1-The International Monetary Fund’s report on Angola (Feb.2025)

None of the IMF’s various interventions in Angola have succeeded in changing the country’s economic structure and helping to launch it on a path of development, demonstrating the fragility of the IMF’s models of action in Africa.[1]

When the IMF comes up with equivocal results, it uses ambiguous communiqués that allow for different interpretations and, of course, disempower the institution. This is the case with the organization’s most recent statement on Angola, which is a real exercise in ambivalence.

However, despite this, or above all because of it, this communiqué[2] is a valuable tool from which to draw some conclusions and clues for the future of the Angolan economy, essentially the need for effective and real acceleration of economic reform in the direction of competition, productivity and radical modification of the financial functioning of the state.

On February 24, 2025, the Executive Board of the International Monetary Fund (IMF) concluded its Article IV consultation on Angola. It then issued a communiqué, which has now been made public.

On a positive note, the IMF points out that Angola’s economy recovered in 2024, mainly due to the oil sector. GDP growth is estimated to have reached 3.8 percent, exceeding previous projections, although this growth has been extended to the non-oil sector. The public debt/GDP ratio fell in 2024, benefiting from higher nominal GDP growth and sustained primary fiscal surpluses. This is the good news: the economy is growing due to the oil sector, while at the same time having a spill over effect on the other sectors.

Fig. 1- Evolution of Angola’s real economy as a percentage. Source: IMF 2025

At the same time, the IMF is cautious and somewhat frightened by a number of problems:

-General State Budget (public accounts) slippage due to higher capital expenditure and delay in removing the fuel subsidy.

-High inflation due to exchange rate pressures and food prices.

-Adverse market expectations and a high external debt service put great pressure on the value of the Angolan currency.

Due to the imminent dangers, the IMF “invites” the Angolan Executive to accelerate structural reforms of the economy, in which it emphasizes fiscal consolidation (cutting public spending or increasing taxes), the withdrawal of fuel subsidies, rationalizing public investment and improving the efficiency of spending, strengthening the management of public finances, including the public procurement framework and reforms of public companies. It also reaffirms the need for monetary policy to maintain a restrictive bias to ensure lasting disinflation.

The main emphasis, according to the IMF, should be on pro-market policies aimed at simplifying business regulation, strengthening governance, fighting corruption, developing human capital and deepening financial inclusion. Greater statistical capacity is also needed to support sound policymaking.

2-Beyond the IMF. The necessary reforms

The IMF communiqué itself contains contradictions that show its difficulty in obtaining a realistic view of the Angolan economy. For example, it attributes inflation to the liberalization of the exchange rate and the rise in food prices. Let’s remember that it was the IMF that recommended the abrupt adoption of a totally flexible exchange rate, without noticing that a good part of Angolan food was imported…so it’s an IMF policy that according to the IMF itself generates inflation….

However, further down he talks about the need for a restrictive monetary policy, which is obviously Angola’s major problem and the ultimate source of all inflation, the lax attitude of the BNA which lives with negative reference interest rates in real terms (BNA reference interest rate, 19.5% for inflation of 26.48%) and has difficulties controlling the money supply .[3]

Fig. 2-Development of monetary aggregates as a percentage/end of period. Source: IMF, 2025

Also surprising is the obsession with fuel subsidies, since it is clear that withdrawing them will generate even stronger inflationary pressures and possible social upheaval.

Even the warning about budget slippage seems out of context. If you look, the balance for Angola’s General State Budget (GSB) for 2025 is -1.3% of GDP, nothing significant. In fact, Angola doesn’t need less spending or austerity; on the contrary, it needs more effective spending.

Fig. nº 3- Overall Budget Balance, percentage of GDP. Source: IMF, 2025

The problems of the Angolan economy do not lie along these lines, but along others that the IMF also addresses, but does not highlight.

Even now, Sonangol’s current income statement presents more doubts than certainties: Sonangol ended 2024 with a debt of 4.5 billion dollars, representing an increase of 15.4% on the previous year. At the same time, revenues fell to 10 billion euros last year, a drop of 8.6% in the space of a year. EBITDA (earnings before interest, taxes, depreciation and amortization) also fell by 8.8% year-on-year to 3.2 billion euros[5] . Let’s be clear, these results are not good. It’s not the catastrophe of 2015, but it’s not very encouraging.

The efficiency of companies can be optimized through partial privatization, since management with private partners tends to be more agile and focused on results, possibly encouraging innovation in mixed companies. The introduction of competing visions (state and private) can lead to cost savings and the elimination of unnecessary bureaucracy. Similarly, selling off parts of state-owned companies can generate revenue for the government, easing budget constraints and reducing the need for public funding. Partial privatization can lead to improvements in the quality of services, as private entities focus on customer satisfaction. Finally, mixed companies will have greater flexibility to adapt quickly to market demands.

Essentially:

All these reforms should be speeded up in the two and a half years that remain before President João Lourenço finishes his term in office.

[1] Cfr. https://actionaid.

[2] See https://www.imf.org/en/Ne

[3] https://www.makaangola.org/2024/03/bna-o-culpado-da-inflacao-em-angola/

[4] A recent example of pure waste: https://www.makaangola.org/2025/02/os-consumiveis-do-saque-no-kuando-kubango/

[5] https://www.jornaldenegocios.pt/economia/mundo/africa/detalhe/sonangol-ve-divida-aumentar-para-43-mil-milhoes-em-2024

China’s economic crisis: facts and causes

There is a problem in the Chinese economy that appears to be structural and could affect relations with debtor countries such as Angola. Various factors are contributing to a decline in economic growth in China and an increase in unemployment, especially among young people, which could also imply some political instability within China itself.

Let’s start with some recent figures[1] :

-The July credit data released on 11 August showed a drop in demand for loans from companies.

-Retail sales rose by just 2.5 per cent in July compared to the previous year, below expectations of a 4.5 per cent increase.

-Industrial production only rose by 3.7 per cent in July compared to the previous year, below the 4.4 per cent increase that analysts were expecting.

The truth is that recent statistics published by China have caused severe concern. In addition to the aforementioned statistics, consumer prices in July were lower than a year ago, suggesting that we may be on the verge of deflation, which reflects a chronic shortage of demand in the economy. China’s foreign trade in the same month of July showed a sharp drop in exports due to weak global demand, accompanied by a sharper decline in imports, signifying the aforementioned weakness in domestic demand. Chinese companies and families are “shrinking”[2] . The seriousness of the situation led China’s leaders at a Politburo meeting last month to refer to this year’s economic recovery as “torture[3] .”

This poor performance raises several thoughts. The first is that we shouldn’t exaggerate. Just as there was an exaggeration in previous announcements about China as an economic superpower, when its GDP per capita will not exceed 13,000 USD in 2021,[4] while the GDP per capita in the United States is more than 70,000 USD, or even 25,000 USD in Portugal, the opposite exaggeration should not be made either, that China has entered an insurmountable abyss. What is clear is that the Chinese economy is in a moment of correction, as is the case with all economies, possibly requiring profound reforms and political adjustments.

Therefore, the context we have adopted in this work is to consider a crisis in the Chinese economy, but to believe that the right policy choices can overcome this crisis.

At this very moment, hopes of a Chinese recovery from the pandemic have faded, as consumption has generally been very subdued, especially for expensive items such as cars and houses, and private investment, the backbone of China’s economy, fell in the first half of this year for the first time since such data was published. Private companies and entrepreneurs aren’t spending much on investment or hiring staff. Youth unemployment has reached 21 per cent. The annual graduation of 11 to 12 million students this summer will exacerbate an already difficult situation because of the problems of finding suitable work and also because the Chinese labour market has become one in which most jobs are low-paid, low-skilled or in the informal economy.

It seems wrong to attribute all this to the pandemic. Most of the threats to China’s economy were growing a few years ago. The fundamental problem is that China has generated, over the last decade or more, a mountain of bad debts, unprofitable and uncommercial infrastructure and real estate, empty flat blocks, underused transport facilities and overcapacity, for example in coal, steel, solar panels and electric vehicles. Productivity growth has stagnated and China can boast one of the highest levels of inequality in the world[5] .

Furthermore, under Xi Jinping, it developed a more intense, state-centred and controlling system of governance, both for political reasons and to deal with the effects of its ailing development model.

We wonder to what extent the political interventions to limit billionaires like Jack Ma[6] have been positive for the economic environment. Whilst it’s true that they have averted the Russian danger of oligarchic state domination and signalled to the general population that power is concerned about excesses, it’s also true that they have sent a chill down the entrepreneurial spirit necessary for a competitive economy. Everyone will be afraid of growing too much, of being too conspicuous and, ultimately, of innovating. Because innovation and excessive attention can have negative repercussions.

In a way, the “animal spirit” that Keynes spoke of as the engine of any healthy economy has been “tamed” in China and this may be the main problem of its economy, which is neither measurable nor solvable with technical measures.

Chinese reaction and other possible directions

For the time being, China has announced the suspension of the release of the official unemployment rate among China’s urban youth aged between 16 and 24, which reached a new all-time high of 21.3 per cent in June. The State Council published new guidelines for stepping up efforts to attract foreign investment. And the central bank lowered interest rates[7] .

None of these measures seem to have the strength to reverse the cycle of decline in the Chinese economy.

Many authors argue that a huge fiscal stimulus would be needed to energise the economy, which should not be translated into more debt, but into pure “printing” of money, which makes sense in a situation of deflation. A kind of “helicopters with money” flying over the cities and dropping it off.[8]

It is also possible that this crisis will force the Chinese president to revise his policy towards the large economic groups and the business community in general, opting, like Lenin a century ago, for a new liberalisation and flexibilisation, while also seeking to ease the tension that has been building up between China and the United States.

In fact, we believe that a good part of the solution to China’s current economic problems lies in politics rather than economics, and in both domestic and foreign policy. Probably the best way out of the crisis would be to reintroduce the more ambiguous and flexible system of Jiang Zemin’s time. Jiang Zemin, president of China from 1993 to 2003, is considered “the man who changed China”. Many Chinese who grew up in the 1990s remember Jiang Zemin for overseeing China’s entry into the World Trade Organisation, and also for allowing the film Titanic to be broadcast. During the Asian financial crisis, Jiang emphasised the importance of finance and financial security for China’s national security and the building of a modern economy. At the same time, this did not imply a lessening of the power of the Chinese Communist Party and its political control. Some authors point to his tarnished record in relation to human rights and freedom of expression. Zemin oversaw the repression of national dissidents, the banning of religious groups such as Falun Gong and the suppression of the press and the Internet, and also maintained an uncompromising stance on Taiwan[9] .

The advantage for Jiang Zemin’s China is that he was able to maintain a balance between liberating market forces and innovation, and the Communist Party’s control of China.

And our opinion is that a large part of the Chinese crisis is not the result of economic factors alone or above all, but of the loss of that balance point that needs to be recovered.

Obviously, this doesn’t just depend on the Chinese leadership, but also on a change in the external situation of quasi-confrontation between the United States and China.

It’s well known that since the time of Donald Trump there has been a shift in US foreign policy towards China. What seemed like “Trumpism” became a central US policy under Joe Biden and today the United States sees and treats China as a potential future enemy that must be contained. Naturally, this coincided with Xi Jinping’s nationalist assertion, which abandoned the previous external caution, and began to want a strong China in the world context and without complexes, wanting the country to be a post-hegemonic alternative to the United States. So on both sides we had a voluntary confrontational initiative.

The question that arises is whether it is possible to retract and create a new space for US-China collaboration, which will certainly increase China’s prosperity, or whether the course is definitely strategic confrontation? In this confrontation, China will tend to compartmentalise and close itself off, losing the capacity for innovation linked to entrepreneurship, which increases the chances of conflict (more or less direct war) and hinders any Chinese economic recovery.

Impacts in Angola

This is the real situation of the Chinese economy at the moment. As mentioned, the fundamental “brakes” on growth seem to be twofold: from an economic point of view, excessive debt, and from a political point of view, which seems more important to us for the medium and long term, the accentuation of the force of political power in the economy and society, and the political condemnation of entrepreneurship and innovation.

Faced with this scenario, Angola is confronted with advantages and disadvantages that act dynamically.

One advantage is Luanda’s rapprochement with the United States and its relations with China. Angola could be a bridge country for a reunion between the two powers, a kind of proving ground where both can co-operate, compete and survive for mutual benefit. However, it could also become a disadvantage for the same reason, with Angola becoming one of the areas of dispute between the two powers, both wanting to pull it into their sphere of influence. This would be another difficult balance for João Lourenço to maintain.

In economic terms, there will be a possible tendency for the Chinese authorities to become more inflexible in relation to foreign debts, and this may already be happening with Angola, or could happen in the future. This is the normal reaction of countries in a “squeeze.” There is therefore the danger of greater Chinese pressure in economic terms on Angola, which could jeopardise Angola’s once again perilous public finances.

The “tree of patacas” spirit that prevailed in China-Angola financial relations from 2002 onwards is definitely over and will not be recovered. China will behave towards Angola, in greater or lesser detail, like any other international creditor, and its pressure will increase as the Chinese domestic economic situation deteriorates. Another challenge for João Lourenço.

One advantage that Angola could offer China is the creation of a large labour market for its young graduates. Cooperation agreements could be made to put Chinese people in Angola to train Angolan staff and help implement policies in areas such as public administration, in which China has millennia of experience, or telecommunications and information technology.

The Chinese civil service system has provided stability for the Chinese empire for more than 2,000 years and has provided one of the main outlets for social mobility in Chinese society. Today, in the 1980s, it has made a successful transition from a centralised Marxist economy to a mixed economy with strong growth.

China has also become one of the largest telecoms markets in the world, with more than one billion Internet users and monthly revenues of more than 130 billion yuan from the telecoms sector. The country has undergone several waves of reforms over the last three decades to liberalise and privatise its telecommunications industry. It is the experience gained in this immensity that can be put at the service of Angolans.

In these terms, the current phase of China-Angola relations could partly leave physical capital behind and centre on human capital, showing that relations between countries can mature. Angola could provide an outlet for Chinese companies and their young people.

What we have to realise is that the relationship is entering a “mature” phase in which each country has its own interests to defend. China will no longer bring “rains of money”, but rational investments, and this is what Angola must count on and counter. In fact, in terms of future markets, investment opportunities and an escape from China’s problems, Angola has a lot to offer and can be the “bargaining chip” in various negotiations.

[1] https://www.cnbc.com/2023/08/14/china-economy-new-loans-fall-property-fears-low-consumer-sentiment-.html

[2] https://www.cnbc.com/2023/08/17/david-roche-chinas-economic-model-is-washed-up-on-the-beach.html

[3] https://www.theguardian.com/business/2023/aug/11/china-economic-problems-show-things-are-seriously-amiss

[4] https://www.ceicdata.com/pt/indicator/china/gdp-per-capita

[5] On the structural and long-term problems of the Chinese economy see Frank Dikotter, China after Mao – The rise of a superpower, 2023.

[6] https://www.forbes.com/sites/georgecalhoun/2021/06/07/the-sad-end-of-jack-ma-inc/

[7] https://www.nytimes.com/2023/08/15/business/china-economy-downturn-unemployment.html, https://www.bloomberg.com/news/features/2023-08-20/xi-jinping-is-running-china-s-economy-cold-on-purpose?in_source=embedded-checkout-banner,

[8] Rui Verde, Helicópteros com dinheiro, 2013

[9] https://www.cfr.org/blog/jiang-zemin-put-chinas-economic-opening-practice

Recent economic turmoil

The results of Angola’s economic policy, which had been favourably received by international institutions and public opinion in recent times, namely low inflation, fiscal consolidation, control of public debt and the success of foreign exchange liberalisation, seemed to suffer a blow in June.

The trigger for this change in perception was the abrupt announcement of the rise of more than 80% in the price of commercial petrol, due to the partial withdrawal of the state subsidy (without the necessary focus on the mitigation measures that had been well thought out), which was followed by a series of cascading events, the resignation of Manuel Nunes Júnior as Minister of State for Economic Coordination, some rumours about delayed public service salaries, and inevitably the announcement by a rating agency that Angola’s economic outlook had been downgraded from “positive” to “stable”.[1]In addition, the Kwanza is depreciating rapidly against the dollar and the euro. At the end of June, the Angolan national currency passed 800 kwanzas to the dollar for the first time.[2]

The depreciation of the kwanza has raised renewed fears of inflation, in a country still heavily dependent on imports for its daily life. Last February, the National Bank of Angola said that the country would spend over US$2 billion (1.8 billion euros) on food imports in 2022, representing a 40 percent increase over the previous year.[3] A lower value of the national currency and a rise in food import requirements obviously results in higher prices.

In turn, the statement that the new Minister of State and Economic Coordination made about the delays in some public salaries in May, did not reassure, since Lima Massano assured that this was due to “a time lag between the time of receipt of the funds resulting from tax collection and the period of payments.”[4] The minister’s explanation is not contested, the problem is that even if we accept it, it contains a problem, which is that of the government’s lack of cash reserves, indicating that the budgetary restraint imposed by the International Monetary Fund (IMF) has not created any space for Angolan public finances. It should be noted that although the price of oil is not very high, over the last six months it has fluctuated between USD 70 and 80, with prevalence at USD 75/76. As the State Budget was based on 75 USD (which we criticised at the time[5] ), the truth is that the price has been in line with the forecast, although with no margin for manoeuvre.

The possible effect of oil prices

In the light of the above, in theory, the price of oil will not yet have a negative effect on the State Budget in the immediate future.

However, this could happen in the second half of the year. We have formed the opinion that there is a strong downward pressure on the price resulting from the oil embargoes on Russia and probably Iran. Our thesis is that these Western oil embargoes do not have the effect of significantly restricting the supply of that product by Russia, which would push up the price of oil, but rather of selling it at a discount to intermediaries who act as “laundromats”. This means that the longer the oil embargo on Russia lasts, the more Russia will make the circumvention mechanisms efficient and the more it will sell oil at a discount. Thus, it is very possible that there will continue to be downward pressure on the price of oil, especially if China’s economy continues not to show the strength of the past.

Consequently, it may be that fiscal tightening will intensify in the second half of this year if oil prices succumb to these pressures.

The doctrinal and practical problem

The concrete fact is that IMF “recipes” in Angola seem to have failed, and once again the application of classical economic doctrines does not work.

It is increasingly clear that a universal theory of economics based on the classical thinking disseminated by North American universities may work in mature developed economies or in places with relatively solid institutions (market, government, courts), but it does not work in countries still suffering from extreme imbalances and under institutional construction. It cannot speak of true markets functioning freely according to the rules of supply and demand, nor of efficient governance or even of a justice system approaching that which works in Angola. For various reasons, these are unfinished processes in the making. To that extent, any economic model that takes them as preconditions will fail. That is why the IMF measures fail, failing to bring prosperity to Angola and making the country go from one crisis to another. It should be stressed that since 2009 the IMF has been monitoring and agreeing with Angola’s economic policies.

There is a doctrinal problem underlying the negative impact of economic policy in Angola that is linked to the fact that the main decision-makers are trained in foreign universities that adopt institutional models of the market economy, with greater or lesser state intervention, but always assuming that the situation is operating normally. The truth is that Angola is in a pre-institutional situation, so the models to be applied should be those of development and institutional building rather than stabilization. This problem, while seemingly very theoretical, has real practical relevance, since something is being applied that has little to do with reality.

Furthermore, some fundamental structural reforms were not undertaken by the government. A system marked by the interference of politicians in the running of companies was maintained, with continued investment in oligopolies that are essentially importers, justice was not speeded up and bureaucracy was clearly not reduced.

The combination of these factors means that the Angolan economy has not yet emerged from the oil cycle and from repeating past mistakes.

The questioning of Agenda 2050

It is these basic deficiencies that appear to limit the effect of Agenda 2050. In a previous report we praised the unassuming and honest way in which the authors of the Agenda made the diagnosis of the past and present situation[6] , and we had some anticipation in reading the proposals for the future.

It is evident that Agenda 2050[7] has many interesting objectives and profound analyses that stimulate the debate, which should be broadened in Angolan society. However, at its core the document does not bring us the necessary ambition and has the defect of being based, as we have mentioned, on generalist models.

If we notice the essential core of the strategic objectives is hardly mobilising. The predicted increase until 2050 of the GDP is 2.4 times, which in terms of GDP per capita, assuming that the population growth is only 2.1 times (and may be much more) results in an increase from USD 3,675 to USD 4,215 of the mentioned GDP per capita. If we look at this, it is a rise in population welfare of only 14% in 27 years[8] . Add that unemployment will still be around 20%. An extremely high figure, although the statistical formula used by the National Statistics Institute of Angola (INEA) cannot be compared with others because it is more demanding and therefore presents more negative results .[9]

It is very discouraging. In fact, in view of the increase in population, what Agenda 2050 is putting as a goal is a quasi-progression. Is it not possible to do differently?

Angola in 2050 is supposed to be similar to what today are countries like Paraguay, Jordan, Sri Lanka, Essuatini or Mongolia[10] . We cannot subscribe to this vision, which in practice envisages a stagnant country where a sharper rise in population will pose severe problems.

Conclusions

In all independence and objectivity, we believe that this future Agenda should be fundamentally revised and substantially altered with the participation of the Economic and Social Council, the various study centres working on Angola in universities and elsewhere, and the country’s living forces, with a view to presenting a model that is both ambitious and feasible for Angola’s future. Only in this way will the current problems resulting from bad doctrinal models and little structural reformism be overcome.

Further and faster has to be the motto of the future.

[1] https://www.noticiasaominuto.com/economia/2347975/fitch-piora-perspetiva-de-evolucao-de-angola-para-estavel

[2] https://www.dw.com/pt-002/angola-queda-hist%C3%B3rica-do-kwanza/a-66037342

[3] https://www.jornaldenegocios.pt/economia/mundo/africa/angola/detalhe/angola-importou-mais-40-de-alimentos-no-valor-de-mais-de-dois-mil-milhoes-de-dolares-em-2022

[4] https://www.angonoticias.com/Artigos/item/74007/ministro-de-estado-esclarece-atrasos-salarias-no-pais

[5] https://www.cedesa.pt/2022/12/20/analise-da-proposta-de-orcamento-geral-do-estado-de-angola-para-2023/

[6] https://www.cedesa.pt/2023/06/11/estrategia-angola-2050-uma-analise-i/

[7] https://www.mep.gov.ao/angola-2050

[8] Idem, note 7, p. 22.

[9] https://www.makaangola.org/2023/05/desemprego-o-erro-das-politicas/

[10] Countries that currently have a GDP per capita close to 4125 USD. GDP, Per Capita GDP – US Dollars”, and 2018 to generate the table), United Nations Statistical Division.

Social life in Angola is very alive and, at this moment, political and judicial matters dominate the country’s agenda. However, it is in the domain of the economy that there is an extremely significant evolution on which it is important to reflect and proceed to a careful analysis.

The recent (February 2023)[1] International Monetary Fund (IMF) report on the country underlines the favorable advances of the Angolan economy and also the necessary reforms. It is based on this report that we will enunciate Angola’s main trends in the economic field and the neuralgic points to avoid relapses such as the last long recession that began in the presidency of José Eduardo dos Santos.

Positive Trends

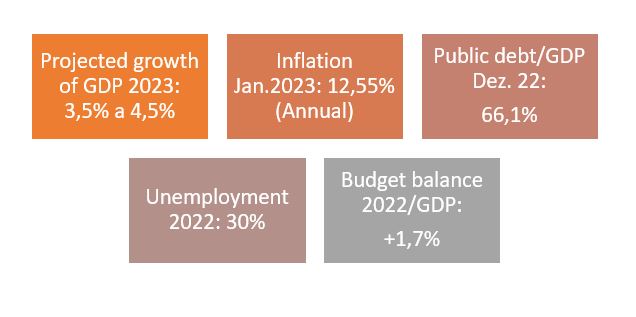

Angola’s economy is in full recovery after the five-year recession (2016-2020). By 2022, supported by higher oil prices and resilient non-oil activity, it has already reached growth of more than 3%, estimating the IMF that by 2023 the country continues to see the GDP increase in the order of 3.5%.

Therefore, we see growths of over 3% per year, which by our calculations, maintaining the price of oil and accelerating the liberalization of Angolan markets and foreign investment, could accelerate to numbers of 4% or 5%, adopted that are the right policies.

The optimism we share here results from the fact that non-oil growth has been widespread, despite a difficult external environment, as it means that the non-oil sector is reviving, as well as the attention that several developed countries with market economies are providing Angola, as is the case of US, Spain, France and Germany. Mentions should be made to recent visits to Angola of the King of Spain and the President of the French Republic, Emmanuel Macron (February and March 2023).

It should be noted that the debt that the public debt/GDP ratio has dropped about 17.5 percentage points of GDP, for an estimated 66.1% of GDP, aided by a stronger exchange rate. It is estimated that the checking account remained with a large surplus in 2022, while coverage of foreign currency reserves remained adequate (IMF data).

The fact is that the Angolan government has, according to the IMF, to adopt and maintain solid macroeconomic policies and maintained a commitment to structural reforms that are vital to Angola’s economy.

Necessary reforms

We understand that it is in the verification of fundamental structural reforms that resides the future of the Angolan economy. We highlight some reforms that are necessary to take and/or continue.

1-First renovation, with impact on the medium and long term, is to foster training for the economy of young people. Training not only means, and perhaps not in most, university education, but solid training in basic education and in professional aspects. We argue, therefore, that there must be an effective bet on vocational and technical education in Angola, before any other. A real bet on professional and technical schools and institutes, which are seen as valuable alternatives to academism and not mere university imitations (tragic error of Portuguese polytechnics).

2-Second renovation entails the creation of more conditions for investment, no longer at the legal level, where there is a modern framing and updated twice during the presidency of João Lourenço, but at the judicial, administrative and good practices level. The investor must feel safe to arrive in Angola and apply his money. One should not be afraid of being without the money due to any interference from an oligarch, or see any process dragging on in court. The speed and impartiality of justice is linked to good investment.

3-Third reform is dedicated to the financial sector, there is a special emphasis on increase credit to private persons and and the resolution of banking weaknesses. Quickly we must merge and capitalize banks, creating a banking sector not dependent on the state, clientelism or mere public debt management.

Finally, among other reforms, we highlight the true imperative of making more progress in strengthening governance and transparency, to improve the business environment and promote private investment.

Of course, continuing and accelerating anti-corruption strategy is also important.

National Employment Plan

All these news should be framed with the well-being of the population and the serious problems still pending. The one we highlight is unemployment, which although noting a slight descent, is still very high, about 30% [2]. This is an area in which we advocate direct state intervention. It is evident that the increase in GDP corresponds to an unemployment decrease, however, we believe that in the face of such high unemployment, in the short term the immediate action of the government is fundamental.

In this sense, the recent announcement of the World Bank of US $ 300 million for a project to accelerate economic diversification and job creation[3] is to greet. Not knowing in detail the design of this acceleration program, its existence should be underlined, as well as the previous announcement of the Angolan Labor Minister of the creation of a National Employment Program, with the aim of creating more opportunities for insertion of young people in job market[4]. Also, in this case, the data are scarce about the design of the plan, and it is certain that the President of the Republic had declared in the discourse of the State of the Nation of 2022, the creation of the referred plan.

So far, these initiatives related to unemployment, although positive, seem uncoordinated and poorly implemented. Therefore, the truth is that Angola would win to see a comprehensive national employment plan, specific and directly coordinated by the President of the Republic, without the risk of not properly implemented a plan, which in the short term is fundamental to the economy and Angolan population.

Fig.N. º1- Key Numbers of the Angolan Economy

[1] https://www.imf.org/en/News/Articles/2023/02/23/pr2352-angola-imf-executive-board-concludes-2022-article-iv-consultation-with-angola

[3] https://correiokianda.info/banco-mundial-financia-usd-300-milhoes-para-fomento-do-emprego-em-angola/

[4] https://www.jornaldeangola.ao/ao/noticias/programa-nacional-de-emprego-e-implementado-este-ano/

Constitutions do not solve problems, but give powerful signs. It is of these powerful signs that Angola’s economy needs at this time.

If we look at the great macroeconomic data, we come across an encouraging picture. Inflation since March 2022 slowed from 27.66% to 13.86% in December 2022, an impressive data, Kwanza, the national currency, oscillates freely in the international market, the State General Budget has a surplus, public debt came down markedly, for a value close to 60% of GDP. The economy grew again in the orbit of 3% by 2022, predicting an increase of 2.7% in 2023. However, oil continues to rise, 86.27 the barrel/brent (25-01-2023).

Therefore, those who can be considered the “fundamental” of the Angolan economy are healthy after a long shortage which began in 2015/2016.

However, the international investment that should flow to Angola is not reality yet, and the threat of instability is latent, as the interview of opposition leader Adalberto da Costa Júnior demonstrates to a Portuguese newspaper [1] last week, not recognizing Electoral results, courts and, therefore, and from what one apprehends any institution of the State; in practice, assuming as possible a power outlet by force.

Consequently, we have a work of meritorious economic stabilization that for political reasons, as well as those that Keynes called “Animal Spirits” (emotions that determine human behaviour), does not produce the desired effects and usually described on economics manuals.

Now, it is precisely this need to unleash the “animal spirit” that does not move in the Angolan economy and the threats of political instability that gives rise to the urgency of discussing a new Constitution to Angola.

It is well known that the Angolan Constitution approved in 2010 is not consensual and was designed in a legal tailoring taking into account the figure of José Eduardo dos Santos, introducing, what Jorge Miranda, the famous Portuguese constitutionalist, dubbed “simple representative government system, to which, diverse configurations were reappointed the French Cesarian Monarchy of Bonaparte, the Corporate Republic of Salazar according to the 1933 Constitution, the Brazilian Military Government according to the 1967-1969 Constitution, several African authoritarian regimes.”[2]

Although having suffered a review in a more democratizing and open sense in 2021, in which the autonomization of the Central Bank stands out and the creation of a constitutional system of supervision of the executive branch by the legislature, it is certain that the constitutional genesis prevents always whenever this is a symbol of an open society and a free economy and on the other hand, it contains no mechanisms of constitutional protection as proposed by Karl Loewenstein and adopted in the German Basic Postwar Law. These mechanisms protect the constitution of internal threats to the constitution itself and are a fundamental element for political stability.

In addition, it is important to reinforce the mechanisms of defense of private and foreign investment. If we notice, private investment is only mentioned once in the Constitution in Article 38, and the history of opportunism and true “theft” of foreign investors in Angola was a reality that requires special normative attention. Also the provisions on the land (article 15) must be updated and rationalized, as well as the guarantee of justice with rapid and impartial judgments.

Justice is admittedly one of the essential aspects of a proper functioning of the economy, expecting predictable and timely decisions. There is no doubt that the Angolan judicial system needs a large “aggiornamento” that would be introduced by a new constitution.

In a mere economic perspective, it is clear that a new constitution would be a sign, a symbol of a new time that would attract investors and give hopes of political and legal stability.

As mentioned at the beginning, a new constitution does not solve all problems, its role is to announce a new time open to investment, market economy and progress and development of the country. It would be the culmination of economic reforms recently enclosed.

[1] Adalberto da Costa Júnior, 2023, Nascer do Sol, https://sol.sapo.pt/artigo/790625/houve-muita-pressao-para-tomar-as-instituicoes

[2] Jorge Miranda, A Constituição de Angola de 2010, CJP-CIDP, p. 42

It is a fact that the war in Ukraine is affecting the entire world economy, and, certainly, this impact will also have political consequences[1], as the International Monetary Fund (IMF) immediately recognized.

The question that will be addressed in this report is about the specific impact of the war on the Angolan economy, which, as we know, is undergoing a demanding reform period and is about to emerge from a deep crisis. It will also superficially assess whether the economic impacts will have political influence.

The two faces of the impact of the oil price in Angola

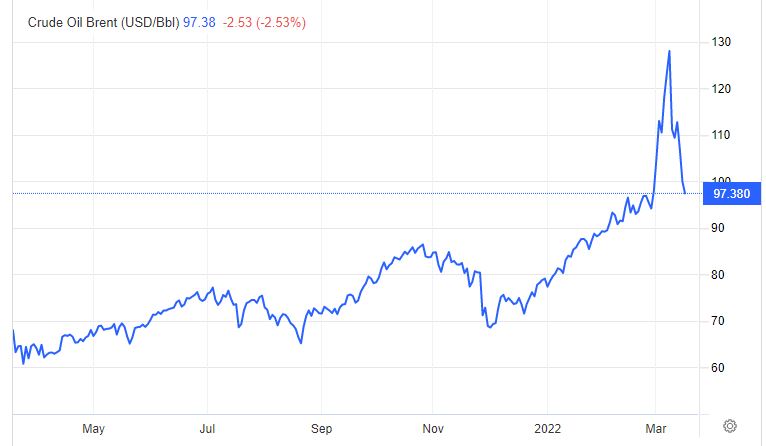

Naturally, the first impact in Angola refers to the price of oil. The rise in the price of oil was a trend that had been going on for some time and was accentuated with the outbreak of the war. To some extent, it is not a novelty brought about by the Ukrainian crisis, but a direction that has been underway for months.

On January 31, 2022, the price of a barrel of Brent was USD 89.9, on February 14, 2022, the value was USD 99.2. It is a fact that with the beginning of the war it reached USD 129.3 on March 8. At this point (March 16), it stabilized at USD 99.11. It seems that the equilibrium price of oil in the near future will be between USD 95-100, with, obviously, the possibility of shocks that make it rise or fall abruptly.

Fig. nº 1- Daily Chart of the Price of a Barrel of Brent (May 2021-March 2022)

Source: Trading Economics.com

In relation to Angola, we have to start from the budgeted forecast for 2022, which calculated the price of a barrel at USD 59. Therefore, there will be an added value since the beginning of the year corresponding to a minimum of 50% more. In this sense, as the budget was balanced, it means that there will be a financial surplus, which is obviously good news.

This rise in the price of oil therefore has, in the first place, two positive effects for Angola.

The first is at the level of extraordinary Treasury revenue, which will naturally increase. In simple terms, it can be said that there will be more money available from the state.

The second effect, which is already being felt, is the so-called “feel good factor” (or confidence index). Entrepreneurs and families are rethinking their expectations in a more positive direction, hoping for better signs from the economy. According to the Angolan National Statistics Institute, businesspeople are finally optimistic about the short-term prospects of the national economy, after remaining pessimistic for more than 6 years[2]. The rise in the price of oil is not the only reason for the optimism revealed, but it helps.

Note, however, that oil price gains do not translate directly into a positive budget balance. There are several constraints in translating the rise in oil prices into direct budgetary benefits for Angola.

The first of these is the type of relationship with China. China is the main buyer of Angolan oil. We do not know how the contracts are made and whether they automatically reflect price fluctuations. In the past, some intermediaries in the purchases and sales of oil to China even entered into fixed-price contracts that greatly harmed the Angolan Treasury[3]. It is imagined that such “schemes” no longer exist, but there are no certainties. What is certain is that, probably, the contracts between Angola and China regarding oil will contain some type of “dampers” that will imply that there is no direct impact on prices. Furthermore, some oil experts, such as those at Chatham House, believe that the fact that China buys around 2/3 of Angolan oil (actually 70%[4]) allows it a certain monopolistic control of the price, meaning that Chinese purchases are made in order to lessen price rises, undermining Angolan advantages[5].

Second, we have debt service. Apparently, there are contractual mechanisms that imply that a higher price of oil implies an increase in debt service, that is, in payments to be made. The Minister of Finance, Vera Daves, has already acknowledged that “what results from the price increase cannot be made an arithmetic account with production” and that the price of a barrel of oil, above one hundred dollars, forces Angola to pay more to their international creditors[6].

Furthermore, the rise in the price of oil also has a possible negative effect on the Angolan budget, which refers to the price of fuel sold to the public. As is well known, this price is subsidized by the State; to that extent, if the cost of oil increases and the government does not increase fuel, it means that it will have to bear more subsidies and spend more to maintain fuel prices. If you don’t, you could be fueling inflation, which is no longer low in Angola, and creating social problems and discontent.

There are four factors here: price increase, relations with China, increase in debt payment obligations and increase in fuel subsidy that have to be taken into account to assess the real impact of the rise in oil prices on the accounts and the Angolan economy.

In fact, we do not have precise figures on these impacts, only ideas of magnitude, and in view of these, the conclusion that can be drawn is that a 50% increase in the price of oil in relation to what is foreseen in the Budget leaves a treasury slack that is still accentuated after the increase in debt service payments and support for the rise in fuel prices, and it is undoubted that a financial “cushion” will be created.

The question of food prices

Alongside the price of oil, many other commodity classes are rising in price. One of them is cereals, namely wheat.

Ukraine and Russia together account for a quarter of all world wheat exports. The conflict is dramatically driving up wheat prices. With the start of the war, the price of a bushel of wheat rose to $12.94, 50% more expensive than at the beginning of 2022.

In the midst of a war, it is unclear whether Ukraine’s farmers will be willing to spend whatever capital they have to plant the next harvest, or even if they will be in a position to do so. What is certain is that Ukraine has announced a ban on all exports of wheat, oats and other staple foods to avoid a massive food emergency within its borders. Therefore, wheat exports from Ukraine, even if there is production, are compromised.

Unlike oil, which affects prices almost immediately, grain prices take weeks, if not months, to reach consumers. In reality, raw grain needs to be shipped to processing facilities to make bread and other staples – and that takes time. In this sense, possibly, it will not be an immediate crisis for Angola, but it will reach the country.

According to government sources, Angola is self-sufficient in six basic agricultural products: cassava, sweet potato, banana, pineapple, eggs and goat meat. However, wheat is the most imported commodity, accounting for 11%[7]. Let us recall that wheat is an essential element in the diet of Angolans, which a few months ago led the Minister of Industry and Commerce to suggest replacing bread with cassava, sweet potatoes, roasted bananas and “ginguba” (peanuts). This statement has generated much criticism. However, from the strict point of economic self-sufficiency it may make sense, since possibly the price of bread will rise and eventually the price of national goods may fall, if there is an adequate competitive market.

What is certain is that Angola could be in the same danger as Egypt, an extremely wheat-based crop that suffers social upheaval when the price of wheat rises.

When grain prices soared in 2007-2008, bread prices in Egypt rose by 37%. With unemployment on the rise, more people became dependent on subsidized bread – but the government didn’t react. Annual food inflation in Egypt continued and reached 18.9% before the fall of President Mubarak.

Most of the poor in these countries do not have access to social safety nets. Bread images became central to the Egyptian protests that led to Mubarak’s downfall. Although the Arab revolutions were united under the slogan “the people want to overthrow the regime” and not “the people want more bread”, food was a catalyst. Incidentally, it should be noted that “bread riots” have been occurring regularly since the mid-1980s, usually after the implementation of policies “advised” by the World Bank and the International Monetary Fund.

Angola is not Egypt, but it is essential that the government pay close attention to the evolution of wheat and bread price to avoid social unrest, at a stage when it begins to emerge from the prolonged crisis.

However, as in the case of oil, there is another side, and in this case it is positive. The crisis in agricultural production resulting from the war could be a turning point for foreign investors to invest in agriculture in Angola. Angola is one of the countries in the world with the most potential, as we have already mentioned in a previous report[8], so this may be the time of opportunity for investors to see Angola’s agricultural capacity and take advantage of it. One of the most promising sectors with the most potential is agriculture. There is currently a combination of factors that make it one of the most profitable bets for investment in Angola.

Conclusions and recommendations

The war in Ukraine has several impacts on the Angolan economy.

The rise in the price of oil, not bringing directly proportional revenues, creates a “cushion” in the Treasury and a “feel good factor” in the business community, which could be a growth booster.

The rise in the price of cereals, especially wheat, can create serious inflationary pressures and discontent among the population, a situation for which the government must be aware. At the same time, it will draw attention to the enormous investment potential that Angola has as an agricultural country.

The government should create a special reserve derived from the gains from oil to guarantee the supply of cereals to the poorer sections of the population and also to promote agricultural investment in Angola.

[1] https://www.imf.org/en/News/Articles/2022/03/05/pr2261-imf-staff-statement-on-the-economic-impact-of-war-in-ukraine

[2] https://www.angonoticias.com/Artigos/item/70611/optimismo-regressa-no-seio-dos-empresarios-seis-anos-depois

[3] Rui Verde, Angola at the Crossroads. Between Kleptocracy and Development (2021), p. 24.

[4] https://www.forumchinaplp.org.mo/pt/china-foi-o-destino-de-71-do-petroleo-exportado-por-angola-em-2020/

[5] Explanations given at a Chatham House meeting that we replicate here, respecting the house rules.

[6] https://rna.ao/rna.ao/2022/03/03/preco-do-petroleo-a-cima-dos-cem-dolares-obriga-governo-angolano-a-pagar-mais-aos-credores/

[7] https://www.expansao.co.ao/economia/interior/grupo-carrinho-destaca-se-nas-importacoes-e-exportacoes-do-pais-106709.html

[8] https://www.cedesa.pt/2020/06/15/plano-agro-pecuario-de-angola-diversificar-para-o-novo-petroleo-de-angola/

Many countries don’t need a robust youth policy, either because the youth population is not significant, with most socio-economic problems being in the elderly, or because they have healthy economies and societies that easily encourage and incorporate young people.

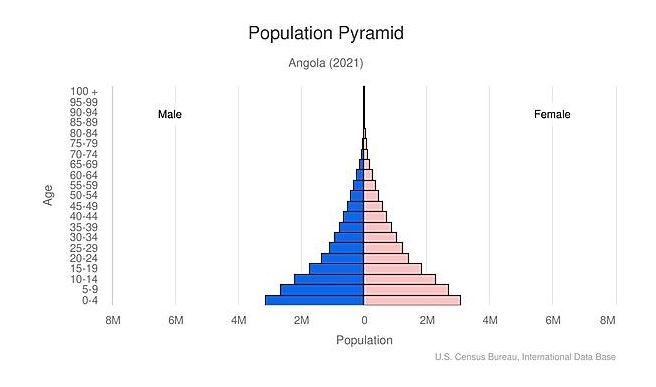

This is not the case in Angola. The numbers on Angolan youth demand special attention from the political power to this age group. With reference to July 2021, it is estimated that 47.83% of the Angolan population is between 0-14 years old and 18.64% between 15-24 years old; therefore, 66.47% of the population is up to 24 years old, or in other words, about 2/3 of the Angolan population is young. It is an immense and impressive mass of babies, teenagers and young adults that constitute the immensity of the Angolan people.[1]

Fig. 1- Angola population pyramid (2021)

This impressive demographic is joined by unemployment figures. According to the most recent data available, unemployment affects 59.2% of the young population (here considered to be aged 15-24) in the third quarter of 2021, with a year-on-year increase in this situation of 2.8%. It is clear that this number does not reflect those who were somehow absorbed by the informal economy, however, its magnitude will always be remarkable[2].

In fact, from a sociopolitical point of view, it has been verified that the demonstrations against the government policy in Angola, and the activism in social networks, is carried out, in large part, by young people.

Youth is, therefore, a huge force in the Angolan economy and societies, which is on the boil.

These various factors: extremely relevant number of young people in the total population, youth unemployment and socio-political discontent that force the consideration of a transversal and encompassing youth policy for Angola.

***

Youth policy is defined as the government’s commitment and practice to guarantee good living conditions and opportunities for a country’s young population[3]. Youth policy is a strategy implemented by public authorities to provide young people with opportunities and experiences that support their successful integration into society and allow them to be active and responsible members of society and agents of change[4].

In these terms, a youth policy seeks to create opportunities for young people, promoting their participation, inclusion, autonomy, solidarity, in addition to well-being, learning, leisure, employment.

The government’s role will be to launch policies with these goals in relation to youth and to work together with the various actors involved in the information, development and implementation of youth policies, such as: youth councils, youth NGOs, interest groups, groups of young people, young workers, researchers, schools, teachers, employers, medical personnel, social workers, religious groups, media[5].

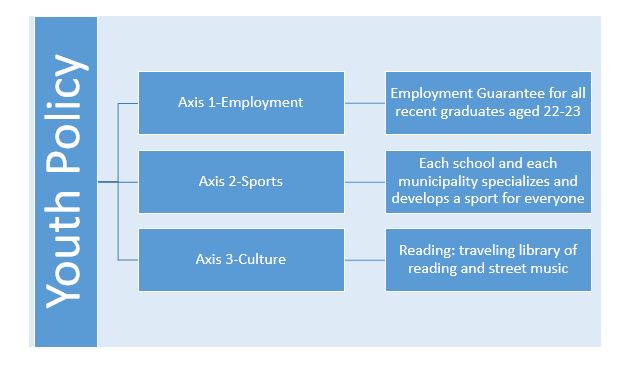

The model we developed attributes three axes to youth policies:

a) The axis of employment;

b) The axis of sport and leisure;

c) The axis of culture and training.

We understand that a youth policy must translate into measures in these three axes in order to provide young people with an integral and complete personal development.

In Angola there is a Ministry of Youth and Sports (Minjud) whose main function is to assist the President of the Republic in the elaboration and execution of the State’s youth policy (Article 2 of the Organic Statute of the Ministry of Youth and Sports, Presidential Decree no. 228/20, of September 7th).

However, in addition to advertisements or programs with a rhetorical value, there is no vision of a transversal and active youth policy such as is needed in Angola. And such a policy is essential. The relevant news that is noted about the activity of Minjud focus essentially on football and football stadiums.

It is therefore urgent to go further and launch a youth policy that will necessarily cover several ministries and will have to be coherent and consistent. As we mentioned, this youth policy would unfold along three axes, paying attention to employment, sports and culture.

***

It is proposed to adopt a youth policy for Angola described in the following terms.

The youth policy would be transversal to several ministries, not dependent only on one ministry, and therefore necessarily coordinated directly by the President of the Republic. As mentioned, it would have three axes that would complement each other.

• In the first axis, referring to employment, a program to guarantee full employment would be launched for all those aged between 22 and 23 years old and having completed a degree. The State would assume the responsibility to employ them in its structure or to subsidize for a period of time not less than 2 years a workplace in the private sector[6]. Therefore, the State would either ensure employment in its several administrations, institutes or public companies, or it would subsidize private companies for the creation and hiring of jobs for young people. All young graduates aged 22-23, in addition to receiving training and assistance to find work, would have guaranteed paid work, with the State having to pay 100% of their salary in a private company or employ participants in the public sector or support creation of a microenterprise. All participants would receive at least a minimum wage fixed in accordance with the Presidential Decree that regulates the subject adequate to a life with dignity[7]. In a second phase, the guarantee of employment for all young people aged 22-23, regardless of their qualification, would also be studied, although those without formal qualifications should attend training to acquire some ability in art or craft.

• In the second axis referring to sports, an integrated sports project in school and in the community would be promoted. In this context, a proposal should not be developed to do everything everywhere, or as referred to in connection with a previous plan “to involve sport modalities of handball, athletics, basketball, football, volleyball, gymnastics and chess” in all schools[8].

The plan would aim at the rational use of scarce resources and with the search for specialization. Thus, each school would be required to dedicate itself to only one sport and to develop it freely within its midst. They would not aim for national championships, nor for large structures, but they would bet on focus and specialization. Each school with its sport. Only one, but open to all young people. At the same time and in competition with schools, each municipality would also promote a sport open to all young people. We would thus have a sport project for everyone with a specialization from each institution and with no other initial ambition other than to put young people in sport.

• Finally, the third axis dedicated to culture would also have to be based on specialization. Here, efforts would be made to concentrate resources on promoting reading by young people. We would start by adopting a project launched by the Gulbenkian Foundation in Portugal in the middle of the last century and already sporadically adopted in Angola in provincial initiatives, such as the “Giro do Saber” promoted by the Provincial Library of Malanje[9].

Reading for youth based on traveling libraries and street readings would be a project aimed at encouraging young people’s taste and reading habits. The traveling libraries will consist of vans that would travel across the country with volunteers and books offered and would stop at each location allowing the reading of these books and explaining some of them. At the same time, these volunteers would perform street readings of books appealing to youth in a mixed spectacle of reading and music, thus attracting target audiences.

One would look for this reading project to be financed by the penal system. That is, it would give rise to a change in the law that would allow all prison sentences of up to two years for economic and financial crimes to be exchanged for donations of vans, books and volunteer support.

Fig. 2- Description of a transversal youth policy

With these measures in the field of employment, sport sand culture, a youth policy that is so necessary for Angola would be launched.

There is nothing like taking advantage of the present party Congresses to promote and discuss these proposals.

[1] Cfr. https://www.cia.gov/the-world-factbook/countries/angola/#people-and-society

[2] https://mercado.co.ao/economia/desemprego-afecta-592-dos-jovens-em-angola-YX1077607

[3] Finn Denstad, Youth Policy Manual, 2009

[4] Conselho da Europa CM / Rec (2015) 3

[5] https://www.coe.int/en/web/youth/about-youth-policy

[6] We have developed proposals for these full-employment programs in other CEDESA reports, see for example https://www.cedesa.pt/2020/11/16/proposta-de-um-esquema-piloto-de-garantia-de-emprego-em-angola/

[7] See the study referred to in the previous note

[8] https://www.angop.ao/noticias/desporto/polidesportivo-desporto-escolar-carece-de-continuidade/

[9] https://www.angop.ao/noticias/lazer-cultura/biblioteca-itinerante-chega-ao-municipio-de-cacuso/

1- Introduction: IMF, sound economic policies and capital accumulation

Contrary to what some economic studies and forecasts currently carried out by some more or less unknown consultants, the current Angolan economic policy has solid foundations. This is demonstrated by the recent assessment by the International Monetary Fund regarding the agreement between the fund and Angola. The IMF administration is clear in declaring[1]: “The authorities [from Angola government] have supported the [economic] recovery through sound policies that aim to further stabilize the economy, create opportunities for inclusive growth and protect the most vulnerable in Angolan society.”

It would be difficult to have a better endorsement of government economic policy.

However, macroeconomic stabilization and the resumption of economic growth are different realities. There is need of a certain engine to ensure economic growth. It is known that the essential growth model was presented by Robert Solow (Nobel Prize for Economics in 1987), that explains that growth depends essentially on the accumulation of capital, with the increase in GDP resulting from the increase in the capital stock[2].

It is known that the latest Angolan GDP figures for the first quarter of 2021 are negative by 3.4%. So the question that now arises is: how to transform sound economic policies into capital accumulation and promote GDP growth?

2-Capital in the Angolan economy

The essential growth model of the Angolan economy, at least from 2021 onwards, was not a model based primarily on investment, but on consumption derived from imports and on the direct benefit of capital gains from the high price of oil. This meant that the investment that existed was induced by oil and not extended to the economy as a whole[3]. It should also be noted that a good part of the savings gains at that time was not transformed into domestic investment, having been transferred abroad from Angola. In a colloquial way, there was a sharp flight of capital from Angola to overseas countries, namely Portugal or off-shore tax havens[4].

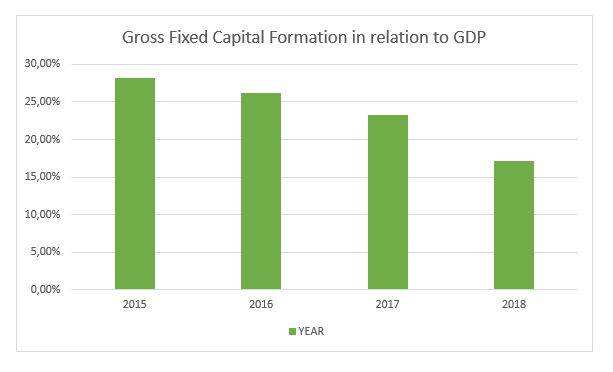

It is public that this model went bankrupt as of 2014, and led to sharp years of recession after 2015. At the same time, it was found that the contribution of gross fixed capital formation (GFCF) to GDP began to decrease from that point on. year (2015). If we look at each year the FCF/GDP was respectively 28.21 %, 26.21 %, 23.24 %, 17.19%. The 2018 number (17.9%) is frightening and makes the discussion about the need to capitalize the Angolan economy more relevant.

Figure 1: Gross Fixed Capital Formation in relation to GDP

“The country has a capital deficit”[5] and this problem has to be resolved so that growth can occur. This aspect has to be one of the guides for future economic policy. A goal must be set to raise the GFCF/GDP rate to higher levels, possibly to the 25/26% that happened in 2007 or 2012, which ensure GDP growth levels (albeit based on oil) of 14% and 8%. Now a new capitalization not only based on oil has to be carried out.

It’s easy to diagnose. Angola lacks capital and needs strong investment. The answers will be the most costly.

3- Increase capital in Angola

What to do to accumulate and increase capital in Angola?

Our answer is divided into two perspectives, the short-term and the medium-term. Let’s focus on the short term, then make a brief reference to the medium term, although it is clear that there is a continuum, as what is done now has repercussions over time.

The executive has already taken some measures, which we have reported in previous reports[6], such as the Private Investment Law (LIP)-Law no. 10/18, of June 26, which no longer requires partnerships with Angolan citizens or companies from Angolan capital and in its article 14, it guarantees that the State respects and protects the property right of private investors; Article 15 establishes that the Angolan State guarantees all private investors access to the Angolan courts for the defense of their interests, being guaranteed due legal process, protection and security. The range of possibilities for transferring dividends were also expanded. Moreover, in administrative terms, it should be noted that in 2018, all requests for the transfer of dividends above five million dollars (4.3 million euros) were granted to foreign companies operating in the country. And, most importantly, since 2020, the capital import from foreign investors who want to invest in the country in companies or projects in the private sector, as well as the export of income associated with these investments, have been exempted from licensing by the Angolan central bank.

However, this is still not enough, and foreign private investment will take a long time, either because a very turbulent electoral period is starting, or because there is a worldwide distraction with Covid-19. In addition, the executive has not yet communicated with all the worldwide amplification, the opening of Angola for business. Even so, it is essential that the executive maintain the political orientation of openness to foreign direct investment.

More needs to be done in the short term to increase investment in Angola and subsequent economic growth. Below is a list of suggestions.

• The initial suggestion is obvious and is based on strengthening public investment. It is essential that the government becomes an inductor of investment and that the capital gains arising from the rise in oil prices and possible apprehensions in the fight against corruption are applied in reproductive investments with short-term results.

The next two suggestions might be more innovative.

Let us address the first of the most unorthodox suggestions. As mentioned, a good part of the savings obtained by Angolans in Angola was remitted abroad, decapitalizing the country. Now we have to reverse this.

• In this sense, the government should, in the first place, sell the dormant shares and assets or in which there is no very relevant strategic interest, which it has abroad. With the result of this sale, it would constitute an investment fund to be invested within Angola. Thus, the first heterodox proposal to increase the capital available in Angola is to sell what there is abroad that belongs to the State (directly or indirectly) and place it in the Angolan economy. Certainly, Sonangol’s position in Millennium BCP should be sold and transformed into investment capital in Angola, and possibly an indirect stake in Galp, if it is not possible to reach a strategic agreement with the Amorim family to better monetize the Angolan position.

• The second suggestion refers to fighting corruption. It is necessary to get out of a certain delay that entered into and boost the capital recovery.

Thus, the government should directly approach those it calls “hornets” and propose a negotiated solution to their situation. Either they deliver the assets that are abroad for investment in Angola, or they will face long prison terms. In relation to these assets, the method outlined above would be followed: Provided market prices were acceptable, everything would be sold and the capital returned to Angola for investment according to a formula agreed between both parties.

This “negotiation” would not be carried out by common means, but by a special force to be set up in Angola and would have short deadlines, not judicial deadlines.

There will have to be a radicalization in both directions in the fight against corruption. More effective punishment or forgiveness with repatriation. Unlike what happened in the previous repatriation law, there would be no waiting, but there would be a proactive attitude on the part of the executive.

By way of an illustration, the participation of Isabel dos Santos in NOS, that of General Kopelipa in the BIG bank and in several hotel developments, the apartments that the former figures have in Estoril, etc., could be sold. The result of these sales would return to Angola where it would be invested in terms to be agreed between the State and the former owners.

These listed measures could give some boost to the Angolan economy and thus promote economic growth immediately.

At the medium-term level, the essential thing is that there is no rampant corruption, good communication infrastructures are created, an investor-friendly legal apparatus and fast, non-corrupt courts, an educated workforce (this does not mean having degree courses but the necessary skills) and reasonable taxes. In short, an inviting political and social climate for investment.

[1] IMF, Fifth review under the extended arrangement under the extended fund facility and request for modifications of performance criteria— press release; staff report, and statement by the executive director for Angola, June 2021, available in https://www.imf.org/en/Publications/CR/Issues/2021/06/30/Angola-Fifth-Review-Under-the-Extended-Arrangement-Under-the-Extended-Fund-Facility-and-461318

[2] Cfr. Recent reassessment and description in Philippe Aghion, Céline Antonin e Simon Bunel (2021), The Power of Creative Destruction

[3] Cfr. Rui Verde (2021), Angola at the Crossroads. Between Kleptocracy and Development

[4] Cfr. For example: Isabel Costa Bordalo, Angola com 60 mil milhões USD é terceiro em África na fuga de capitais, https://www.expansao.co.ao/angola/interior/angola-com-60-mil-milhoes-usd-e-terceiro-em-africa-na-fuga-de-capitais-94979.html

[5] Jonuel Gonçalves (2021), Angola: Não é a Covid que está a provocar a crise económica, https://www.dw.com/pt-002/angola-n%C3%A3o-%C3%A9-a-covid-que-est%C3%A1-a-provocar-a-crise-econ%C3%B3mica/a-58859385

[6] CEDESA, (2020), A nova atractividade para o investimento internacional em Angola https://www.cedesa.pt/2020/03/09/a-nova-atractividade-para-o-investimento-internacional-em-angola/

Indications

The latest figures available from the National Institute of Statistics on the Angolan economy point to a decrease in GDP in the 1st quarter of 2021 in the order of -3.4%, an unemployment rate in the same quarter of 30.5%, and a annual inflation rate for the month of July 2021 of 25.72%[1]. None of these figures that reflect macroeconomic magnitudes are encouraging in the short term.

However, there are other economic and financial realities to consider in order to have a global view of the movement underway in the Angolan economy, and which allow for a more optimistic perspective.

To begin with, in terms of the budget balance and public debt, essential elements of the support program of the International Monetary Fund (IMF), the expectation is that the 2021 budget balance will be positive, possibly above 2% of GDP (further on we will present our prediction). In relation to public debt, as we had predicted in previous reports, its sustainability is consolidated, as recognized by the IMF representative in Angola very recently (see our forecast below)[2].

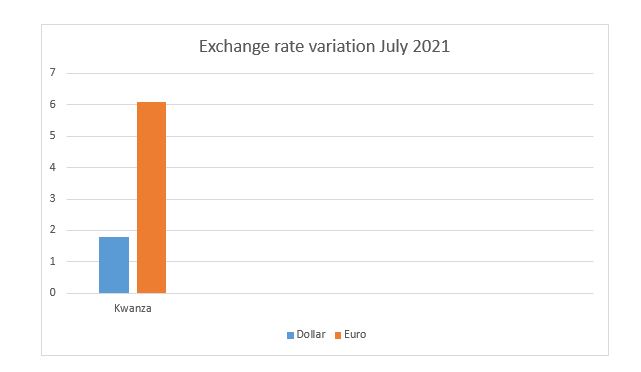

In terms of exchange rate with reference to the month of July 2021, the Kwanza has already appreciated 1.8% against the dollar and 6.1% against the euro, since January 2021, breaking a strong period of strong devaluation started in 2018. Furthermore, 3.5 years after exchange rate flexibility, the gap between formal and informal market rates is below the 20% target announced by the central bank at the time of liberalization, between 7% and 8% for the dollar and euro respectively. Note that at the time prior to liberalization, the same gap was 159% and 167%.

Figure 1 – Kwanza Exchange Rate Variation against the Dollar and Euro (July 2021)

Currently, some sectors are already announcing an increase in the profitability of exports due to the favorable exchange rate policy. This is the case of cement, where Pedro Pinto CEO of Nova Cimangola assures that “To boost exports, the devaluation of the currency helped, because all the costs that the company has in national currency, in dollars, were lower and, in this way, the competitiveness of the company to place products on the international market. In other words, all those products that we continue to buy in Kzs and that have not suffered large price variations in dollars were lower and, therefore, allowed the company to have greater profitability with exports.[3] ”

Also a reference to PRODESI (Program to Support Production, Diversification of Exports and Substitution of Imports), which has generated more than USD 29 million since the beginning of the year. As the main exported products, emphasis is placed on cement, beer, glass packaging, bananas, juices and soft drinks and sugar[4].

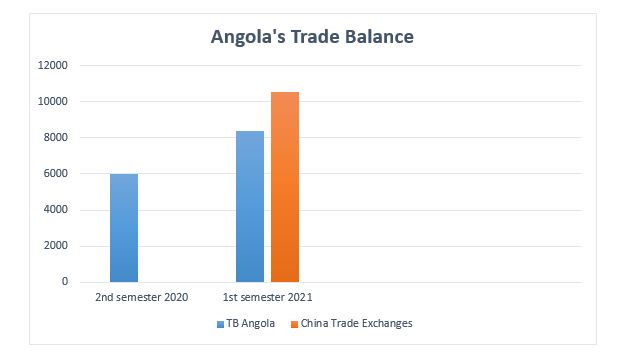

These movements are reflected in the trade balance. Angola’s trade balance recorded, in the 1st half of 2021, a surplus of USD 8,381.9 million[5], an increase of 40.2 % compared to the results recorded in the 2nd half of 2020 (USD 5,978.8 million)[6]. Within this framework, there was an increase in exports of 25%, naturally still influenced by the increase in exports from the oil sector of 28.4%.

Figure 2 – Angola’s Trade Balance and Trade Relations with China

But there is also a significant increase in trade with one of Angola’s main trading partners, China. “Trade between Angola and China increased 23.9% in the first half of 2021, to US$10,550 million (€8,985 million), compared to the same period last year”[7]. According to Gong Tao, Chinese ambassador to Angola, despite the adverse effects caused by the covid-19 pandemic, Chinese companies remain interested in investing in Angola, highlighting the recent construction of factories, one dedicated to the production of tiles and another qualified for the production of energy and water meters.

2021 Summer Forecasts

In modeling the perspectives we present here, several factors are taken into account, among which we highlight the main ones. The first element is the calculation of the oil price (always a determining factor in the Angolan economy). We assume that the price of Brent will maintain a slight upward trend, standing at a level between USD 65 to USD 75 per barrel. A relative stabilization or possible appreciation of the Kwanza against the dollar and the euro is also part of our model, which makes it possible to reverse some of the falls in the past that were merely nominal due to the more flexible exchange rate. We anticipate that the post-Covid-19 world recovery will boost the Angolan economy’s exports, as is already happening with China. Finally, we anticipate that the environment for foreign investment will gradually improve as a result of legislative reforms and the commitment of political power. We have as a recent example the several advertisements coming from Turkey. At the end of July 2021, Angola and Turkey signed 10 cooperation agreements, in the fields of economy, trade, mineral resources and transport, having already announced an increase in the trade balance with Angola to a value of around USD 500 million[8].

From the point of view of obstacles, it is worth mentioning the immense lack of capital. This is the main element for any sustained recovery, and also the inexistence of economic diversification[9] and the persistence of administrative bureaucracy.

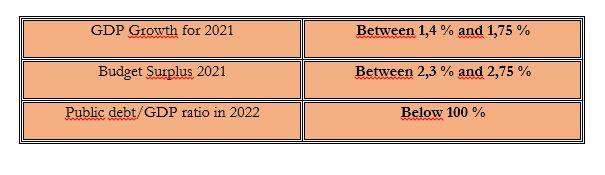

All things considered, our model predicts that by the year 2021 the Angolan economy will come out of recession, and GDP growth will reach between 1.4% and 1.75%.

Our model points to a budget surplus between 2.3% and 2.75%, depending on the evolution of the oil price until the end of the year. And considering the evolution of the Kwanza exchange rate, our forecast is that in 2022, the public debt/Gross Domestic Product (GDP) ratio will be below 100%, achieving greater consolidation.

Figure 3 – CEDESA Model – Forecasts for the Angolan Economy

Consequently, the initial period of strong adjustment and contraction of the Angolan economy is expected to come to an end this year, with no more shocks and global control of the Covid-19 pandemic.

The special case of Unemployment

We understand that unemployment is a special case that should be treated differently, both statistically and in terms of public policies. In terms of statistics, it should be better ascertained who is occupied with informal productive paid activities and who cannot effectively obtain any paid work they want. We should avoid statistical biases that disturb the proper understanding of reality.

On the other hand, it is clear that it will not be the market or the private economy that will solve the problem of lack of employment in the short term, especially for young people. To that extent, the authorities are urged to develop a Keynesian-type employment promotion program, if necessary using available capital from the fight against corruption, as we have advocated in other reports. The state has to spend money on job creation.

[1] Cfr. https://www.ine.gov.ao/

[2] Cfr. https://www.sapo.pt/noticias/atualidade/representante-do-fmi-em-angola-afirma-que_611bf099d1bccf29fd83b48c

[3] https://mercado.co.ao/grandes-entrevistas/a-desvalorizacao-da-moeda-permitiu-que-a-empresa-tivesse-maior-rentabilidade-com-as-exportacoes-XJ1038347

[4] https://www.angonoticias.com/Artigos/item/68811/prodesi-rende-mais-de-usd-29-milhoes-em-exportacoe

[5] https://www.bna.ao/Conteudos/Artigos/lista_artigos_medias.aspx?idc=15419&idsc=15428&idl=1

[6] https://www.angonoticias.com/Artigos/item/68824/balanca-comercial-regista-superavit-de-usd-83819-milhoes

[7] https://www.rtp.pt/noticias/economia/comercio-entre-china-e-angola-recupera-24-no-1o-semestre-apos-forte-quebra-em-2020_n1343994

[8] https://www.angop.ao/noticias/economia/angola-e-turquia-reforcam-balanca-comercial/

[9] Cfr, the most recent elements on the sectoral participation in the GDP that demonstrate the immense and reinforced weight of the oil sector. https://www.bna.ao/Conteudos/Artigos/lista_artigos_medias.aspx?idc=15907&idsc=15909&idl=1