There is an undeniable fact. Angolan elections scheduled for the 24th of August are the most disputed of the post-civil war (2002)[1]. Never has been a discussion so renamed and the intensity of the arguments and uncertainty so debated.

Despite some tension and sometimes incendiary rhetoric, this electoral context represents a significant advance of the democratic struggle, which is expected not to go beyond from other forms of struggle.

One of the innovative aspects that has arisen in these elections is the plurality of polls. As much as memory and files allow to determine, the existence of polls was not a usual fact in the previous Angolan elections.

In fact, in 2017, only one reference came up to a supposed poll made by the Brazilian company “Sensus, Pesquisa e Consultoria”. The existence of this poll was never confirmed, but at the time sources revealed that this entity would have learned that the MPLA would gain only 38 percent of the votes. UNITA would obtain 32 percent of voting intentions, while the Casa-CE would appear very close to Unita, with 26 percent. From this it would result that the majority in the National Assembly would be the opposition[2].

What is certain is that this poll has never been confirmed and the final results were quite different. As is well known, the MPLA had 61.05%, while Unita and Casa-CE reached 26.72% and 9.49% of the votes, far from what the supposed poll stated.

2-The polls in the 2022 elections

If the 2017 elections revolved around a ghost survey that had nothing to do with the final reality in 2022, unlocked public polls appear, although fought by the forces that do not like the results.

It is about these polls and the possibility of predicting an end result based on them that this analysis is leaning.

We follow the identification of polls by a Portuguese Cable Channel[3] and consider five published polls. These are:

All of these entities have their site and present the results publicly.

We do not ignore that there are several controversies around some of these entities, however, we chose to rely on the technical records of each of the polls and the good faith of the interveners. Let’s look at the message and not “kill the messenger.”

In fact, with the exception of Afrobarometer, all other entities are reasonably recent and seem to be dedicated to present Angolan elections, containing professionals from other companies or organizations. This is a sign of democratic liveliness and therefore does not deserve criticism. What is certain is that these entities after the first essay that are these elections in Angola will be perfecting to contribute to the democratic discourse in Angola.

Looking at the data sheets of each of the polls and results we will make a measure of the results following two criteria, the reliability of the method and the normal Gaussian distribution.

First, the type of inquiry performed. From the technical records and affirmations of those responsible we conclude that Mudei and Afrobarometer do random street surveys based on premises that specify in their methodology pages. In turn, Angopolls and PoBBrasil perform telephone inquiries according to a random computed selection. Angobarometro, on the other hand, performs online polls.

We understand that online surveys are not reliable because they benefit from a “neighborhood effect”, that is, there is a tendency to call friends and people who think the same way to visit the site. Therefore, if a site is taken as closer to UNITA will call more people from UNITA, having a bias in its favor, the same happening if the site is MPLA. To this extent, we believe that online polls demonstrate a party’s ability to mobilize, but not the voting intentions of a random sample of the population.

We thus remove the AngoBarometro from this appreciation.

Regarding the remaining four, we proceed to a Gaussian distribution by eliminating the extremes and maintaining the standard-normal distribution. To this extent we will not consider the POBBrasil Survey that gives the MPLA an extreme victory, and also Mudei that gives UNITA an extreme victory.

3-Standard-polls

There are two polls that seem to us the most standardized: Afrobarometer and Angopolls.

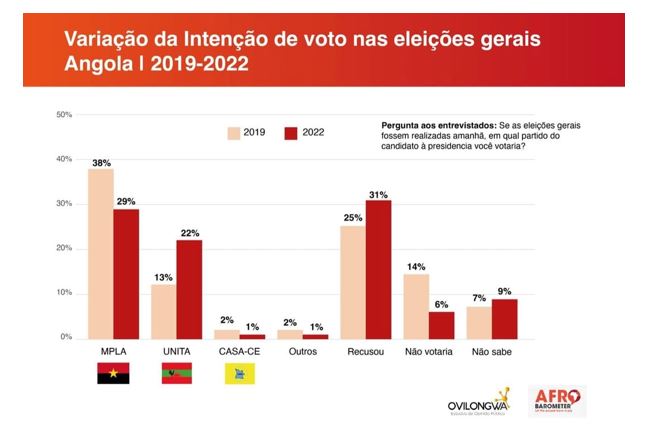

Afrobarometer’s technical record reveals that: “The Afrobarometer team in Angola, led by Ovilongwa – Public Opinion Studies, interviewed 1,200 adult Angolans, between February 9 and March 8, 2022. A sample of this size produces national results with one Error margin of +/- 3 percentage points and a confidence level of 95%. The previous research in Angola was conducted in 2019”.

The results achieved are presented in the table below:

Table No. 1- Afrobarometer results

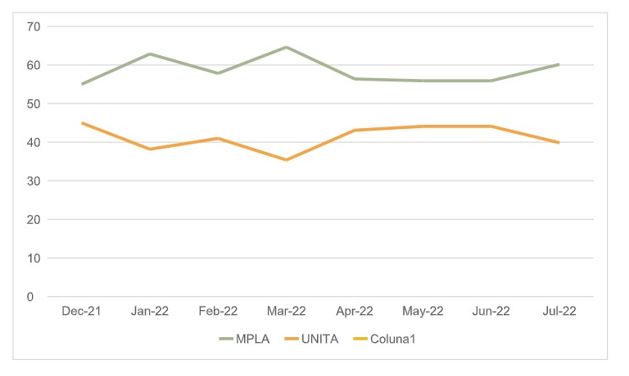

Angopolls has conducted several inquiries since December 2021. We will focus on the last of the published sequence, “VII-General Elections poll. July 2022”. Its datasheet states that: “The poll was made by telephone. 5040 valid inquiries were obtained, 21.03% of respondents were female.”

The results obtained were as follows:

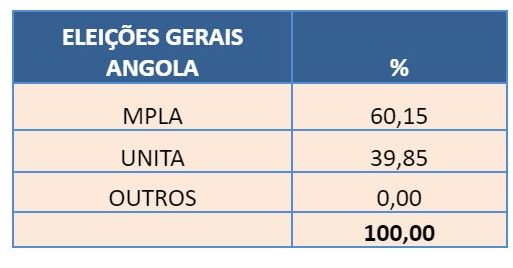

Table No. 2: Angopolls results

¹ Not accounting for undecided and abstentions.

The Angopolls page also contains a curious chart with the presentation of the evolution of results over the several months:

Table No. 3- Voting Trends According to Angopolls

In a first analysis, it would seem that Afrobarometer and Angopolls polls give different results. In fact, the presentation of Afrobarometer attributes 29% to the MPLA and 22% to UNITA, while Angopolls refers to a percentage of 60.15% to the MPLA and 39, 85% for Unita. It appears to be a very large difference between the two polls.

However, a thinner analysis reveals that this is not the case.

In the end, in essence, the two entities came to very similar results: MPLA wins and UNITA reinforces its result, and even in percentages the difference is not very significant. The explanation for the apparent difference that does not exist is in the methods of presentation of the results and not in the results themselves.

If we notice Angopolls withdraws from their presentation the non-response (abstentionists, undecided on whether they would vote, etc.), while Afrobarometer does not do so. Note that they keep 46% – don’t know, don’t vote, refused to answer.

Now if we apply the same criterion for both polls, that is, removing the do not know, don’t vote, refused to answer, the so -called non-responders we will have a significant approximation between the two polls that mirror the table below:

Table No. 4: Comparative results Afrobarometer and Angopolls Following the same method of presentation

It is evident that another method for considering non-response is to impute them according to historical criteria (that is, considering the meaning of voting in previous elections) to political forces or then you can go into several speculative exercises.

Conclusions

What results from this analysis is that normal predictability points to a victory of MPLA in a percentage that oscillates between 54% and 61% and a substantial reinforcement of UNITA to 40%, with a sharp decrease of other political forces, what is called in political science a bipolarization.

It should be noted, however, that giving the percentage of non-respondents, these numbers are not fixed and definitive. They are a photograph at a given moment, but everything can change.

Therefore, polls give some indications, mark trends, but do not give certainty. As mentioned at the beginning of this work, this is an area of democracy that only now begins to be explored, so you can’t expect definitive answers, but only mutable observations.

[1] In this analysis it is not included the 1992 elections because they were conducted in a historically very different context.

[4] Due to rounding adjustments it doesn’t equal 100 %

https://www.cedesa.pt/wp-content/uploads/2022/08/image.png302619CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2022-08-17 11:00:002022-08-17 15:05:51Elections in Angola: polls and results predictions

The starting point for this study is the statement of a renowned researcher during the II International Congress of Angolanistics according to whom the “next elections in Angola should be the least transparent and credible.”[1]

It is recalled that Angola had its first elections in 1992, after which there was a resurgence of the civil war that ended in 2002, and it only held elections again in 2008, followed by electoral acts in 2012 and 2017, so far, four electoral processes in Angola.

The next elections are scheduled for August 24, 2022.

In all the elections whose count has reached the end, the MPLA, the party in government since independence in 1975, won with the following results: 1992- 53.74%; 2008- 81.76%; 2012-71.84%; 2017- 61.05%.

Table no. 1- Winner of the elections in Angola (1992-2017)

1992

MPLA

53,74%

2008

MPLA

81,76%

2012

MPLA

71,84%

2017

MPLA

61,05%

Interestingly, in every election, even in 1992[2], which had wide international coverage and had over 400 foreign observers, the main opposition party alleged fraud.

In 1992, these allegations resulted in renewed civil war and undisguised massacre and violence. In fact, the resolution of the dispute only took place with the death of the opposition leader and the end of the war in 2002. In the other elections, there was final acceptance of the results and integration into the constitutional-legal functioning.

In 2008, 90 observers from the European Union were present, and the MPLA’s victory was overwhelming. It was, in fact, the time of the oil boom. Even so, the opposition claimed fraud, and demanded a repetition of the elections due to delays that marked the process, described by the opposition leader as “a disaster”, with numerous delays across the country. In any case, despite these protests, the elections were eventually accepted and the deputies took their seats. This time there was no war and a certain democratization of public life began.

2012 was again the year of elections, and again, there were reports of irregularities, but without the vocality of the past. The opposition took their seats in parliament and played their part.

In the year 2017, the African Union sent observers to the elections, with the aim of guaranteeing democratic elections, but the European Union decided not to send a large team of observers. The opposition contested the results, but ended up accepting them after decisions by the Constitutional Court that validated the elections.

There are patterns that repeat themselves. The first two are obvious, the victory of the MPLA and the permanent contestation of the process by the opposition. There is also the intervention of external observers, for example 400 in 1992.

Despite repeated accusations of fraud on the part of the defeated candidates, what is certain is that, with the exception of 1992, they always ended up accepting the results and taking their seats in the National Assembly.

Comparisons: Transparency and Democracy in 2022

The question that we are going to answer is whether the present elections, scheduled for August 24, 2022, represent a decrease in the electoral conditions of the past, as some researchers claim, or if, on the contrary, even though they are not perfect, they present a clear evolution in terms of transparency and democracy?

To assess the conditions, we will review current legislation, as well as the characteristics of the current public scrutiny compared to the past, as we believe that this is the realistic critical mechanism to assess the transparency of elections.

Legislation

Regarding the legislation in force, there are some aspects to emphasize, many of which have been the target of misunderstandings or not very literal interpretations. Elections are now regulated by Law No. 30/21 of 30 December, which amended Law No. 36/11 of 21 December — Organic Law on General Elections (OLGE). In the current legislation we have to highlight the following topics that focus on the electoral process:

i) Basic conditions: demonstration, right to broadcast and financing

During the electoral campaign period, freedom of assembly and demonstration for electoral purposes is governed by the provisions of the general law applicable to the exercise of freedom of assembly and demonstration, with the following specificities (article 66 of the OLGE):

a) Processions and parades may take place on any day and time, respecting only the limits imposed by freedom of work, maintenance of calmness and public order, freedom and traffic management, as well as respect for the period of citizens’ rest.

b) The presence of public authority agents at meetings and events organized by any candidate can only be requested by the competent bodies of the applications, with the organizing entity responsible for maintaining order when such a request is not made.

c) The communication to the competent administrative authority of the area about the intention to promote a meeting or demonstration is made at least 24 hours in advance.

What results from the law is a broad possibility of demonstration, with no constraints or noticeable obstacles.

It should be noted, moreover, that in the pre-campaign period there have already been large demonstrations without incident, either by the government party or by the opposition.

The opposition leader has moved freely in the territory from north to south, specifically, from Cabinda to Menongue and carried out large mass acts, without any impediment or confrontation. This fundamental aspect for the electoral process has been ensured.

In relation to the right to broadcast, article 73 of the OLGE provides that candidates for general elections are entitled to use the public broadcasting and television service, during the official period of the electoral campaign, in the following terms: a) Radio: 10 minutes a day between 3 pm and 10 pm; b) Television: 5 minutes a day between 6 pm and 10 pm.

The law guarantees what we might call the minimum amount of political intervention during the electoral campaign period.

The global funding of all political parties carried out by the State is also provided for and is imperative under the terms of article 81 of the OLGE, which provides that the State will allocate an amount to support the electoral campaign of candidates for the general elections, which is distributed equitably, and it can be used to support the List Delegates.

The letter of the law offers sufficient guarantees that certain minimums of equity and competition between parties are upheld for the 2022 elections[3].

ii) Voting and counting of votes

This is an area where there has been a lot of discussion and perhaps misunderstandings or misinterpretations. Therefore, it is important to underline the essential provisions of the law.

Firstly, polling stations, contrary to what one might think in light of some published analyses, play a central role in the process. From the outset, the List Delegate present at the Polling Station can request clarifications and submit, in writing, complaints regarding the electoral operations of the same Polling Station and instruct them with the appropriate documents, and the Polling Station cannot refuse to receive the complaints, and must initial them and attach them to the minutes, together with the respective resolution, whose knowledge will be given to the claimant. (Article 115 of the OLGE).

This means that there is a direct inspection by each of the parties in each of the Polling Stations. What we might call an atomist oversight. Every atom of the election is being verified.

Afterwards, it is still at the Polling Station that the polls are opened and the votes are counted, also contrary to what has been stated.

In fact, once voting is over, the Chairman of the Board, in the presence of the other members, opens the ballot box, followed by the counting operation in order to verify the correspondence between the number of Voting Ballots in the ballot box and the number of voters who voted at that Polling Station. (Article 120 of the OLGE).

Then, the President of the Polling Station orders the counting of the Ballots, respecting the following rules:

a) The President opens the bulletin, displays it and reads it aloud;

b) The first scrutineer records the votes allocated to each party on a sheet of white paper or, if available, on a large board;

c) The second scrutineer places, separately and in batches, after displaying them, the already read votes corresponding to each of the parties, the blank votes and the null votes;

d) The first and third tellers proceed to the counting of the votes and the Chairman of the Board to divulge the number of votes that fell to each party.

After this operation, which is well detailed in the law, the President of the Polling Station compares the number of votes in the ballot box and the sum of the number of votes for each lot. The List Delegates have the right to verify the lots without being able to complain in case of doubt to the Chairman of the Board who analyzes the complaint. (Article 121 of the OLGE).

Consequently, we have an electoral act that is supervised and the votes are counted locally at each Polling Station with the presence of delegates from each party.

This is what the law defines.

After this local operation, a Minute of the Polling Station is drawn up by the Secretary of the Table and duly signed, in legible handwriting, by the President, Secretary, Tellers and by the List Delegates who have witnessed the voting, being then placed in a sealed envelope that must be duly forwarded, by the quickest route, to the Provincial Electoral Commission. (Article 123 of the OLGE). Subsequently, the National Electoral Commission is responsible for centralizing all the results obtained and for distributing the mandates (article 131 of the OLGE). In summary, the national tabulation is based on the summary minutes and other documents and information received from the Polling Stations (article 132 of the OLGE).

It can thus be seen that the counting of results is carried out at the local level, with no centralization of the opening of the polls or the counting, the centralization is carried out a posteriori, based on the results obtained at the Polling Stations.

Looking at the legal provisions mentioned above, a transparent and properly supervised mechanism can be seen at the local level.

Added to this mechanism is the rule of article 116 of the OLGE which makes it mandatory that the technologies to be used in the scrutiny activities meet the requirements of transparency and security.

The same rule requires the audit of source programs, data transmission and processing systems and control procedures and makes it imperative that before the beginning of each election, the Plenary of the National Electoral Commission carry out an independent, specialized technical audit, for public tender, to test and certify the integrity of source programs, data transmission and processing systems and control procedures to be used in tabulation and scrutiny activities at all levels.

iii) The transparency of the President of the Republic election

The Voting Ballot is printed in color, on smooth and non-transparent paper, in a rectangular shape with the appropriate dimensions so that it can fit all the candidacies admitted to the vote and whose spacing and graphic presentation do not mislead voters in the exact identification and signage of the application one has chosen.

The serial number, the statutory designation of the political party, the name of the candidate for President of the Republic and the respective passport-type photograph, the acronym and the symbols of the political party or coalition of political parties, arranged vertically, are printed on each Ballot, one below the other, in the order of the draw carried out by the National Electoral Commission, after the approval of the candidacies by the Constitutional Court (article 17 of the OLGE).

This means that despite the presidential election method chosen by the Constitution, voters clearly know who they are voting for for President of the Republic. It has the face and name indicated.

iv) Electoral litigation

The assessment of the regularity and validity of elections is ultimately the responsibility of the Constitutional Court (article 6 OLGE). This rule commits the Constitutional Court (CC) all final decisions on elections, not the National Electoral Commission (NEC).

The fact that the CC has the final word and not the NEC is an added jurisdictional guarantee. At the present time, as we will see later, this is relevant because the CC has been the subject of a great deal of public scrutiny, making it more difficult to make decisions that have no legal basis.

Public Scrutiny

It is natural, above all for the supporters of a realistic vision of the law[4], in which we include ourselves, according to which what is important is not what is written in the law, nor even the meta-legal principles on which it is based, but its application and practical result, one is not satisfied with the mere legal enumeration, even if it appears well constructed and promising, as it seems to us to be the case with the present Organic Law on General Elections.

It is necessary to invoke other real factors that allow a more objective assessment of the electoral phenomenon in Angola, as expected for 2022.

We understand that the key factor is the public scrutiny that the electoral process is having. Public scrutiny understood as a thorough examination and diligent investigation of a phenomenon carried out by society in general, and not just by specific bodies that may or may not be aligned with a given political or ideological option.

Our argument is that the greater the public scrutiny to which an electoral phenomenon is subject, the greater its transparency and democracy and the lower the probabilities of fraud, with a direct relationship between scrutiny and transparency.

Now, the brief excursus that we carried out on the several elections that took place in Angola, and removing the one from 1992, which due to its specificity and historical context has no place in this comparison, and considering that some of our contributors personally followed the 2012 and 2017 elections, allows us to advance with some trends in relation to aspects of scrutiny by members of civil society or non-political structuring bodies of the community. These themes lead us to a qualitative comparison between 2008 and 2017.

First, let’s highlight the Catholic Church. Possibly, as a result of certain accusations of collaboration with the colonial power and some clash with the post-independence Marxist ideology, the Catholic Church, in general, had committed itself in the previous elections to a discreet and little public intervention role, not contributing for a strong debate about the electoral process in the previous elections (2008 to 2017).

This will not happen in 2022, following in the footsteps of its counterpart in the neighboring Democratic Republic of Congo (DRC) in which the Catholic Church played a decisive role in the 2018/2019 electoral transition between Kabila and Tshisekedi, the Angolan Catholic Church has adopted a manifesto leading role in the preparation of the Angolan elections. Its bishops and priests are active in their pastoral care and in their homilies and have an intense public activity, demanding adequate elections[5].

It is precisely this Catholic activism, bearing in mind that according to statistics, around 40% of the Angolan population is Catholic[6], which allows us to conclude that the scrutiny that the Catholic Church is carrying out of the elections will not leave a large part of the population indifferent and obliges by itself to increased transparency in the process. In other words, Catholic scrutiny and its multiple organizations is, in itself, an intrinsic factor of transparency.

A second factor that we notice different in relation to other Angolan elections is the role of social networks. These will cover about a quarter of the voting population[7], but perhaps more of those who actually vote. By frequenting social networks, one can easily glimpse the intensity with which they talk about the elections and how they discuss their realization and the need for transparency. A candidate for deputy for the opposition party and activist constantly present on the networks like Hitler Samussuku has 52,000 followers on Facebook and his posts often reach more than 1000 likes. This is just a random example, but many others could be mentioned.

Never before have social networks in Angola been so alive and active as in this period, contesting, discussing and affirming positions.

As in the situation of the Catholic Church, we understand that this digital scrutiny has a double function. By itself it is synonymous with transparency and at the same time it increases transparency by placing the discussion on the elections in the public space.

We have here two factors intrinsically conducive to electoral transparency: the activism of the Catholic Church and digital activism.

Finally, it is worth mentioning the issue of international observers. In the difficult year of 1992, according to public information, 400 international observers were present[8], in 2017, more than 1000 observers will have been present[9], currently, according to publications that have focused on the subject, 2000 national observers are expected for 2022 and an undisclosed number of international observers. It should be said that in view of the aforementioned activism of the Church and in the digital world, national observers will play a very intense role, contrary to what could happen in the past.

Conclusions

The issue we studied here is not the platonic perfection of the Angolan elections, but the evolution of electoral transparency since 2008 with the forecast for 2022.

What we have found, taking into account two indices, legislation and public scrutiny, is that, at the moment, there is a law strong enough to hold free and fair elections, and that public scrutiny, namely by the Catholic Church and its satellite organizations and also through social networks, has never been as high as it is today.

To that extent, even with imperfections, it is expected that these elections will be more transparent than in the past, because if this does not happen, public opinion will feel better and more deeply than in the past.

[3] We do not discuss in this work the problem of public service imbalance in the pre-campaign period. It will possibly be the object of another study pointing out solutions and needs for a holistic view of the situation encompassing all sources of news: public, private, foreign and digital.

[4] See for exemple Rui Verde, Juízes: o novo poder, 2015.

https://www.cedesa.pt/wp-content/uploads/2022/06/28263904.jpg10801920CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2022-06-29 12:53:002022-06-23 17:59:15Theories of electoral fraud, legislation and public scrutiny in Angola

1- Framework: the requirements and agents of tourism promotion in Angola

Angola is gradually seeking to diversify its economy, choosing tourism as one of the main priorities for structuring economic policy. As is well known, the reconstruction started from 2002 did not focus on tourism, but on the oil, mining and construction industry. Once this model was exhausted, diversification became the keyword for development.

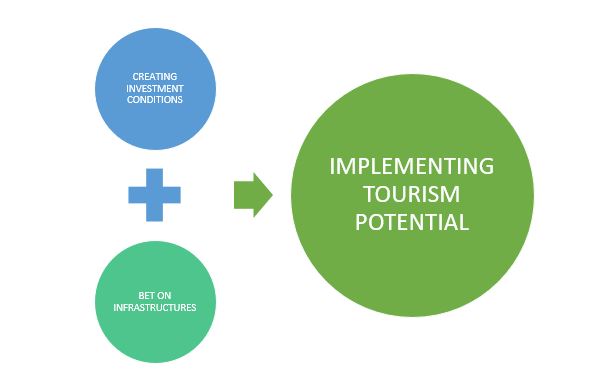

Since it is conspicuous that Angola has an enormous tourist potential, the truth is its implementation implies the removal of sveral obstacles and the creation of adequate conditions. We refer to two essential axes to create these conditions: the first is the creation of favorable conditions for investment in the tourism sector, this implies the review of the investment law that has already taken place, the removal of barriers to market entry and the facilitation of bank credit for new projects.

The second axis is of an infrastructural nature and requires the creation of an adequate transport network, roads, planes and boats, as well as a climate of criminal security, in addition to the facilitation of tourist visas.

Figure 1: The 2 axes for the development of tourism potential

Furthermore, the growth of tourism cannot be solely dependent on the State, it is naturally responsible for the regulation, supervision and creation of infrastructure and conditions. However, the fundamental role belongs to the private business community, which must advance and establish partnerships to enter the international circuits. And, finally, it is also up to the provincial, municipal and communal leaders to encourage and leverage their resources.

State, businessmen and local leaders form the tripartite partnership that must come together to launch tourism in Angola.

In 2019, at the opening of the World Tourism Forum that took place in Luanda, the President of the Republic made it very clear what the executive wanted for the sector: within the framework of the diversification of the economy, tourism should play a role in promoting development and generating income and employment. For this to materialize, the government should invest in the short and medium term, in the expansion of hotel infrastructures and in the infrastructure of the tourist centers of Cabo Ledo, Calandula and the Transfrontier Project of Okavango Zambeze, with the purpose of increasing the offer and the options diversity of tourists and customers in general[1].

Recently, a possible crisis in tourism in Europe has been discussed, admitting that Greece, Italy, France, Spain and Portugal are affected by the sanctions on Russia resulting from the war in Ukraine (which, in relation, at least to Portugal, is doubtful, as the country was not dependent on Russian tourism), Egypt has not yet fully recovered from fear of bomb attacks, Indonesia struggles to contain Muslim fundamentalism, India struggles with rising pollution levels, Kenya and Senegal could be invaded by Islamic agitation, favorite destinations like Turkey, Israel, Thailand and Dubai are somewhat saturated. This scenario is described in a somewhat emphatic way, however, it opens up opportunities for tourism in Angola, as it represents a certain verifiable trend.

The country has potential in tourism to attract tourists, as Cape Verde and Botswana did; it has paradisiacal beaches, desert and forests, rivers of great flow, mountains, exuberant fauna and flora, and, above all, a welcoming people and a rich and varied gastronomy.

2-Scenario of Angolan tourism

There is no developed tourism industry in Angola. The few areas that are developed took advantage of the country’s natural beauties, rivers, waterfalls and the 1,650 km of Atlantic coast. As the official brochures describe: “The humid tropical climate [of Angola] has created an exuberant flora and rich fauna spread over regions with forests, savannas, impressive mountains, rivers, beaches that seem to stretch without limits, waterfalls, oases and beautiful landscapes which seem to go on to infinity and are all immaculate and intact. An endless summer of warm afternoons bathed in warm breezes to contemplate adventure and discovery.”

Angola has an extreme natural beauty that reveals itself as a promising tourist destination. Mussulo Island and Cabo Ledo are examples of places with an immense capacity to attract tourists, as well as several areas of the provinces such as Namibe, Benguela, Malanje and Cuanza-Sul. The Calandula Waterfalls in Malanje are particularly impressive.

However, currently, most foreign travelers arriving in Angola are not tourists, but entrepreneurs, workers and consultants. This means that hotels are geared towards business and not tourism or leisure. As businesses have been through a serious crisis since 2015, that only now (2022) is truly emerging, that is to say that in recent years there has been a markedly low occupancy rate in hotels, which went from 84% in 2014 to 35% in 2017 and 25% in 2018. This drop in occupancy reflected the crisis that overshadowed the country, not the lack of interest in tourism. The drop in oil prices that has occurred since 2014 and until last year led to a decrease in economic activity in Angola, which resulted in fewer business travelers occupying hotels.

Those responsible recognize that there are currently major weaknesses in the tourism sector, namely “lack of concrete support and incentive measures, difficult access to places, potential resources and tourist attractions, lack of appreciation of tourist resources, lack of flexibility of the banking system to finance tourist projects, deficit in terms of hotel and tourist training establishments, excessive dependence on imports, due to the deficit in domestic production, lack of tourist culture, lack of greater openness in granting entry visas to the main tourist-issuing markets of the world and reduced purchasing power of Angolans[2]”.

However, these unsatisfactory numbers and facts do not represent any structural trend. Between 2009-2014 Angola registered strong growth in the hotel sector with revenues exceeding 45 billion kwanzas (100 million euros at the time exchange rate), creating around 223 thousand jobs. Thus, there is clear potential for the tourism business.

3-Touristic locations and potential markets

Angola has numerous tourist attractions, among which we can highlight the national parks of Kissama and Iona, Quedas de Calandula, Ruacaná, Mussulo, Miradouro da Lua or the Zambezi River.

It is possible to promote the development of hotels and tourist resorts aimed at vacationers in some of the areas specifically intended for sun, sea and sand tourism, such as Cabo Ledo, 120km from Luanda in the municipality of Quiçama, which has 2,000 hectares of enormous beauty and is a potential location for world surfing, once visa processes are facilitated.

Another alternative for nature tourism is Calandula, Malange, which has the most impressive waterfalls in Angola and is the second largest in Africa at 150 meters high and 401 meters wide. An area of 1,978 hectares of endless vegetation and waterfalls as far as the eye can see and which has an enormous potential for tourist investment: tourist accommodation, restaurants, entertainment, golf and casinos.

The idea of a museum route also emerged. The initiative of this route is to awaken and increase the culture of visiting museums, in order to create a heritage identity. This route includes the Iron Palace, the National Museum of Military History (Fortaleza São Miguel), the National Museum of Natural History and the National Museum of Slavery, passing through several hotel units. This route should serve as a model for implementation in all provinces of the country.

The target markets for Angolan tourism should be Russia (after the peaceful resolution of the war) and China, which are now the countries from which more than 50% of international tourists come, Angola has everything it takes to absorb a substantial share of these markets. Furthermore, as mentioned above, it could absorb some European demand, especially in the area of adventure and new ecological experiences.

4-Strategic axes and special tourism areas (STA)

As mentioned above, the strategy for tourism must be based on two axes: the promotion of investment and the creation of infrastructure.

We recognize that there is a new favorable climate for investment and also an effort, especially within the scope of the CPLP, to make the bureaucratic process of issuing tourist visas more flexible, that is, conditions are being developed for a new strategy for attracting tourists.

According to an Angolan official, the documents required for the licensing of tourist developments were reduced, from 11 documents previously required to three. The validity of permits was changed from three to five years, the process of decentralizing the permit issuance system is in progress. All these actions aim to improve the business environment in the tourism sector. Regarding visas, the same official points out that the process was already more difficult. He made it known that there have been significant advances, which need to be improved, to attract more tourists[3].

The same officials argue that in terms of infrastructure there are gaps that are easy to solve; Catumbela Airport (Benguela) may be equipped with mechanisms to receive direct international flights, transport is part of the investment that is up to the private sector, the Benguela Railway line passes hundreds of meters from the airport, connects to Zambia and to the Democratic Republic of Congo and goes to Tanzania on the Indian Ocean, Lobito has a large-capacity port, and the expansion itself is providing parallel investments in health, training, services, and the capacity to produce skilled and competitive labor.

At the government level, tourism is recognized as a strategic sector in the National Development Plan 2018-2022, as a guarantee of intensive labour, alongside agriculture, various industries and fisheries. The National Development Plan includes some specific actions, such as the improvement of communication with the Tourist Development Poles, the elaboration of projects for the construction and rehabilitation of hotel and tourist infrastructures, state and mixed infrastructures, the identification of priority development areas, with the aim of recovering and developing the entire heritage of the hotel and tourist network.

Another government official, who has since ceased his duties, underlined that in addition to Angola starting to reduce restrictions and bureaucracy, as part of the strategy to relaunch tourism and promote the attraction of investment to the sector, he wanted to draw attention for the country, with the collaboration of the international supermodel Maria Borges, who would help to promote the potential. The strategy would involve calling an international name, Maria Borges, to help promote the country’s culture, history and main tourist destinations[4].

With the new strategy for the promotion of tourism, Angola hopes to integrate the list of the main tourist destinations in Africa by 2025[5] .

***

However, it is not possible in the short term to create a complete national infrastructure for tourism. There must be pragmatism and realism in political approaches to promoting tourism in a country where tourism has been almost non-existent. It is in this sense that the best solution must be dual and with different deadlines.

In the medium term, a national tourism strategy should be developed. However, in the short term, there must be a focus on what we will call Special Tourism Areas (STA). The STAs would be five areas of the country in which the State in partnership with the private sector and local authorities would focus to create infrastructure and specific conditions for tourism. Areas with easy access, hotels, restaurants, guaranteed security and maybe free transit visas to visit these areas. Preferred areas chosen to test the STAs could be Malanje, a beach area with urban animation, a paradisiacal-style beach area, and a city with a lot of history or an area with ecological interest aimed at European tourists.

Figure 2: Special Tourism Areas

These areas would have privileged tax treatment and the elimination of visas should be considered for those who went there for up to 15 days. This proposal would imply the elimination of visas for foreign tourists from the target markets who travel to the STAs for a maximum period of 15 days in tourism. All they need to do is present a return flight ticket and proof of booking in tourist accommodation.

There would thus be the creation of pilot districts dedicated to tourism, small capsules of what could be global tourism in Angola in the future.

Conclusions

Tourism can be one of the areas of excellence in the ongoing diversification of the Angolan economy, as it is a sector where the country has enormous potential. The investment in tourism must be a tripartite work of the State, private business and local communities. Target markets will be Asia and Russia (after the Ukrainian War settlement), as well as eco-tourists or European adventurers.

For tourism to exist in Angola, investment conditions must be provided (which is ongoing) as well as adequate infrastructure in physical terms and easy to move around.

It is advisable to proceed in the short term with the creation of Special Tourism Areas that work as pilot experiences for tourism promotion. Areas that will bring together hotels, restaurants, local entertainment, security and easy access, and elimination of visas for tourism in the STAs. And then with the results of these STAs extend to the entire country.

1-Introduction: characterization of the water catchment construction project on the Cunene River

It has been our concern to seek concrete answers to specific problems, in addition to the intense rhetoric in pre-election periods. In this case, one of the topics that interests us is the drought in southern Angola. As we mentioned in a report from last November[1], we follow the works in progress related to the Drought. One of them is almost ready to be inaugurated and operational. It is about that project we give an account in this document.

This report focuses on the execution of the Structuring Works to Combat Drought, specifically the design and construction of a catchment on the Cunene River and the construction of pipelines to the localities of Cuamato, Namacunde and Ndombondola.

This project has 2 Lots:

• LOT 1 – Design and Construction of Intake on the Cunene River, Pumping System, Pressurized Duct, Open Channel from Cafú to Cuamato and 10 Chimpacas (water reservoirs);

• LOT 2 – Design and Construction of Adductor Channel from Ombala – Cuamato to Ndombondola, Adductor Channel from Cuamato to Namacunde and 20 Chimpacas.

Regarding Lot 1, the General Contractor is SINOHYDRO Corporation Limited, a limited company incorporated in 2011 in Luanda whose property is held by Chinese companies. The supervision is carried out by the Consortium GWIC – Angola, S.A / SINTEC – Consultoria de Engenharia, Lda. As for Lot 2, the responsible entity is the same, except for inspection; in this case the responsible entity is TRIEDE Angola, Lda. A prestigious company from Portugal.

The deadline for the project conclusion points to the end of March 2022. Therefore, a very brief opening is expected.

The value of the two works reaches 140 million US dollars.

Fig. 1: Lots 1 and 2 of the Project (Cunene Province, Angola)

2- Projects explanation

Lot 1 comprises the water transfer works from the Cunene River, in the Cafu section, to the localities of Cuamato, and is based on the construction of the water intake, pumping station, pressurized pipelines, feeder channels and associated facilities.

The Project consists of the following main elements:

• Intake from the Cunene river bed, including the water intake structure, floodgates, grates and other associated equipment;

• Pumping Station with a capacity of 2 m3/s;

• The Pumping Station will be equipped with two active pumps and one backup pump in the first phase. The pumps will be turbine-type, vertical, with a nominal capacity of 1 m3/s;

• Gravity channel coated to receive 6 m3/s. The length of the channel is 46.54 kilometers with connection to the reservoir, considering the alignment that minimizes earth movements;

• A North-South alignment was established from Cafu to the Ombala-Io-Mungo region. In the end, the gravity channel will be divided into two branches, serving the localities of Namacunde and Ndombondola.

Fig. 2: General Conductor Channel | Manual cladding with concrete class C20/25, 35 km, 1 front km (45,954)

Fig. 3: Chimpacas | State of the Chimpaca

In turn, Lot 2 comprises the works of the following channels, which derive from the Bypass Structure (BS) of flows from the General Conductor Channel (GCC):

• West Conductor Channel – WCC (Cuamato / Ndombondola), with a length of around 53.04 kilometres;

• East Conductor Channel – ECC (Cuamato / Namacunde), with a length of about 53.11 kilometres.

Fig. 4: East Adductor Channel (EAC)

Fig. 5: Placing the fence on the Chimpacas of the East and West channels

3-Delays, advances and resources used

Due to several constraints that occurred in 2021, such as lack of diesel in the south of Angola, water for concrete production and respective curing, cement at work, and rainfall, the completion of the work slipped a little, since completion was initially scheduled for February. Now the completion date is for the end of March (maybe early April).

A total of 1250 workers (Lot 1 – 417; Lot 2 – 833) were assigned to the works, 162 (Lot 1 – 70; Lot 2 – 92) of Chinese nationality and 1088 (Lot 1 – 347; Lot 2 – 741) of Angolan nationality. Equipment is allocated to the works, in a total of 388 units, of which 135 in Lot 1 and 243 units in Lot 2.

4-Benefits for the population

The project, as presented above, consists of the construction of the water transfer system for the Cunene River, from the locality of Cafu to the Chanas region in the province of Cunene, in Angola. The interventions are included in a total investment of more than €140 million made by the government to deal with long periods of drought that dramatically affect people and animals.

The aim is to create the right conditions for the development of agriculture and livestock, increasing resilience to climate change in this practically deserted region of southern Angola, subject to frequent prolonged droughts, benefiting hundreds of thousands of inhabitants and livestock, as well as providing water for irrigation in an area estimated at 5,000 hectares.

The project is expected to benefit approximately 200,000 inhabitants and 250,000 head of cattle. It should be noted that Cunene has about 900 thousand inhabitants, therefore more than 20% of the population is covered by this work.

https://www.cedesa.pt/wp-content/uploads/2022/03/Rio-Cunene.jpg345640CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2022-04-03 11:00:002022-03-31 15:48:20Structural works to combat the effects of drought in southern Angola

It is a fact that the war in Ukraine is affecting the entire world economy, and, certainly, this impact will also have political consequences[1], as the International Monetary Fund (IMF) immediately recognized.

The question that will be addressed in this report is about the specific impact of the war on the Angolan economy, which, as we know, is undergoing a demanding reform period and is about to emerge from a deep crisis. It will also superficially assess whether the economic impacts will have political influence.

The two faces of the impact of the oil price in Angola

Naturally, the first impact in Angola refers to the price of oil. The rise in the price of oil was a trend that had been going on for some time and was accentuated with the outbreak of the war. To some extent, it is not a novelty brought about by the Ukrainian crisis, but a direction that has been underway for months.

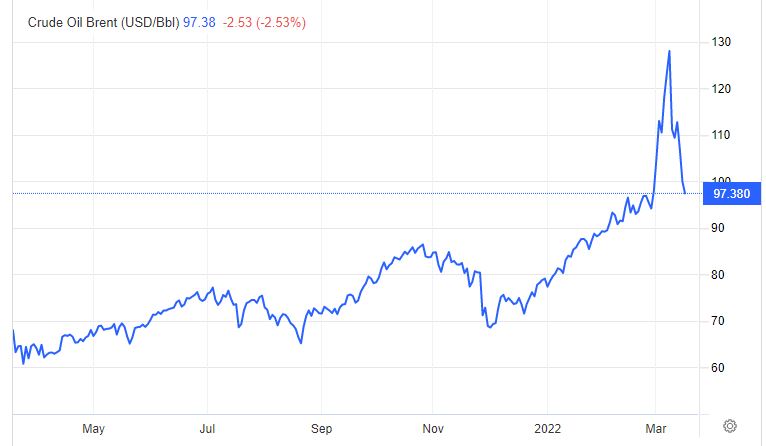

On January 31, 2022, the price of a barrel of Brent was USD 89.9, on February 14, 2022, the value was USD 99.2. It is a fact that with the beginning of the war it reached USD 129.3 on March 8. At this point (March 16), it stabilized at USD 99.11. It seems that the equilibrium price of oil in the near future will be between USD 95-100, with, obviously, the possibility of shocks that make it rise or fall abruptly.

Fig. nº 1- Daily Chart of the Price of a Barrel of Brent (May 2021-March 2022)

Source: Trading Economics.com

In relation to Angola, we have to start from the budgeted forecast for 2022, which calculated the price of a barrel at USD 59. Therefore, there will be an added value since the beginning of the year corresponding to a minimum of 50% more. In this sense, as the budget was balanced, it means that there will be a financial surplus, which is obviously good news.

This rise in the price of oil therefore has, in the first place, two positive effects for Angola.

The first is at the level of extraordinary Treasury revenue, which will naturally increase. In simple terms, it can be said that there will be more money available from the state.

The second effect, which is already being felt, is the so-called “feel good factor” (or confidence index). Entrepreneurs and families are rethinking their expectations in a more positive direction, hoping for better signs from the economy. According to the Angolan National Statistics Institute, businesspeople are finally optimistic about the short-term prospects of the national economy, after remaining pessimistic for more than 6 years[2]. The rise in the price of oil is not the only reason for the optimism revealed, but it helps.

Note, however, that oil price gains do not translate directly into a positive budget balance. There are several constraints in translating the rise in oil prices into direct budgetary benefits for Angola.

The first of these is the type of relationship with China. China is the main buyer of Angolan oil. We do not know how the contracts are made and whether they automatically reflect price fluctuations. In the past, some intermediaries in the purchases and sales of oil to China even entered into fixed-price contracts that greatly harmed the Angolan Treasury[3]. It is imagined that such “schemes” no longer exist, but there are no certainties. What is certain is that, probably, the contracts between Angola and China regarding oil will contain some type of “dampers” that will imply that there is no direct impact on prices. Furthermore, some oil experts, such as those at Chatham House, believe that the fact that China buys around 2/3 of Angolan oil (actually 70%[4]) allows it a certain monopolistic control of the price, meaning that Chinese purchases are made in order to lessen price rises, undermining Angolan advantages[5].

Second, we have debt service. Apparently, there are contractual mechanisms that imply that a higher price of oil implies an increase in debt service, that is, in payments to be made. The Minister of Finance, Vera Daves, has already acknowledged that “what results from the price increase cannot be made an arithmetic account with production” and that the price of a barrel of oil, above one hundred dollars, forces Angola to pay more to their international creditors[6].

Furthermore, the rise in the price of oil also has a possible negative effect on the Angolan budget, which refers to the price of fuel sold to the public. As is well known, this price is subsidized by the State; to that extent, if the cost of oil increases and the government does not increase fuel, it means that it will have to bear more subsidies and spend more to maintain fuel prices. If you don’t, you could be fueling inflation, which is no longer low in Angola, and creating social problems and discontent.

There are four factors here: price increase, relations with China, increase in debt payment obligations and increase in fuel subsidy that have to be taken into account to assess the real impact of the rise in oil prices on the accounts and the Angolan economy.

In fact, we do not have precise figures on these impacts, only ideas of magnitude, and in view of these, the conclusion that can be drawn is that a 50% increase in the price of oil in relation to what is foreseen in the Budget leaves a treasury slack that is still accentuated after the increase in debt service payments and support for the rise in fuel prices, and it is undoubted that a financial “cushion” will be created.

The question of food prices

Alongside the price of oil, many other commodity classes are rising in price. One of them is cereals, namely wheat.

Ukraine and Russia together account for a quarter of all world wheat exports. The conflict is dramatically driving up wheat prices. With the start of the war, the price of a bushel of wheat rose to $12.94, 50% more expensive than at the beginning of 2022.

In the midst of a war, it is unclear whether Ukraine’s farmers will be willing to spend whatever capital they have to plant the next harvest, or even if they will be in a position to do so. What is certain is that Ukraine has announced a ban on all exports of wheat, oats and other staple foods to avoid a massive food emergency within its borders. Therefore, wheat exports from Ukraine, even if there is production, are compromised.

Unlike oil, which affects prices almost immediately, grain prices take weeks, if not months, to reach consumers. In reality, raw grain needs to be shipped to processing facilities to make bread and other staples – and that takes time. In this sense, possibly, it will not be an immediate crisis for Angola, but it will reach the country.

According to government sources, Angola is self-sufficient in six basic agricultural products: cassava, sweet potato, banana, pineapple, eggs and goat meat. However, wheat is the most imported commodity, accounting for 11%[7]. Let us recall that wheat is an essential element in the diet of Angolans, which a few months ago led the Minister of Industry and Commerce to suggest replacing bread with cassava, sweet potatoes, roasted bananas and “ginguba” (peanuts). This statement has generated much criticism. However, from the strict point of economic self-sufficiency it may make sense, since possibly the price of bread will rise and eventually the price of national goods may fall, if there is an adequate competitive market.

What is certain is that Angola could be in the same danger as Egypt, an extremely wheat-based crop that suffers social upheaval when the price of wheat rises.

When grain prices soared in 2007-2008, bread prices in Egypt rose by 37%. With unemployment on the rise, more people became dependent on subsidized bread – but the government didn’t react. Annual food inflation in Egypt continued and reached 18.9% before the fall of President Mubarak.

Most of the poor in these countries do not have access to social safety nets. Bread images became central to the Egyptian protests that led to Mubarak’s downfall. Although the Arab revolutions were united under the slogan “the people want to overthrow the regime” and not “the people want more bread”, food was a catalyst. Incidentally, it should be noted that “bread riots” have been occurring regularly since the mid-1980s, usually after the implementation of policies “advised” by the World Bank and the International Monetary Fund.

Angola is not Egypt, but it is essential that the government pay close attention to the evolution of wheat and bread price to avoid social unrest, at a stage when it begins to emerge from the prolonged crisis.

However, as in the case of oil, there is another side, and in this case it is positive. The crisis in agricultural production resulting from the war could be a turning point for foreign investors to invest in agriculture in Angola. Angola is one of the countries in the world with the most potential, as we have already mentioned in a previous report[8], so this may be the time of opportunity for investors to see Angola’s agricultural capacity and take advantage of it. One of the most promising sectors with the most potential is agriculture. There is currently a combination of factors that make it one of the most profitable bets for investment in Angola.

Conclusions and recommendations

The war in Ukraine has several impacts on the Angolan economy.

The rise in the price of oil, not bringing directly proportional revenues, creates a “cushion” in the Treasury and a “feel good factor” in the business community, which could be a growth booster.

The rise in the price of cereals, especially wheat, can create serious inflationary pressures and discontent among the population, a situation for which the government must be aware. At the same time, it will draw attention to the enormous investment potential that Angola has as an agricultural country.

The government should create a special reserve derived from the gains from oil to guarantee the supply of cereals to the poorer sections of the population and also to promote agricultural investment in Angola.

https://www.cedesa.pt/wp-content/uploads/2022/03/ucrania-war-scaled.jpg13471920CEDESA-Editorhttps://www.cedesa.pt/wp-content/uploads/2020/01/logo-CEDESA-completo-W-curvas.svgCEDESA-Editor2022-03-21 09:04:002022-03-21 09:37:03The economic consequences in Angola of the Ukraine war

Angola’s history has been one of constant and overcoming challenges, and its survival as a single entity has been threatened since independence in 1975. It is never too much to remember that independence itself was declared at different times and in different places by different entities, with greater or less legitimacy. Agostinho Neto proclaimed the independence of the People’s Republic of Angola at 11 pm on November 11, 1975, in Luanda. Holden Roberto, leader of the FNLA, announced the Independence of the People’s Democratic Republic of Angola at midnight on November 11, in Ambriz and Jonas Savimbi did the same for UNITA in what was then Nova Lisboa on the same day, declaring the birth of the Republic Social Democratic Republic of Angola.

Immediately, a civil war followed that more or less sporadically, covering larger or smaller areas, lasted until 2002. Attempts at external invasion were also frequent, South Africa, even before independence, entered Namibia and Mobutu’s Zaire the same to the north. Then it was Cuba’s turn, at the invitation of the Luanda government to also enter the country to counter the other invasions[1]. Indirect interventions by the then superpowers also abounded, and it is unnecessary to recall the threats of disintegration that the country experienced until the end of the civil war in 2002.

After that date, the threats posed to Angola diminished, although many remained latent and others emerged, such as those linked to the capture of the State and corruption[2].

Currently, there is an increase in external threats after 2002, not assuming the dramatic contours of the years after independence, but posing demanding challenges to the forces defending sovereignty, territorial integrity and national public order.

Separatism

Internally, we can see the rekindling of separatist attempts, both in Lundas and in Cabinda, which could be a trigger for other initiatives. In relation to Cabinda, reports have recently appeared on social media, replicated in some media of clashes between the armed wing of the Front for the Liberation of the State of Cabinda (FLEC) and the Angolan Armed Forces (FAA)[3]. These attacks, real or virtual, follow several complaints from the Democratic Republic of Congo (DRC) about Angolan incursions into its territory in apparent hot pursuit of FLEC members. Last August, the Chief of Staff of the Armed Forces of the DRC, Célestin Mbala Musense, criticized alleged incursions by the Angolan Navy into the country’s territorial waters in operations against rebels in Cabinda and claimed that FAA soldiers were multiplying incursions into the country, persecuting FLEC rebels[4].

Alongside this possible military upsurge, which is uncertain and about which there is no reliable information, there is a duly publicized current of opinion that invokes the need for a solution, although it is not clear what it is, or is tired of a confrontation.

The truth is that the Constitution of Angola (CRA) in its articles 5 and 6 is determinant: “… no part of the national territory or of the sovereign rights that the State exercises over it may be alienated.” It should be noted that this formulation implies that any territory always remains an integral part of the State, but does not prohibit different statutes and approximations, such as the establishment of autonomies always integrated into the national whole and of local authorities, more or less decentralized.

There is, therefore, a constitutional duty to combat any attempt at territorial secession, the CRA admitting the use of force to make this happen (“energetically fought”). In this context, the FAA will play a crucial role in preventing any dismemberment. In addition to constitutional law, it is also easy to see that any separation or “detachment” of Cabinda from Angola would have a disintegrating effect on the country, which as we know, historically, is a recent construction in progress.

This leads to the second threat of the same separatist type that exists in the Lundas. In January 2021, there was a bloody confrontation, the contours of which were duly described in Rafael Marques’ text, “”Miséria & Magia.[5]” In addition to socio-economic aspects, the event has been seen as linked to independence attempts by a self-styled Movement of the Portuguese Protectorate Lunda Tchokwe (MPPLT).

It is evident, in the first place, it is the duty of the State and the government to deal with the grievances of local populations, taking into account their developmental, economic and social demands. It is primarily a question of politics and progress. However, it is not worth ignoring that in the end, national integrity and sovereignty will always have to be guaranteed, and the FAA may play a decisive role in ensuring territorial cohesion.

That is why it is considered that a real threat to the sovereignty of Angola are the separatist impulses or intentions of part of its territory, with the FAA as the mainstay of the State to guarantee the integrity and unity of the State.

State capture and corruption

The second internal threat is linked to the aforementioned capture of the State and the fight against corruption. The option of political power was to hand over the fight against corruption to the common judicial means, therefore, this is not a function of the FAA, but of the police forces, criminal investigation and judiciary. The FAA only enters in what refers to the “capture of the State”. If forces or entities that benefit from corruption try to affect the normal functioning of the Rule of Law and Justice, weakening political power, it can be understood that the FAA will have a duty to defend constitutionality and legality, not intervening in specific judicial proceedings, but guaranteeing the conditions of tranquility and peace for the normal judiciary bodies to do their work. This is a difficult line to draw for the actions of the military, so the posture here must be understood as one of surveillance and symbolic support for the activity of the police forces and not of direct intervention.

If separatism and “state capture” are threats to sovereignty and peace in Angola, from the external point of view there are more and varied threats that have to be listed and have increased in recent years, requiring special attention from the FAA. The following stand out as external threats:

i) instability in neighboring countries, namely the DRC;

ii) the spread of terrorism designated as Islamic;

iii) crime and maritime piracy;

iv) increased competition between world powers with interests in African goods.

A few quick words about each of these segments:

i) instability in neighboring countries, namely the DRC

Although for the first time in 2018/2019 there was a peaceful transition of power in Congo (DRC), the truth is that the situation in this huge country is far from under control. The porosity with the Angolan border is a fact that is usually mentioned, but the main problem is that Tshisekedi, the President of the Republic and the state apparatus do not seem to control vast areas of the country that, according to some, are subject to militias promoted by Rwanda to search richness for processing in that country. A recent article by the Angolan professor and member of the Angolan government party, Benjamim Dunda, states that “What some do not know is that Rwanda is the gateway to the looting of excessive mineral resources in the DRC. Much of the endless instability of the neighboring nation of Mobutu has Kagame’s fingerprints. The Rwandan Patriotic Army (EPR) and Ugandan military, militarily occupy part of the territory of the DRC. Coltan (columbite and tantalite) is currently the most coveted ore in the technology industries worldwide. 80% of the world’s reserves are in the Democratic Republic of Congo.[6]” Without Dunda’s exalted tone, Laura McCreedy, from the International Peace Institute’s Center for Peacekeeping Operations, is on the same wavelength, referring already this month to reports of the resumption of proxy violence – attributed to Uganda, Rwanda and Burundi – as well as recent offensive operations against Allied Democratic Forces (ADF) by Ugandan forces and the alleged presence of Rwandan police and Burundian troops in eastern DRC, which is particularly alarming[7].

What appears is that there is a latent conflict in the DRC that is far from being resolved, to which is added a kind of asymmetric invasion, using the techniques popularized by Vladimir Putin in Crimea and Ukraine, by forces from Rwanda and perhaps Uganda within the DRC. This could soon provoke a more intense and not so covert war in the country with obvious effects in Angola. We shouldn’t forget that Angola was present in the so-called First Congo Civil War (1996-1997) and Second Congo Civil War (1998-2003), in addition to having directly or indirectly intervened in subsequent relevant moments in the DRC’s history. Consequently, it will not be indifferent to the evolution of the situation in the DRC and to this kind of discreet or disguised invasion that takes place, with the FAA having at least a deterrent role.

ii) the spread of terrorism designated as Islamic

The Angolan religious reality would not suggest an imminent danger from Islamic terrorism. However, there are two factors that must be taken into account to increase the degree of danger of Islamic terrorism in Angola.

The first factor is that what is often called “Islamic terrorism” does not have a real religious connotation, but represents a kind of franchise or brand adopted by insurrectionary movements or guerrillas in economically and socially degraded areas. This means that it is possible that in disaffected areas in Angola there may arise “Islamic” terrorist movements, which have nothing but Mohammedan but the designation, adopted to instill fear and terror in the populations and authorities. In fact, it seems clear that several Islamic terrorist movements that emerge in Africa are not the result of a command or central planning, but are more or less autonomous cells that imitate and mutually inspire, seeking common elements in propaganda and methodologies. As Chatham House experts Alex Vines and Jon Wallace put it, “[In Africa, the] line between jihadism, organized crime and local politics is often blurred and further complicated by global factors such as climate change, population and migration.[8] ” This means that the aforementioned “broth” can arise in Angola, and suddenly, the Islamic flag will be attractive to insurrectionary groups dissatisfied with the government.

Added to this first factor is the spreading across the African continent in relation to Islamic terrorism and which is gradually surrounding Angola. In the neighboring DRC, although still far from the Angolan borders, there is already talk of Islamic terrorism regarding the ADF (Allied Democratic Forces), with links between this organization and the Islamic State. In Tanzania, there are small attacks such as those in October 2020, in the village of Kitaya in the Mtwara region; attack that was claimed by Islamic extremists operating from northern Mozambique. Obviously, the case of Cabo Delgado in Mozambique is paradigmatic of the combination that can be foreseen for Angola, a socio-economic discontent allied to the emergence of Islamic terrorism. Further north, whether in the Central African Republic, Chad or Nigeria, there is a permanent threat from terrorist groups that identify themselves as Islamic.

The porosity of the borders, allied to the socio-economic difficulties, become powerful magnets for the expansion of terrorism that can become an internal threat in Angola, and it is certainly already a border threat and spreading across the African continent.

iii) crime and maritime piracy

From Cape Verde to the Angolan coast, attacks on ships have increased in recent years. In this vast maritime region, pirates – initially concentrated around the Niger Delta – extended their activities to all Nigerian coasts, as well as Benin and Togo. Since 2011, no less than 22 acts of piracy have been recorded in Benin, affecting traffic in the port of Cotonou, which has dropped by 60%. The massive economic impact of maritime crime – which includes illegal fishing, drug trafficking and weapons – on the coasts of West Africa increases every year. The Gulf of Guinea is now considered the continent’s maritime red zone[9].

Angola’s position has been clear, assuming itself as a strategic engine in the fight against piracy, pointing to the creation of a government funding strategy in the Gulf of Guinea and in the Great Lakes region, recognizing that crime has been growing in this area, endangering the region itself from a national, international and regional point of view. It is in this perspective that Angola attaches great importance to the maritime spaces that have to be controlled. In fact, of the 90 percent of crimes committed in the Atlantic Ocean, 70 percent occur in the Gulf of Guinea, which is worrying.

iv) increased competition between world powers with interests in African goods

This situation is more general and perhaps less imminent in causing disruption than the previous ones, however it exists and in the medium term could be the main threat to Angola. Some authors speak of a new “race for Africa”, such as those that took place at the end of the 19th century in connection with the Berlin Conference and after independence in the context of the Cold War. Angola was obviously a central part of both “races”. The first served to delimit its borders and complete the Portuguese colonial intervention, while in the second, it was one of the main battlefields of the US-Soviet Union confrontation. The prestigious English magazine The Economist summarized in 2019 the new, and third, rush to Africa, writing that there is a third wave in the works. The continent is important and is becoming increasingly important, mainly because of its growing share of the global population (by 2025 the UN predicts that there will be more Africans than Chinese). Governments and companies around the world are racing to strengthen diplomatic, strategic and commercial ties[10]. In fact, those who first discerned the continent’s opportunities were the Chinese who, since the beginning of the 21st century, have invested heavily in Africa, with Angola as their main partner, at least in terms of debt. The rest of the world has only just woken up to Africa. But in fact, we see Turkey in search of new markets and allies since it abandoned its alignment with the European Union, the Persian Gulf countries in the same line looking for diversification projects for their economies, and the European Union, led by Germany and France, with Italy and Spain also intensively recovering old ones and arranging new contacts, either for economic reasons or to try to stop the illegal immigration that affects their countries and can cause their governments to lose elections. Also Russia, in the mix of imperial recovery and business demand, returns to Africa. Only the United States of America has pursued a dormant policy towards the continent since Donald Trump, not yet understanding very well what they are doing in substance, apart from some noises against China and/or about Islamic terrorism. However, this lethargy can end.

At the moment, China is far ahead in the new race for Africa. As soon as Europeans and North Americans definitively understand – we are still in an ambivalent stage – that the Chinese presence in Africa is a threat to their geopolitical and economic interests, competition will intensify. It should be remembered that China currently absorbs around 60% of cobalt exports from Africa; 40% iron; and 25-30% of its exports of chromium, copper and manganese.

Consequently, Angola’s role as holder of key raw materials and a stabilizing force for the DRC, another immense repository of resources, will be decisive.

The current moment of the FAAs

In view of the above, it is easy to understand that these times is of great demand for the FAAs, who can once again be called upon to perform functions of national survival.

At this time, according to the most credible sources, the FAAs are comprised of approximately 107,000 active soldiers (100,000 Army; 1,000 Navy; 6,000 Air Force); there are still an estimated 10,000 in the Rapid Intervention Police (2021)[11].

Military expenditure is around 1.7% of GDP, therefore, below the 2% that the United States intends as a parameter for NATO countries (North Atlantic Treaty Organization of which Angola is obviously not a part, but whose parameter can serve as an ideal value of military expenditure). It is not an exaggerated expense, on the contrary, one might think.

Most Angolan military weapons and equipment are of Russian, Soviet or Warsaw Pact origin; since 2010, Russia remains the main supplier of military equipment to Angola[12].

Regarding its military capability in 2022, Angola is ranked 66th among 140 countries considered by Global Fire Power[13]. Its forces include 320 tanks, 1210 armored vehicles, and several artillery pieces. It should be noted, however, that tanks are essentially old, acquired in the 1990s from the Soviet Union. From our research, we could only find a reasonably modern (2016) tank-destroyer type vehicle, the PTL-02 Assaulter purchased from China. As for the naval forces, despite having an extended coastline and responsibilities in the Gulf of Guinea, the country only has 37 patrol boats and no medium or larger ships such as corvettes, frigates or cruisers.

As for the Air Force, there are 299 planes, of which 71 are fighters, 117 are helicopters and 15 are attack helicopters.

A recent analysis by Africa Monitor, which, it should be noted, has reflected a critical stance on the part of João Lourenço’s government, presents an alleged factuality, which, even if it is exaggerated or represents an overly pessimistic perspective, paints a less than encouraging picture of the readiness and material from the Angolan Air Force and Navy. Second, this publication, the navy fleet has its operational levels chronically “impaired by non-compliance with maintenance requirements and/or unpreparedness of its crews.[14]” In the Air Force, too, paralysis will be the keyword. According to the same newspaper, “the units of the transport helicopter fleet that were still operating (Russian-built Mil Mi-8) will be paralyzed, either aircraft from the 1980s-1990s, or units reconditioned later”, there is a “inability to ensure the maintenance of combat helicopters (Mil Mi-24)” and also in “a situation of near paralysis (…) Sukhoi (Su-22, Su-25, Su-30, Su-27).[15] ”Specialists with whom we have contacted directly and who prefer to remain anonymous assure that in recent years there has been no significant purchase of military material. So apparently there may be a need for reinforcement with these branches of the military.

In summary, there are three types of needs in the Armed Forces: obsolete and not modernized material, lack of equipment maintenance and unpreparedness of some cadres for specific activities. This obviously makes it important to intervene in the FAAs in order to increase their budget and increase their operational capacity in the face of the challenges described.

FAA modernization vectors

From all the above, two basic assumptions result that lead us to a simple conclusion. The assumptions are that threats to Angola’s sovereignty and integrity have increased in recent years after a period of some calm after 2002. Today the country faces a new “race for Africa” by the great and emerging powers, the threat of so-called Islamic terrorism spreads across the continent and piracy and criminality in the Gulf of Guinea along the coast is a reality. Added to this is the renewal of internal separatist tendencies and the strong reaction of the formerly dominant oligarchy to the fight against corruption. These facts correspond, at this moment, to some FAAs with some gaps in terms of material, readiness and training, which may, eventually, make an adequate reaction unfeasible in the event of an increase in any of the exposed threats.

It follows from the equation of these assumptions that an FAA modernization policy in terms of equipment, training and readiness/maintenance is essential. On the contrary, what many would claim, a reinforcement of the military budget and a modernizing reform of the Armed Forces is necessary.

The General State Budget for 2022 does not yet fully reflect these needs. If we look at it, from 2021 to 2022 there is a nominal increase in defense spending of 19.7%. It is enough to think that official inflation is around 27% in 2021[16] to realize that in real terms defense spending is decreasing, probably leading to cuts in the military sphere. In turn, defense spending is equivalent to 1.4% GDP[17].

We understand that the modernization of the FAA has a qualitative vector that must be defined by specialists in the area and involve the readiness of the Armed Forces, their implementation capacity and levels of sustainability, as well as the quality of the force they can exert. However, the vector that we focus on in this report is quantitative and we present the very simple suggestion already adopted by the countries of the North Atlantic Treaty Organization (NATO), which is to place defense expenditure at around 2% of GDP[18] . This is not a magic number and can be subject of much criticism, but it represents an objective and quantifiable parameter, and in fact gives political power a measurable instrument to achieve[19] , which can be an advance in good governance and transparency policies that intend to implement in Angola.