Constitutions do not solve problems, but give powerful signs. It is of these powerful signs that Angola’s economy needs at this time.

If we look at the great macroeconomic data, we come across an encouraging picture. Inflation since March 2022 slowed from 27.66% to 13.86% in December 2022, an impressive data, Kwanza, the national currency, oscillates freely in the international market, the State General Budget has a surplus, public debt came down markedly, for a value close to 60% of GDP. The economy grew again in the orbit of 3% by 2022, predicting an increase of 2.7% in 2023. However, oil continues to rise, 86.27 the barrel/brent (25-01-2023).

Therefore, those who can be considered the “fundamental” of the Angolan economy are healthy after a long shortage which began in 2015/2016.

However, the international investment that should flow to Angola is not reality yet, and the threat of instability is latent, as the interview of opposition leader Adalberto da Costa Júnior demonstrates to a Portuguese newspaper [1] last week, not recognizing Electoral results, courts and, therefore, and from what one apprehends any institution of the State; in practice, assuming as possible a power outlet by force.

Consequently, we have a work of meritorious economic stabilization that for political reasons, as well as those that Keynes called “Animal Spirits” (emotions that determine human behaviour), does not produce the desired effects and usually described on economics manuals.

Now, it is precisely this need to unleash the “animal spirit” that does not move in the Angolan economy and the threats of political instability that gives rise to the urgency of discussing a new Constitution to Angola.

It is well known that the Angolan Constitution approved in 2010 is not consensual and was designed in a legal tailoring taking into account the figure of José Eduardo dos Santos, introducing, what Jorge Miranda, the famous Portuguese constitutionalist, dubbed “simple representative government system, to which, diverse configurations were reappointed the French Cesarian Monarchy of Bonaparte, the Corporate Republic of Salazar according to the 1933 Constitution, the Brazilian Military Government according to the 1967-1969 Constitution, several African authoritarian regimes.”[2]

Although having suffered a review in a more democratizing and open sense in 2021, in which the autonomization of the Central Bank stands out and the creation of a constitutional system of supervision of the executive branch by the legislature, it is certain that the constitutional genesis prevents always whenever this is a symbol of an open society and a free economy and on the other hand, it contains no mechanisms of constitutional protection as proposed by Karl Loewenstein and adopted in the German Basic Postwar Law. These mechanisms protect the constitution of internal threats to the constitution itself and are a fundamental element for political stability.

In addition, it is important to reinforce the mechanisms of defense of private and foreign investment. If we notice, private investment is only mentioned once in the Constitution in Article 38, and the history of opportunism and true “theft” of foreign investors in Angola was a reality that requires special normative attention. Also the provisions on the land (article 15) must be updated and rationalized, as well as the guarantee of justice with rapid and impartial judgments.

Justice is admittedly one of the essential aspects of a proper functioning of the economy, expecting predictable and timely decisions. There is no doubt that the Angolan judicial system needs a large “aggiornamento” that would be introduced by a new constitution.

In a mere economic perspective, it is clear that a new constitution would be a sign, a symbol of a new time that would attract investors and give hopes of political and legal stability.

As mentioned at the beginning, a new constitution does not solve all problems, its role is to announce a new time open to investment, market economy and progress and development of the country. It would be the culmination of economic reforms recently enclosed.

[1] Adalberto da Costa Júnior, 2023, Nascer do Sol, https://sol.sapo.pt/artigo/790625/houve-muita-pressao-para-tomar-as-instituicoes

[2] Jorge Miranda, A Constituição de Angola de 2010, CJP-CIDP, p. 42

https://www.cedesa.pt/wp-content/uploads/2023/02/constiy.jpg446665CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2023-02-03 13:24:452023-02-03 13:25:09The Angolan economy and the need for a new constitution

1-Introduction: IMF, sound economic policies and capital accumulation

Contrary to what some economic studies and forecasts currently carried out by some more or less unknown consultants, the current Angolan economic policy has solid foundations. This is demonstrated by the recent assessment by the International Monetary Fund regarding the agreement between the fund and Angola. The IMF administration is clear in declaring[1]: “The authorities [from Angola government] have supported the [economic] recovery through sound policies that aim to further stabilize the economy, create opportunities for inclusive growth and protect the most vulnerable in Angolan society.”

It would be difficult to have a better endorsement of government economic policy.

However, macroeconomic stabilization and the resumption of economic growth are different realities. There is need of a certain engine to ensure economic growth. It is known that the essential growth model was presented by Robert Solow (Nobel Prize for Economics in 1987), that explains that growth depends essentially on the accumulation of capital, with the increase in GDP resulting from the increase in the capital stock[2].

It is known that the latest Angolan GDP figures for the first quarter of 2021 are negative by 3.4%. So the question that now arises is: how to transform sound economic policies into capital accumulation and promote GDP growth?

2-Capital in the Angolan economy

The essential growth model of the Angolan economy, at least from 2021 onwards, was not a model based primarily on investment, but on consumption derived from imports and on the direct benefit of capital gains from the high price of oil. This meant that the investment that existed was induced by oil and not extended to the economy as a whole[3]. It should also be noted that a good part of the savings gains at that time was not transformed into domestic investment, having been transferred abroad from Angola. In a colloquial way, there was a sharp flight of capital from Angola to overseas countries, namely Portugal or off-shore tax havens[4].

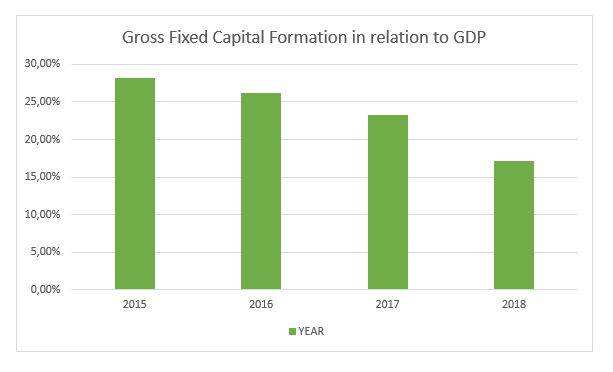

It is public that this model went bankrupt as of 2014, and led to sharp years of recession after 2015. At the same time, it was found that the contribution of gross fixed capital formation (GFCF) to GDP began to decrease from that point on. year (2015). If we look at each year the FCF/GDP was respectively 28.21 %, 26.21 %, 23.24 %, 17.19%. The 2018 number (17.9%) is frightening and makes the discussion about the need to capitalize the Angolan economy more relevant.

Figure 1: Gross Fixed Capital Formation in relation to GDP

“The country has a capital deficit”[5] and this problem has to be resolved so that growth can occur. This aspect has to be one of the guides for future economic policy. A goal must be set to raise the GFCF/GDP rate to higher levels, possibly to the 25/26% that happened in 2007 or 2012, which ensure GDP growth levels (albeit based on oil) of 14% and 8%. Now a new capitalization not only based on oil has to be carried out.

It’s easy to diagnose. Angola lacks capital and needs strong investment. The answers will be the most costly.

3- Increase capital in Angola

What to do to accumulate and increase capital in Angola?

Our answer is divided into two perspectives, the short-term and the medium-term. Let’s focus on the short term, then make a brief reference to the medium term, although it is clear that there is a continuum, as what is done now has repercussions over time.

The executive has already taken some measures, which we have reported in previous reports[6], such as the Private Investment Law (LIP)-Law no. 10/18, of June 26, which no longer requires partnerships with Angolan citizens or companies from Angolan capital and in its article 14, it guarantees that the State respects and protects the property right of private investors; Article 15 establishes that the Angolan State guarantees all private investors access to the Angolan courts for the defense of their interests, being guaranteed due legal process, protection and security. The range of possibilities for transferring dividends were also expanded. Moreover, in administrative terms, it should be noted that in 2018, all requests for the transfer of dividends above five million dollars (4.3 million euros) were granted to foreign companies operating in the country. And, most importantly, since 2020, the capital import from foreign investors who want to invest in the country in companies or projects in the private sector, as well as the export of income associated with these investments, have been exempted from licensing by the Angolan central bank.

However, this is still not enough, and foreign private investment will take a long time, either because a very turbulent electoral period is starting, or because there is a worldwide distraction with Covid-19. In addition, the executive has not yet communicated with all the worldwide amplification, the opening of Angola for business. Even so, it is essential that the executive maintain the political orientation of openness to foreign direct investment.

More needs to be done in the short term to increase investment in Angola and subsequent economic growth. Below is a list of suggestions.

• The initial suggestion is obvious and is based on strengthening public investment. It is essential that the government becomes an inductor of investment and that the capital gains arising from the rise in oil prices and possible apprehensions in the fight against corruption are applied in reproductive investments with short-term results.

The next two suggestions might be more innovative.

Let us address the first of the most unorthodox suggestions. As mentioned, a good part of the savings obtained by Angolans in Angola was remitted abroad, decapitalizing the country. Now we have to reverse this.

• In this sense, the government should, in the first place, sell the dormant shares and assets or in which there is no very relevant strategic interest, which it has abroad. With the result of this sale, it would constitute an investment fund to be invested within Angola. Thus, the first heterodox proposal to increase the capital available in Angola is to sell what there is abroad that belongs to the State (directly or indirectly) and place it in the Angolan economy. Certainly, Sonangol’s position in Millennium BCP should be sold and transformed into investment capital in Angola, and possibly an indirect stake in Galp, if it is not possible to reach a strategic agreement with the Amorim family to better monetize the Angolan position.

• The second suggestion refers to fighting corruption. It is necessary to get out of a certain delay that entered into and boost the capital recovery.

Thus, the government should directly approach those it calls “hornets” and propose a negotiated solution to their situation. Either they deliver the assets that are abroad for investment in Angola, or they will face long prison terms. In relation to these assets, the method outlined above would be followed: Provided market prices were acceptable, everything would be sold and the capital returned to Angola for investment according to a formula agreed between both parties.

This “negotiation” would not be carried out by common means, but by a specialforce to be set up in Angola and would have short deadlines, not judicial deadlines.

There will have to be a radicalization in both directions in the fight against corruption. More effective punishment or forgiveness with repatriation. Unlike what happened in the previous repatriation law, there would be no waiting, but there would be a proactive attitude on the part of the executive.

By way of an illustration, the participation of Isabel dos Santos in NOS, that of General Kopelipa in the BIG bank and in several hotel developments, the apartments that the former figures have in Estoril, etc., could be sold. The result of these sales would return to Angola where it would be invested in terms to be agreed between the State and the former owners.

These listed measures could give some boost to the Angolan economy and thus promote economic growth immediately.

At the medium-term level, the essential thing is that there is no rampant corruption, good communication infrastructures are created, an investor-friendly legal apparatus and fast, non-corrupt courts, an educated workforce (this does not mean having degree courses but the necessary skills) and reasonable taxes. In short, an inviting political and social climate for investment.

https://www.cedesa.pt/wp-content/uploads/2021/09/capital-angola-1.jpg10801920CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2021-09-17 13:52:002021-09-15 13:53:50The question of capital in Angola

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.