegging the Angolan currency at a high value in view of market conditions, caused unrestrained consumerism while domestic production was allowed to decline, since international prices were artificially made more competitive.

It was the time when Luanda became the most expensive city in the world with the Angolan elite making flagrant shows of wealth. This situation did not correspond to domestic production or development, but rather excessive spending of foreign currency earned from high oil prices which bolstered the inadequate value of the Kwanza. This was unsustainable.

The prolonged recession since 2014 demanded an end to the artificial appreciation of the Kwanza and the introduction of a flexible exchange rate.

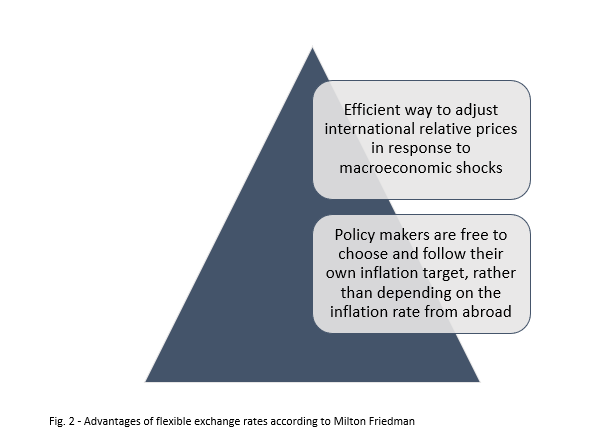

The model underlying the adoption of flexible exchange rates has clear goals. Since Milton Friedman’s seminal text in 1953[1] on flexible exchange rates, two arguments support this policy: first, free movements in exchange rates are an efficient way of adjusting international relative prices in response to macroeconomic shocks; second, with flexible exchange rates, policymakers are free to choose and follow their own inflation target, rather than depending on the inflation rate from abroad. This last factor should be emphasised. Milton Friedman stressed that exchange rates would help to insulate the domestic economy from external shocks and would give national political authorities the ability to meet domestic goals. Flexible exchange rates provide enough insulation to the domestic economy if the sources of the recessionary shock are abroad.

This means that with a flexible exchange rate, it is possible for the government / central bank to pursue an autonomous anti-inflationary policy on the external value of the currency. In fact, the devaluation of the Kwanza could mean that the prices of international goods become excessively expensive for Angola, and spark that, contrary to what happened previously, being cheaper to produce goods in Angola. That would be the opportunity to invest in Angola`s agriculture and industry, at they will have a market and low production costs due to the devaluation.

With national goods becoming more competitive than corresponding foreign goods, this will boost national production and encourage exports.

And provided that the central bank does not pint excess money, national production should increase and inflation should decrease if internal policies are adequately followed.

This does not mean that the transition from an economy artificially anchored by a high-value Kwanza supported by rising oil prices to a competitive and productive economy is easy. Angola is currently in deep crisis, made worse by the Covid-19 pandemic, and luck, either bad or good, has to be considered.

However, the exchange rate easing policy is right and there is no need to be afraid of devaluation. This is making the economy more competitive overseas and encouraging the manufacture and production of goods to sell both internally and abroad. Success depends more on government policies; policies that are coherent and consistent.

That is why the figures being released on devaluation and inflation are, on the surface, frightening, but they will only have a negative impact if the government implements the wrong policies.

Otherwise, they are not, by themselves, of any relevance. It is known that the Kwanza was overvalued and that this has greatly affected the Angolan economy. It is known that combating inflation, with flexible rates, does not depend on the outside world, but on the right decisions by the government.

There is awareness that Angola is in deep economic crisis, but some real encouraging indicators are beginning to emerge. One of them is that “Angola disbursed, in the first quarter of the year, 495 million dollars (436.5 million euros) on importing food products, a decrease of 31% compared to the 717 million dollars (632.3 million euros) ) for the last quarter of 2019.[2]”

The Angolan government attributed this evolution to a better organisation of its foreign exchange market and to an increase in the demand for national products. Official sources state: “We are verifying these two factors, we can say that we are on the right path, there is a demand for national production, there is a decrease in imports.” These facts seem to confirm the analysis we do. Obviously, in the end everything will depend on the right internal public policies.

[1] Friedman, M. (1953) “The Case for Flexible Exchange Rates.” In Essays in Positive Economics, 157–203. Chicago: University of Chicago Press.

https://www.cedesa.pt/wp-content/uploads/2020/07/kwanzas_photos_v2_x2-scaled.jpg12121920CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2020-07-27 09:47:322020-07-27 09:47:34The devaluation of Kwanza and inflation

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.