The Global Gateway initiative of the European Union and Angola: seize the opportunity now

The European Union (EU) has recently unveiled its Global Gateway project, seen as a European alternative to China’s Belt and Road Initiative (BRI).

The Global Gateway is a €300 billion infrastructure spending plan that aims to boost EU supply chains and trade around the world.

The difference that the EU intends to emphasize compared to the Chinese model of BRI, is that on the European side it will not grant loans, but promote public and private investments, presenting what it considers to be transparent and more favorable financing, especially for developing countries.

The Global Gateway aims to be a more modern version of BRI, focusing on investments in future-oriented and environmentally responsible projects in the digital, healthcare, education, scientific research, renewable energy and other sectors.

It is clear that Africa, and in this, among others, Angola is the logical target of this EU initiative, as it is also where a good part of the Chinese influence through the BRI can be verified. The European Commission does not mention the African market as a priority goal, but it is logical that it should be, as it was the arrival of Chinese financing that most harmed European companies, which often lost market share. And Angola served as a model for the intervention of China in Africa, through the establishment of the so-called “Angolan model”.

The Angolan authorities will have every interest in contacting those responsible for this European Union program to be the first to develop a solid partnership that promotes investments in three fundamental areas for Angola: renewable energies, education and health.

Eventually, the great qualitative leap that one wants to take in Angolan education could be the first bet of this European project. The EU could be the major funder of the qualification of universities and scientific research in Angola, since it is a soft power supporter, and it would be an area in which it has an extremely favorable competitive advantage, easy to the alleged Chinese competition.

On the other hand, an immediate approach by Angola to implement the program will allow the assessment of the seriousness and commitment of the European Union in this program, verifying that it is not a mere advertisement for propaganda purposes, as many claim.

In conclusion, immediate Angolan action is strongly recommended to benefit from the Global Gateway in the area of education.

1- Introduction. Sonangol’s privatization and the oil market

On June 15, 2021, at 16.00, the sale price of Brent oil (which serves as a reference for Angola) was USD 73, 45[1] . A month and a half ago, the price was around USD 66.00, and in recent times there has been a sustained rise in the price, as we had predicted in a previous report[2]. If we notice, when we made this forecast (June 2020), the price of oil was situated at USD 36.6. In practice, in one year the price doubled.

However, the government has put forward more details on Sonangol’s partial privatization. The Minister of Mineral Resources, Oil and Gas, Diamantino Azevedo, repeated[3] his promise to approve the schedule for the sale of 30% of Sonangol’s capital on the stock exchange during the current presidential term, explaining that it will be a staggered process, and that there will be several available tranches: “stocks for Sonangol workers, stocks for Angolans who are interested and for strategic partners who later want to become partners”, a model that we defend in due course[4].

A third element to consider when analyzing Sonangol’s is the energy transition. In the United States and Western Europe, at least, this has become something of a recurring mantra forcing oil companies to modify their strategies so that they are less dependent on oil and contribute to a “green” economy. Sonangol finds itself at this crossroads between the need to recover its old aura, to be privatized, but not just relying on oil.

This report will analyze the possible solutions that the Angolan oil company has and point out some strategic paths.

2-The two determining forces in Sonangol’s strategy

There are two somewhat opposing forces regarding the strategy Sonangol may adopt in the future.

The first force “glues” the company to the oil price and aims to keep it as an oil company. In this view, what Sonangol must do is focus on its “core business” – oil – and then become efficient. Therefore, in this context, Sonangol’s restructuring is focused on achieving profits in the oil business, making profitable investments in the area and increasing as much as possible, at the lowest cost, in oil production. The essential measures taken by the current government with a view to reorganizing the company are in this direction. As Minister Azevedo said: “The first measure we took was to free (Sonangol) from the concessionary function, which could create conflicts of interest. We could not take a company with a concessionary, regulatory and business function to the stock exchange”, and another measure was create an “attractive” company that “encourages investment”, which involved reducing the number of subsidiaries and selling non-nuclear oil companies[5].

The other, somewhat opposite force is the energy transition (the green economy). Here it is argued that Sonangol should not be overly dependent on oil, and that Sonangol should become, as happens with other companies, for example, BP, Aramco or Galp, a global energy company and not an oil company. To this is added the potential of non-oil natural energy resources that the country has, such as sun, water, etc.

3-China, India and the OPEC gap

Contrary to what one might think in a Eurocentric analysis, the answer to Sonangol’s future characterization is not obvious. Much depends on the markets to which Sonangol wanted to allocate its production and on the country’s development needs. If you look at it, the recent rise in the price of oil was essentially “pulled” by China’s renewed oil appetite. According to the Bloomberg[6] financial agency, it was the strong demand for gasoline in China that boosted the need for crude oil. The truth is that China is among the biggest drivers of fluctuations in oil prices and China has been buying oil like there is no tomorrow, as a result, prices have gone up. The question is whether China will continue to drive this rise in the medium term in a way that allows for a sustainable oil strategy in relation to Sonangol.

There are two broad lines to consider in trying to anticipate China’s future behavior. The first is its economic level, while the second is its commitment to the energy transition.

China is not yet at an economic level that corresponds to a rich and developed country. According to data from the World Bank, in 2019, the Chinese GDP per capita is in the order of USD 10,000. For comparison, Portugal, one of the poorest of the rich countries, has a GDP per capita on the same date of USD 23,000 and the United States is at USD 65,000[7]. Countries with GDP per capita identical to the Chinese are Argentina, Lebanon, Bulgaria, Kazakhstan, Turkey or Equatorial Guinea. It is easy to see that China still has a long way to go and will need a lot of energy, especially oil.

China’s oil demand has nearly tripled over the past two decades, accounting on average for a third of global oil demand growth each year. From what we have just exposed, China will continue to lead the demand for oil in the coming decades. However, the pace of the country’s oil consumption will not grow as fast, although it will continue to grow. Over the past two decades, China’s oil consumption has grown by more than 9 million barrels per day (mb / d) from 4.7 mb / d in 2000 to 14.1 mb / d in 2019. China’s oil use should continue to grow, albeit at a slower pace, as China is also investing heavily in renewable energy.

China is the world leader in electricity production from renewable energy sources, with more than twice the generation of the second country, the United States. At the end of 2019, the country had a total capacity of 790 GW of renewable energy, mainly hydroelectric, solar and wind power. China’s renewable energy sector is growing faster than that of fossil fuels, as is its nuclear power capacity. China has pledged to achieve carbon neutrality before 2060 and peak emissions before 2030. By 2030, China aims to reduce carbon dioxide emissions per unit of GDP by more than 65% from the level of 2005, increase the share of non-fossil energy in primary energy use to about 25 percent, and bring the total installed capacity of wind and solar electricity to over 1200 GW. Furthermore, China sees renewable energies as a source of energy security and not just a means of reducing carbon emissions[8][9].

In India, another of the world’s great countries in a process of growth, the situation is as follows: trade relations between Angola and India amount to US$4 billion, of which US$3.7 million correspond to exports from Angola to the Asian country, being 90% related to oil. Angola is currently the third most important African exporter to India, when in 2005 it was not relevant. In 2017, the Ambassador of India issued a statement in which he highlighted: “Trade between Angola and India increased by 100% in 2017.” The thing to remember is that India is becoming a significant partner of Angola through its oil needs.

In terms of GDP per capita, India in 2019 was around USD 2000.00. It is easy to see that the growth that India expects is enormous, even if it does not have China’s ambitions of world leadership, just to reach its current level, it has to multiply its GDP by five. Obviously, this implies a growing need for oil. India was the world’s third largest crude oil importer in 2018, and has an estimated oil import dependency of 82%. India’s economic growth is closely related to its demand for energy, so the need for oil and gas is expected to grow even further, making the sector very investment-friendly. At the same time, India is one of the countries with a large production of energy from renewable sources. As of November 27, 2020, 38% of India’s installed electricity generation capacity came from renewable sources. In the Paris Agreement, India committed to a target of achieving 40% of its total electricity generation from non-fossil fuel sources by 2030. The country is aiming for an even more ambitious target of 57% of total electricity capacity from renewable sources by 2027.

Official data indicate that Angola’s oil production reached, in May 2021, only 34 million 887 thousand 890 barrels, less about one million compared to April. In that month, a daily average of one million 125 thousand 416 barrels of oil was obtained, when the forecast was one million 184 thousand 813. This means that Angola is below the target set by the Organization of Petroleum Exporting Countries (OPEC). ), which was 1 million 283 thousand barrels per day, in May, with subsequent increases.

4- Conclusion: Sonangol’s challenges

Considering all of the above, it is evident, first of all, that there is a large margin for Sonangol to continue to focus on oil, either because not even the quotas defined by OPEC for Angola are met, ie, Angola is producing less than it should in a tight market situation, either because the large potential oil futures markets such as China and India will need plentiful oil shipments.

To that extent, Sonangol should not make the mistake – as some oil companies are doing – of underestimating the potential for growth in the oil market. In the Western world with mature economies, the demand for oil may not feel as strong as in the past, but in fast-growing economies, more oil will be needed, albeit often not as exponentially as before.

There is space and market for Sonangol, as an oil company, to grow. Therefore, Sonangol’s ongoing strategic structuring should focus on producing more oil more efficiently, both in terms of costs and in terms of the environment.

However, this model focused on oil efficiency has to be matched with the enormous potential that is opening up in renewable energies and the company has to take advantage of energy synergies, as many of its counterparts are doing and also China and India.

At the present time, when the intention is to privatize Sonangol from a global perspective, it seems sensible to commit Sonangol to tasks in the area of renewable energies. In fact, to be an attractive company for the international stock market, Sonangol must present itself as adopting the latest trends in oil companies, i.e., also following the needs of the energy transition.

Not abandoning or belittling oil, Sonangol must boldly explore the combined possibilities brought by renewable energies.

This exploration of renewable energies by Sonangol should not start from scratch, but rather seek some sustainability and economies of scale. One hypothesis, which we have already touched upon in a previous report[10], would be a strategic partnership with Galp for this purpose. As is known, Galp accelerated its energy transition process.

As this hypothesis was not adopted, Sonangol should review the rationality of its permanence at Galp. In fact, at this moment, the Angolan position in Galp is “sandwiched” between Isabel dos Santos and the Amorim family, corresponding to a mere financial investment. This doesn’t make much sense anymore. Either Galp becomes a strategic partner for Sonangol’s energy transition, or a position review becomes required.

The alternative would be for Sonangol to acquire a company that is minimally established in the field and develop its activities based on this new platform. At this time, partnerships have already been announced with ENI and TOTAL to develop projects in renewable energy that will be operational in 2022. Perhaps a strategic focus in this area is more interesting, which would translate into an internal commitment by Sonangol and, as mentioned above, it would go through the purchase or merger with a company operating in the renewable energy sector, to provide initial support for Sonangol.

In short, Sonangol must become a bi-focused company: on oil and renewable energies.

[9] Deng, Haifeng and Farah, Paolo Davide and Wang, Anna, China’s Role and Contribution in the Global Governance of Climate Change: Institutional Adjustments for Carbon Tax Introduction, Collection and Management in China (24 November 2015). Journal of World Energy Law and Business, Oxford University Press, Volume 8, Issue 6, December 2015.

https://www.cedesa.pt/wp-content/uploads/2021/06/sonangol-energetica.jpg6941024CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2021-06-28 10:25:002021-06-28 10:25:15Sonangol. Oil or energy company?

0-Introduction. Failure to take advantage of synergies between Sonangol and Galp

It was a recent article in the Jornal de Negócios, by its director Celso Filipe, which drew attention to the lack of synergies between Sonangol and Galp[1] and which serves as a starting point for this note on the topic.

Sonangol is the Angolan oil company and for many years it has been the real core of the country’s economy. In fact, it still is, despite the government’s diversification policy. In technical terms, the group consists of Sonangol E.P. (a public company) and a myriad of subsidiaries[2]. Galp is a Portuguese group also linked to oil, which includes several companies such as Petrogal, Galp Energia etc[3]. Obviously, Sonangol is the giant of the Angolan economy, while Galp is one of the largest companies in Portugal, alongside EDP.

The interesting thing is that since 2005, Sonangol has been a shareholder of Galp, although such participation is not assumed directly, but through a company of the Amorim family. It is known that, in an initial phase, this participation was publicly attributed to Sonangol, but then the daughter of President José Eduardo dos Santos, Isabel dos Santos, emerged as the holder of interests in the same participation, and there was sometimes factual confusion between what belonged to Isabel dos Santos and Sonangol. Today there is a dispute between the position of Sonangol and that of Isabel dos Santos, which led to the investigation of the latter in the Netherlands, where the vehicle company that it uses to control its position is headquartered[4].

Therefore, we have more than 15 years of indirect participation by Sonangol in Galp. The curious thing is that during that time, Sonangol and Galp never really sought to create synergies between the two companies. Sonangol’s participation was limited to being seen as a financial participation. Sonangol invested money and received dividends from that money. Nothing else. As Celso Filipe points out, in the aforementioned article: “Sonangol never sought to create industrial synergies with Galp, which could benefit the activity downstream and upstream of production and even improve its profitability.”

• The approach of Sonangol’s partial privatization requires that its holdings be valued to the maximum and the exploitation of synergies is done in the most efficient way so that the company obtains the best price for the sale of part of its shares.

• In addition, the current Angolan economic crisis requires an additional effort by its largest company to increase profitability.

These two reasons make it imperative to revisit the topic of Sonangol’s participation in Galp in order to see what is the best way to maximize its usefulness.

With this objective in mind, we will start by defining Sonangol’s current position at Galp, and understand its formal justification, suggesting a change, then we will try to find explanations for the purely financial strategic position that the Angolan company adopted in its Portuguese counterpart and finally, we will explore the various options for the future.

1- Sonangol’s position at Galp

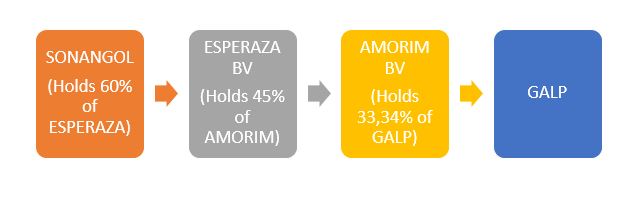

What results from Galp’s public corporate documents is that Sonangol does not hold any direct stake in the Portuguese oil company. Galp’s largest shareholder is Amorim Energia, BV with 33.34% of the capital, followed by Parpublica (which holds the Portuguese State’s shareholdings) with 7.48% of the capital and several investment management companies such as Massachusetts Financial Services Company, T. Rowe Price Group, Inc. and BlackRock, Inc. with about 5% each. Then there is Banco New York Mellon and Canada’s Black Creek Investment Management with around 2%[5]. This list of reference shareholders includes a company based in the Netherlands with the name Amorim, the Portuguese State and several American financial institutions. Sonangol does not appear.

In fact, Sonangol’s position is associated with the Dutch company Amorim. Sonangol holds the majority of the capital of a company called Esperaza Holding BV (also based in the Netherlands). In turn, Esperaza participates with 45% of Amorim.

This means that Sonangol has a minority position in Galp’s majority company. If Sonangol represents 45% of Amorim’s capital, it is clear that the Amorim family owns the other 55%. In turn, it seems that even in Esperaza Sonangol’s position is not total, since it shares it with Isabel dos Santos, with a dispute between them that it will not be cured here, since it does not affect the assumption that Sonangol controls Esperaza.

Fig. No. 1- Sonangol’s indirect participation in Galp

In a way, Sonangol’s position appears “sandwiched” between the Amorim and Isabel dos Santos, effectively lacking strategic room for maneuver and not having a decisive role at Galp, since it is always mediated by the Amorim.

Is the doubt that persists one see the reason why Sonangol accepted to participate in Galp in a dependent and submissive position to the Amorim? Was it a political demand from the Socrates government at the time, to avoid an overpowering onslaught by Angola? Was there shyness or ineptitude in negotiations on the part of Angola? Or was it a strategic formulation of Isabel dos Santos to appear unseen? We have no elements to justify this indirect choice.

• What can be said today is that Sonangol’s indirect position is detrimental to the appreciation of its shares as it is always dependent on a third party, in this case the Amorim, and does not have direct access to the company. This does not give value to the position or give it room for strategic maneuver.

What can be seen is that Sonangol’s stance enhances the Amorim’s leading role as they, with a mere 18.33% of the company, control 33,34%. We do not know whether Sonangol receives (or has received) any “prize” from the Amorim for this contribution or if there is any shareholder pact.

If there is no “prize” or shareholder agreement that benefits Sonangol, the truth is that, from Sonangol’s point of view, what will make the most sense is to split its position from Amorim and make its participation in Galp independent. This, as mentioned above, will give financial value to the participation as it becomes direct, and will give the Angolan company more strategic room for maneuver. This element is even more relevant at a time when it seems that strategic differences between the Amorim and the Galp’s CEO, Carlos Gomes da Silva, led to his hasty departure from the helm of the company. We don’t acknowledge the role Sonangol played in this divergence and its resolution, if any.

2- Possible reasons for the “passivity” of Sonangol’s position in Galp

As we have been saying, Sonangol’s role in Galp has been passive, essentially limiting itself to receiving dividends and not looking for any strategic synergy. The question that arises is why such a large and important participation, which several Sonangol CEOs consider in their public speeches as strategic, ended up being nothing more than a financial investment?

The first reason to justify such behavior is of a formal nature. Since Sonangol is not a direct Galp shareholder, it did not have the necessary means of influence to propose and create any synergy. This justification seems to us too formalistic and does not necessarily correspond to reality. However, it should be noted that in 2020, regarding several controversies involving Isabel dos Santos, Galp’s CEO, Carlos Gomes da Silva, was not afraid to affirm that “Isabel dos Santos is not a direct or reference shareholder [ of Galp] ”, adding“ The long-term reference shareholder is Amorim Energia, which is controlled by the Amorim family [6]”. Although the context of these statements is perceived, they still represent an effective disregard for the Angolan position, but that basically corresponds to the truth.

A second reason for Sonangol’s passivity is linked to the preponderant role that Isabel dos Santos played in Galp’s Angolan participation. The businesswoman only worked for a short time in Sonangol (2016-2017), in the remaining time, that is, between 2005 and at least until the emergence of several controversies in 2019/2020, her position was that of a private entrepreneur. in constant investment process. Isabel dos Santos did not stop in the extension of her “economic empire”, making purchase after purchase, investment after investment. In Angola, in addition to the initial investment in Unitel (a leading telecommunications company), Isabel dos Santos, as of 2008, enters several sectors such as distribution, banking, and hospitality. In banking, in addition to participation in BFA, the foundation of Banco BIC, in the distribution sector, launched Candando. In Portugal, she participated in BPI, bought BPN, took a stake in what is today NOS, in addition to Galp. She also bought vast real estate.

There is a pattern in Isabel dos Santos’ business activity, that of the investment cascade, using loans or dividends from one company to acquire others, not worrying, at this stage, in strategically integrating her business conglomerate. Now, the behavior observed in the construction of Isabel dos Santos’ “empire” and the possible political control that she assumed for some years over the Angolan participation in Galp, may have implied an option for receiving dividends as a priority. In fact, Isabel dos Santos would need Galp’s dividends to cover her expenses and, without having other relevant oil interests, there would be no focus on building synergies.

This is a working hypothesis that, of course, needs to be confirmed as the documentation on the involvement of Isabel dos Santos in the control of the Angolan position at Galp, between 2006 and 2016, is made public.

• However, what appears to be that the determining interest in this Angolan participation in Galp in the referred period was that of Isabel dos Santos and her main concern was to obtain funds for investment in its expansion and maintenance of its business conglomerate.

Obviously, this hypothesis does not explain the apathy observed after Isabel dos Santos left. Since 2018, there have been no special moves by Sonangol vis-à-vis Galp. At this stage, this inertia can be justified by the strategic uncertainty that has plagued Sonangol and also its participation in Galp.

In one way or another, this is the imperative time to take a rational stand on this participation.

3- Sonangol’s several options vis-à-vis Galp

When the Angolan oil company is in the process of restructuring and intends to privatize part of the capital, it is essential to consider what it will do in relation to its participation in Galp.

There are several hypotheses for action. To better analyze them and discover the most appropriate course, it is pertinent to approach the strategies that each of the companies is following, since both are in a moment of reconfiguration.

Sonangol’s strategy

As for Sonangol, the strategy followed is based on several vectors, of which we highlight[7]:

-Like several of its counterparts, ARAMCO or BP, the oil company wants to become greener. It is also intended to permanently move away from the image of corruption. The plan for the next seven years, focuses on renewable energies and the relaunch of exploration and production in several oil blocks. In particular, Sonangol intends to:

– Increase the capacity of operated production of crude oil, with a target of not less than 10% of national production, instead of the current 2%.

– Invest in several oil blocks in order to increase net rights, with the relaunch of exploration and production in several oil blocks expected this year (blocks 3/05, 3 / 05A, block 5/06, Kon 4, as well as the cooperation, together with Total, of blocks 20 and 21, three years after the first oil).

– Optimize and modernize the Luanda refinery and ensure an increase in refining capacity, with investment in new refineries, in order to reverse the fuel import situation.

– Increase the capacity to distribute LPG [liquefied petroleum gas], monetize LNG [liquefied natural gas] and invest in renewable energy projects.

– Consolidate the company’s position as a reference player in the shipping segment in the region.

– Reinforce the position of trading crude oil and refined products in the international market, thus leveraging additional sources of revenue collection in foreign currencies.

-Optimize the retail network, aiming to consolidate the position of largest distributor of liquid hydrocarbons in the national market, in an environment that is increasingly liberalized, as well as relaunching the distribution and commercialization activity in other countries in the region, of which we have already the re-entry process is underway in the Democratic Republic of Congo.

Galp’s strategy

Galp is also in a strategic transition phase[8]. Decarbonisation has now become a priority, already manifested in the decision to close the Matosinhos refinery and the Sines Thermoelectric Power Plant. In fact Joana Petiz at Dinheiro Vivo[9], says that it was the Amorim’s commitment to accelerating the energy transition that led to the shortening of Carlos Gomes da Silva’s mandate and the appointment of Andrew Brown. Brown will have a mandate to bring about an intense change in Galp’s business, which is already advanced in its energy transition. In reality, Galp is the largest producer of solar energy in the Iberian Peninsula and invests in lithium, having acquired 10% in the company to which the lithium exploration in Portugal, Savannah Resources, was handed over.

However, despite these movements, oil is the company’s main source of revenue, with a special emphasis on holdings in Brazil, which make a substantial contribution to the company’s sustainability. Apparently, this will be where the financing for new projects “like gas in Mozambique – an intermediate step in the transition to cleaner energy – will come from, as well as the new bets from the oil company, including the exploration of lithium in Portugal[10]”.

Brief comparison between Sonangol and Galp

In 2019, according to the Reports and Accounts, Sonangol obtained total revenues in the order of US $ 10 billion, and an EBITDA of 5 billion. In turn, Galp achieved revenues of more than 19 billion dollars and an EBITDA of just over 2.5 billion dollars. Both companies affirm they are committed to an energy transition, this bet being more visible in Galp, but in terms of revenues both are dependent on oil.

Sonangol can choose one of the following options or a combination of several in relation to Galp:

1-Sale of participation;

2-Reinforcement of participation;

3-Maintenance of the strategy as a financial investor;

4-Synergy in the energy transition;

5-Industrial and commercial synergies.

Let’s look at each hypothesis.

Sale of participation

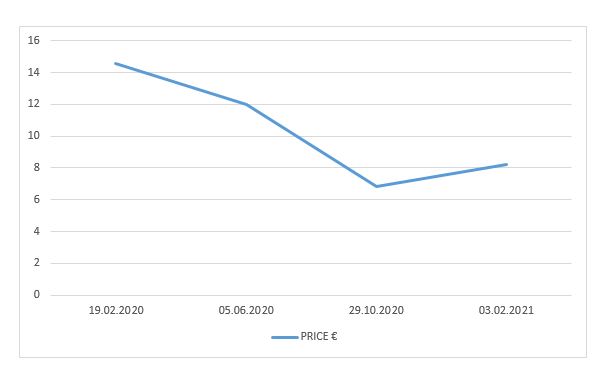

It is clear that lately the price of Galp’s shares has been discouraging. If you notice, throughout 2020 the bonds were losing value, even in October they were below € 7.00. It should be noted that this happened after the start of Covid-19, as in February 2020, the securities were being traded at around € 14.00. At this point, stock trading is slightly above € 8.00. The reality is that it is only after the fight against the Covid-19 pandemic is over that it will be possible to assess Galp’s trend market value.

Consequently, there is nothing to advise a low sale at this time.

Strengthening participation

Alternatively, Sonangol, given the low price of Galp shares, could consider strengthening its position in Galp. This would be justified as long as Sonangol had funds available for such an acquisition and saw an additional strategic interest that would lead it to have a more influential position in the company.

Maintaining the strategy as a financial investor

This has been Sonangol’s position for the past 15 years and, of course, it has borne fruit, being able to choose to maintain its posture. If we analyze Galp’s ROE (return on equity) since 2011, we see different numbers. In 2011, we had a robust number in the order of 14, 73%. In 2013, the number was around 2.86%. 2015, presented 1.91%, 2016, 2.86%. ROE in 2019 was at 6.75%, and recently in September it was negative, -8.19%[11]. This instability is important for Sonangol to evaluate its participation in Galp as it allows the Portuguese company to be qualified in terms of risk and consequent expected profitability.

This means that Sonangol will be able to convince itself that there are other more satisfactory alternatives for investing its capital and that they do not bring such large fluctuations, preferring to disinvest. We believe that if this is Sonangol’s option, this will mean that sooner than later, when the price is good, it will eventually sell the position.

Synergy in the energy transition

This is the option that seems most promising to us. With Galp already embarking on an advanced energy transition program and Sonangol wanting to take more firm steps in this direction, as indeed a good part of the large oil companies is already doing, the alliance or cooperation between Sonangol and Galp in this area, namely in solar energy, where Galp, as mentioned, has a prominent position in the Iberian Peninsula, and Sonangol comes from a country with great potential, there is a great possibility for joint action. In this sense, the possibility of creating and implementing common and ambitious projects in the area of energy transition is envisaged, providing Sonangol with the Know-How it does not have yet, and giving Galp a broad market for the development of its already designed strategy.

Industrial and commercial synergies

Obviously, the possibility of industrial and commercial synergies is immense. From oil refining at Galp’s refineries, to derivatives and shipping, in addition to using Galp’s accumulated experience in pre-salt prospecting in Brazil to open up new horizons in Angola, there are a myriad of possibilities that could be explored[12].

4. Conclusions

• The first conclusion reached through this short analysis is the need to legally reformulate the participation of Galp’s Sonangol. This should appear independently and directly in the shareholder body of the Portuguese company.

• The second conclusion is that there is a wide map of possible synergies between Sonangol and Galp, and it is strongly advised to develop them in the areas of energy transition, namely in solar energy.

I-Introduction. The revival of interest in industrialization

The industrialization of Angola has become one of the objectives of the current government under the leadership of the President of the Republic João Lourenço. In fact, either at the International Summit on Sustainable Development “The Future of Africa” held in Abu Dhabi in 2019, or at the third edition of the Global Summit on Manufacturing and Industrialization, promoted by the United Nations Industrial Development Organization (UNIDO) in 2020, Lourenço always emphasized that industrialization was a pressing need with a view to creating wealth and well-being for citizens and employment as the main source for all opportunities.

In fact, since Angola does not have staff and skills with sufficient critical mass in terms of services, and having recently seen the strategic weaknesses of economies that are too much based on services, it is normal for any economic start-up in the country to be also based on industry.

The industrialization of Angola must be thought based on three assumptions.

The first is that it will be based on strong agriculture. It is not a question of replacing agriculture with industry, but simultaneously developing agriculture and livestock as the basis for a renewed industrial start-up.

The second assumption is that what is called industrialization today will be different from what was considered at the beginning of the 20th century when such a movement was linked to the so-called heavy industries: steel, cement, etc. Furthermore, industrialization is not just manufacturing, but a set of transformative processes.

Finally, the vectors of industrialization in Angola will have to be linked to specific factors that bring added value to the economy or where it has competitive advantages. Therefore, it is not a matter of making mere copies of industrial models, but of realizing where Angola has benefits in industrializing.

II- Industry in the Angolan economy

As Nuno Valério and Maria Paula Fontoura write “in 1975, [when] Angola became an independent state, (…) the economy was prosperous, whether due to the existence of considerable exports of agricultural products (coffee, cotton, sugar, sisal) and others from plantations; corn from traditional farms) and minerals (diamonds, iron and oil) and even services (particularly through transit to Shaba, formerly Catanga, via the Benguela railway), either due to the beginning of an industrialization process.[1]“

The Angolan industrial start-up began in the 1960s, still under colonial rule. In fact, from that time, framed in the general liberalization and pro-European measures that Portugal took, in the creation of a Portuguese free trade zone and in the expansion of the internal market through the troops and families displaced with the overseas war “between 1960 and 1970, the gross value of manufacturing industry production grew at an average annual rate of 17.8% and GDP 10% in nominal terms.[2] “

In fact, on the eve of independence (1973) the Angolan industry (excluding civil construction) represented 41% of GDP. The important industries were the food industry, with 36% of the gross value of production in the manufacturing sector; followed by the textile industry, with 32%, beverages, with 11%, chemistry, non-metallic mineral products and tobacco, with 5%, petroleum derivatives and metallic products, with 4%, pulp, paper and derivatives, with 3%.[3]

Fig. 1- The main industries in Angola in 1973 (% gross value of production in the manufacturing sector):

Food

36%

Textile

32%

Beverages

11%

Chemistry, non-metallic mineral products and tobacco

5%

Petroleum products and metal products

4%

Pulp, paper and derivatives

3%

Oil

30%

Coffee

27%

Diamonds

10%

Source: Nuno Valério and Maria Paula Fontoura, op.cit.

It should be noted, however, that by this time, the “evil” of the Angolan economy was already present, i.e., the excessive dependence on raw materials for export. In reality, the manufacturing industry only contributed to around 20% of Angolan exports, with the main products exported in 1973 being: oil (30%), coffee (27%), diamonds (10%).

This liberalizing start-up in the Angolan industry was subject to some criticism, and in the 1970s, the government of Lisbon began to impose a protectionist perspective on Angolan industrial development. This did not affect the healthy growth of the industry. In fact, as noted by Nuno Valério and Maria Paula Fontoura: “the manufacturing industry’s VBP grew at an average annual rate of 21% between 1970 and 1973.[4]”

It is known that the situation of prosperity was interrupted by the civil war and it was only after 2002 that there was a strong revival of the economy. However, this restart was based on crude oil exploration and not on any sustained industrialization process. Even when it comes to oil, there was no concern about integrating it into an industrialization process and making Angola a country that bet on the transformation of its raw material instead of exporting it raw. This meant investing in refining, in petrochemicals, in the production of fertilizers, which did not happen[5].

Arriving in the second decade of the 21st century, the situation of the economy becomes worrying when oil exploration is no longer satisfactory due to the drop in its price. In this context, we start talking about the diversification of the economy and looking at the industry, but the scenario is not encouraging in terms of the strength of the industry within the scope of the Angolan Gross Domestic Product (GDP), so it is essential to mix and actively promote a project to launch industrial activity.

The most recent data referring to the weight of the manufacturing industry (except crude oil refining), dated from the second quarter of 2020, point to a 4.8% contribution to GDP. This contribution was 3.69% in 2002, and 4% in 2017 and 2018. On the same date, the year-on-year change in the manufacturing industry had been negative by 4%. The Gross Added Value was also negligible[6].

Fig. 2 – Weight of the manufacturing industry in Angola (2nd quarter of 2020)

Contribution to GDP (%)

4,8

Year-on-year change (%)

-4

Source:Banco Nacional de Angola. Contas Nacionais (bna.ao)

III. Industry relaunch project in Angola

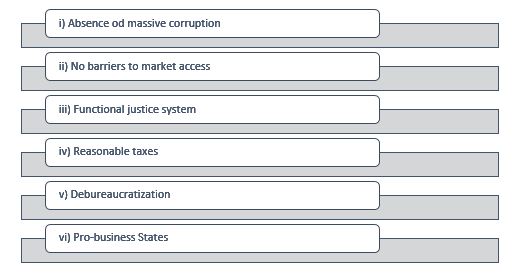

Any project to relaunch the industry should start by having the right context. This context is a free economy with a social climate conducive to investment. The social climate is based on six necessary assumptions:

i) Absence of massive corruption. Corruption distorts the rules of economic competition and prevents free access to markets, fundamental conditions for industrial development;

ii) No barriers to accessing markets. Entrepreneurs should be free to obtain their production factors and settle in to produce;

iii) Functional Justice System. The justice system should not be seen as corrupt, slow and incompetent, but as applying the rules, punishing those who do not fulfill contracts and having legal and normal forms of debt collection;

iv) Reasonable taxes. Taxes should tend to be moderate and not stifle productive activity;

v) Less red tape. Public administration should be pro-business and not create administrative bureaucratic obstacles to the installation and operation of companies.

vi) Pro-business state. The State should have a fomenting and proactive role in industrialization, pointing and framing paths, building infrastructures, qualifying the workforce and establishing partnerships.

Fig. No. 3- Context for the industrial relaunch

In view of the necessary context, the important thing is to point out the axes through which the efforts of industrial growth should be channeled.

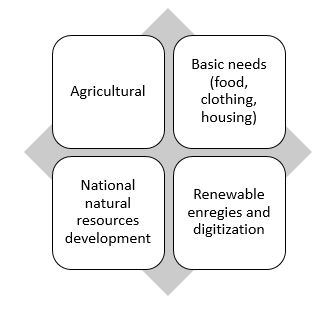

We see four axes of industrialization in Angola. These axes are chosen taking into account the economic history of Angola, its wealth and potential, the experiences of global industrialization and the possible trends of the markets in the coming decades.

Thus, we propose an industrial development according to the following points that can be interconnected or complementary:

1-Agriculture;

2-Basic needs industries;

3-Industries of development of natural wealth;

4-Future: renewable energies and digitalization.

Fig. N. º4 – Axes of the Industrial Relaunch Project

1-Agriculture

The agricultural industry represents the natural development of the Angolan potential already in operation and which was the subject of our previous report[7].

This a small example to gauge the potential. Recently, it was reported that Angola has been the main banana producer in Africa for six consecutive years. According to the Food and Agriculture Organization of the United Nations (FAO) Angola is the largest African banana producer and the seventh in the world with an offer of 4.4 million tons[8].

It will be elementary that it will be easy and possible to create an industrial line based on bananas: fruit juices (beverage industry), medicinal exploitation of banana / potassium (chemical / pharmaceutical industry), etc., are some of the possibilities in the refrigeration or pharmaceutical industry regarding banana.

The same type of reasoning can be applied to products and natural resources that Angola has or exploits in abundance. By internally transforming its natural resources and products, the country adds value to them, ceasing to be dependent on the mere evolution of the world price of raw materials.

2-Basic needs industries

Basic needs are understood as food, clothing and housing. This industrial axis represents an industry in which no specific sophistication is required and it is possible to make an import substitution without special losses of competitiveness, in addition to making it possible to create export markets in similar countries. In addition, Angola has already had a powerful industry in the area of food, beverages and textiles. With a market of 30 million people that can easily be extended to many millions more with the developments of the Southern African Community (SADC) and the African Free Trade Area, Angola has enough potential demand for essential products: clothing , shoes, houses (obviously), basic food products from yoghurts to beers. There is no reason not to create its own industry with its own brands, in many cases imitating what has been done successfully in countries in these areas such as Bangladesh and Vietnam.

3-Natural wealth development industries

Another industrial axis, which basically replicates in a more comprehensive way what was mentioned in the first axis, focuses on national wealth, now not agricultural, but the rest. It has all the logic and economic rationality to use and transform what exists in Angola, adding value to it instead of exporting in gross terms, allowing capital gains to be appropriated by others. Here we have the most obvious example, oil. What makes sense is to develop the industry downstream from oil: refining, petrochemicals, plastics, fertilizers, etc. As the United Nations expert Carlos Lopes said, “The question is clear: it is not turning your back on wealth, such as oil, but integrating it in the transformation and making Angola a country that invests in the transformation of its raw material. instead of exporting it gross. This means investing, in addition to refining, petrochemicals, fertilizer production, etc. [9]“

4-Future: renewable and digital energies

The final axis is connected to renewable energies and the digital transition. Today, it is common ground that there is a demand for the replacement of oil by clean and renewable energies. In the United Kingdom, the goal was announced in 10 years to end the circulation of gasoline or diesel cars. Electricity generated by renewable energies seems to be the future. Large oil companies like BP or Aramco are transforming or embracing these areas. Now Angola has excellent natural conditions for this investment in renewable energies. Solar energy from the start. An industrial niche around solar energy and electricity production would be a bet to consider very seriously.

From the point of view of the digital transition, Angola will be able to make an important qualitative leap using digital techniques for the development of applications for the massification of basic and secondary education, for basic health and in the financial area. Here we have an industry of digital applications for teaching, health and banking that could be developed in Angola by Angolans, immediately combining a synergy between betting on health and education alongside digital industrialization.

IV-Coordination of the industrial relaunch project

On the part of the State, there must be a commitment to this project that will essentially be up to the private sector.

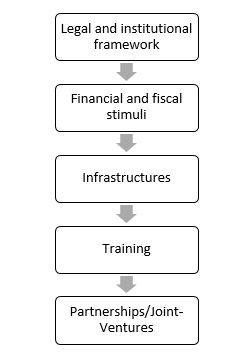

However, the State must create the legal and institutional framework, prepare financial and fiscal incentives, build infrastructure, promote the training of agents capable of change and establish partnerships.

For the task of coordinating the activities of the State with a view to industrial relaunch, there should be a coordinator directly dependent on the President of the Republic: a Czar of the Industrial Project.

Fig. No. 5 – State’s role in relaunching the industry

[1]Nuno Valério e Maria Paula Fontoura, A evolução económica de Angola durante o segundo período colonial — uma tentativa de síntese, Análise Social, Quarta Série, Vol. 29, No. 129 (1994), pp. 1193-1208, p.1193.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.